China rolls out measures to support economic growth

On April 15, the People’s Bank of China, China’s central bank, announced a reduction in its reserve requirement ratio. The government also published 23 measures last week to support individual and small businesses and stepped up its efforts to keep supply and industrial chains stable. We present an updated view of the China and Hong Kong markets. In our view, these latest measures reiterate China’s stance on economic stability, and believe that China and Hong Kong equities can benefit from these supportive policy actions.

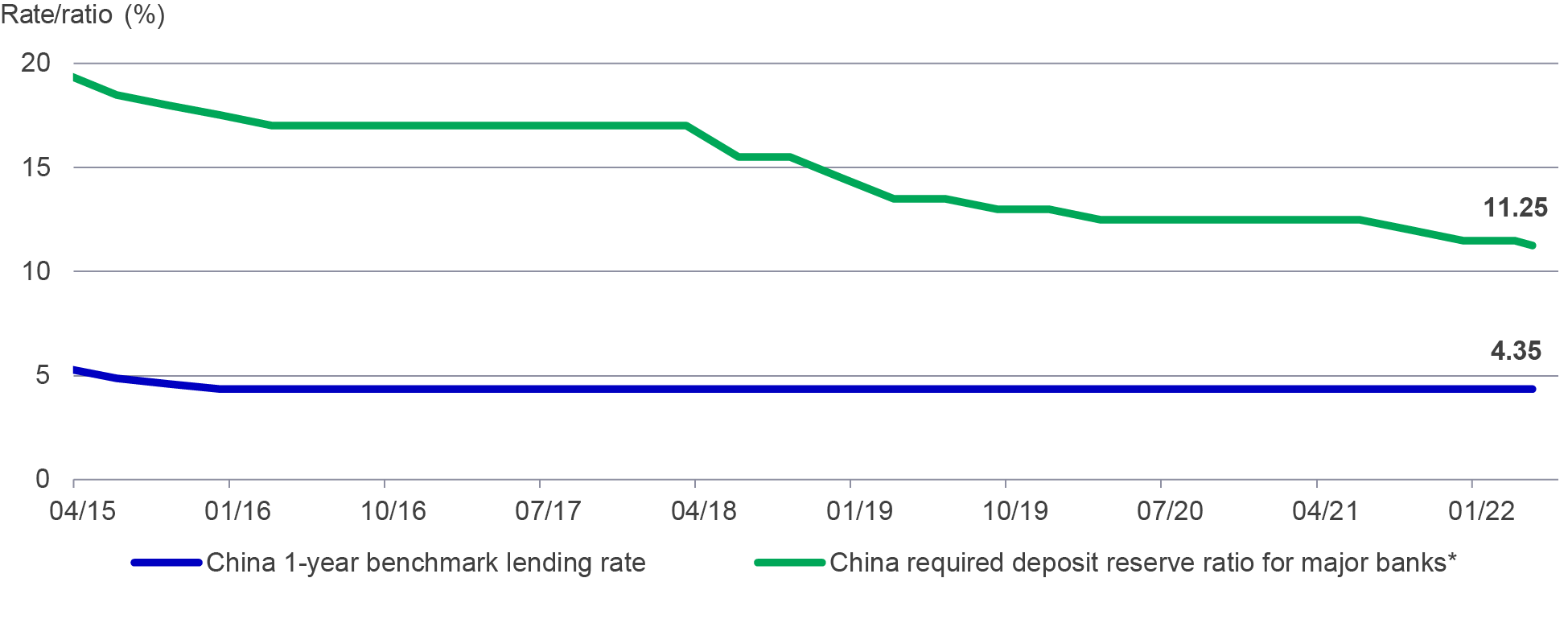

China’s central bank flexes its monetary policy tools

China announced several measures to release long-term liquidity into the financial system to bolster the economy. These include¹:

- On April 15, the People’s Bank of China (PBoC) reduced the reserve requirement ratio (RRR) for most banks by 25 basis points (bps), and by 50bps for smaller lenders, effective April 25.

- The central bank left one-year policy interest rates unchanged, disappointing most economists who had predicted a cut.²

- According to the PBoC, the RRR change will unleash about RMB530 billion (US$83 billion) of long-term liquidity into the economy. The PBoC last reduced the ratio in December 2021.

China’s RRR and lending interest rate

Source: Bloomberg, as of April 19, 2022. RRR refers to reserve requirement ratio, which will be reduced to 11.25% from April 25, 2022.

