Potential implications of the U.S. presidential election on Asian fixed income

On Tuesday, November 3, 2020, U.S. voters decided who would hold the balance of power in Washington. President-elect Joe Biden was declared the winner of the election (November 7), and at the time of this writing, (November 16), President Trump hasn’t formally conceded defeat.¹ Overall, assuming current expectations hold, that is a Biden presidency and split U.S. Congress, we believe the outcome of the U.S. presidential election should be constructive for Asian fixed income.

We believe greater clarity and policy consistency are the greatest benefits

After months of nonstop campaigning and a hard-fought election, we believe that clarity is one of the greatest benefits that an outcome can bring to the markets. Indeed, there was substantial volatility and uncertainty in the run-up to early November, and the election outcome has catalyzed a rally in risk assets. We expect this to continue over the short term and believe it should—particularly—benefit emerging-market (EM) assets, including Asian fixed income.

Where Asia is concerned, we envisage that a Biden administration might bring greater policy consistency. Over the past four years, U.S.-China relations have progressively worsened, particularly economically, punctuated by a prolonged trade dispute that brought unexpected policy changes that fueled bouts of market volatility. Although we don’t expect a significant improvement in the U.S.-China relations over the near term, we believe the possibility exists for more stable, consistently communicated foreign and economic policy from Washington. This should be positive for Asian fixed-income markets that had previously suffered from volatile policy swings and uncertainty over future actions.

This has created a more favorable macro backdrop for Asian fixed income, which should be underpinned by accommodative monetary policy globally and a weaker U.S. dollar. In the aftermath of the COVID-19 pandemic, global central banks slashed interest rates to cushion the impact of the economic downturn. We expect monetary policy in developed markets to remain accommodative over the near term, particularly in the United States where the U.S. Federal Reserve’s (Fed’s) recent revision of its inflation-targeting framework led Fed officials to signal that interest rates should remain near zero over the next two to three years.²

In our view, an expansionary Fed will likely be coupled with more active U.S. fiscal policy. Separately—while the ultimate scope and quality of the expected stimulus package will depend on President-elect Biden’s relationship with Congress—additional federal spending (and an escalating federal deficit) with lower interest rates should put pressure on the U.S. dollar. We believe that select Asian currencies, such as the Chinese renminbi and South Korean won, may benefit from this dynamic.

Asian fixed-income fundamentals remain intact in a post-U.S. election world

In a post-U.S. election world, the fundamentals of Asian fixed income remain intact—diversified economic growth, resilient credit performance, and relatively attractive nominal and real yields.

The outbreak of COVID-19 dented economic prospects and roiled financial markets across the globe. Asia was no exception—regional economies contracted in the second quarter due to administrative lockdowns and reduced consumption in Western markets. In our opinion, the region still boasts some of the best economic prospects globally due to its economic heterogeneity and diversified growth models.

According to the latest forecasts from the International Monetary Fund, although Asia’s GDP is expected to experience its worst downturn in recent history, surpassing even the Asian Financial Crisis (1997/1998), the rate of its contraction is expected to be the smallest of all major regions. Crucially, Asia is expected to have the strongest economic rebound globally in 2021.³

Resilient credit performance (so far)

The region’s economic performance coupled with its unique credit structure are reasons why Asian credit has remained relatively resilient.

During the first quarter of 2020, when global markets experienced sharp volatility, Asian investment-grade (IG) credit only fell 0.50%, while their U.S. (-4.1%) and EM (-8.6%) peers posted larger losses.⁴

Asia’s unique IG structure provides one plausible explanation for this divergence in performance: The J.P. Morgan Asian Credit Index (JACI) is largely composed of IG credits (77%). Furthermore, a significant component of the Asian credit market (about 40%) is state-owned enterprises and quasisovereign entities that have access to greater economic resources, including government support and bank loans.

Overall, we believe that Asia won’t be immune from the general trend of credit deterioration globally—rating downgrades and defaults are expected to gradually rise over the next two years, although at a relatively lower level in Asia than other regions.⁵ The risk of fallen angels (credits downgraded from IG to non-IG rating) in Asia, although present, should also be more subdued when compared to other global markets.⁶

Attractive rate differentials in Asia