Measures to support economic growth

China’s corporates and small and medium enterprises may benefit from the central bank’s 23 additional measures, which are aimed at supporting the economy. Some key highlights include³:

- Banks are urged to expand lending to people with flexible employment (e.g., taxi drivers, online shop owners, and truck drivers) and provide longer-term and cheaper loans to small businesses.

- The PBoC vowed to extend or establish relending programs that provide funds for banks to lend to sectors that were hit by the pandemic. Such relending programs are expected to represent approximately RMB1 trillion (US$157 billion) in additional bank loans.

- Local authorities are being called on to set appropriate minimum down payment requirements and mortgage rates based on each city’s conditions, and banks are encouraged to support reasonable financing needs of property developers and construction companies.

- Policy banks are asked to step up their financing to major investment projects, while commercial banks are expected to be more proactive in lending to infrastructure projects and purchase local government bonds to support advanced construction.

- A transfer of RMB600 billion (US$94.2 billion) of profit was made to the central government in mid-April, which will be mainly used for tax rebates and transfer payments to local governments. This profit transfer has increased the base money supply in the country and is equivalent to a 25bps cut in RRR, according to the PBoC.

Separately, the China Banking and Insurance Regulatory Commission vowed to increase financial resources for logistics, transportation, and courier industries and use the relending funds to lower financing costs. It will provide funding support to smaller businesses that are suffering from temporary difficulties due to COVID-19.

The implications of China’s newly announced measures

While some market participants expected a bold reduction in interest rates, we believe China has adequate policy tools other than a rate cut to support growth if needed.

Despite a near-term dampening of investor sentiment, we believe these recent measures prove that China is determined to support the local economy:

- China continues to strike a balance between epidemic control and economic development. On Monday, April 18, Chinese Vice Premier Liu underlined efforts to stabilize supply and industrial chains. Shanghai’s city authorities have asked 666 local and foreign companies, mainly in the automobile, semiconductor, and energy industries, to resume production amid the city’s lockdown.

- We expect more targeted fiscal stimulus to be announced in the third or fourth quarter of 2022, which will likely underpin further economic growth.

- Although more than 60 non-tier 1 cities have already rolled out relaxation measures, additional housing-related policies may be unveiled. Many cities have introduced more favorable mortgage costs or down payment requirements, while more tier 2-cities such as Quzhou, Dalian, Suzhou, and Nanjing have relaxed home purchase and/or resale restrictions.⁴

- China is pushing ahead with its mRNA vaccine development, which should help fight the spread of Omicron or other COVID-19 variants down the road. For example, the country’s health authorities have recently approved the trials of two mRNA vaccines.⁵

Structural growth opportunities in China and Hong Kong equities

While we remain selective, we see opportunities in sectors and key themes in China and Hong Kong equities that should benefit from China’s structural growth story. These opportunities include:

- Exposure to both domestic Hong Kong equities with attractive dividends while also tapping into growth areas

- Potential beneficiaries in the consumption sector (e.g., companies with the ability to pass on cost inflation

- The materials sector, which could potentially benefit from a boost in infrastructure investment

- In general, we continue to favor sectors and investment themes that are likely to benefit from China's 14th five-year plan. These could include consumption upgrades, research and development, innovation, renewable energy and energy transition, as well as new infrastructure.

China stands ready for further policy measures

Overall, we believe China's ready to act and is likely to ease policy further should a sharper economic slowdown occur. In addition, China could turn to fiscal policy to boost growth (such as further spending on investments and infrastructure) as well as tax refunds and cuts. While near-term market sentiment has been mixed, we view the latest measures as signs that China is on track to maintain its economic course.

1 Bloomberg, as of April 19, 2022. 2 “Analysts see less room for China rate cut after ‘conservative’ RRR cut,” Reuters, April 18, 2022. 3 “These Are the 23 Measures China Just Unveiled To Save the Economy,” Bloomberg, April 19, 2022. 4 “Chinese cities ease home purchase down-payments to reignite demand,” Reuters, February 18, 2022. 5 “China approves CSPC, CanSino mRNA vaccines for clinical trial, boosting country’s arsenal against raging Omicron outbreak,” South China Morning Post, April 4, 2022.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. Past performance does not guarantee future results. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeim.com/institutional

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland. Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance

552508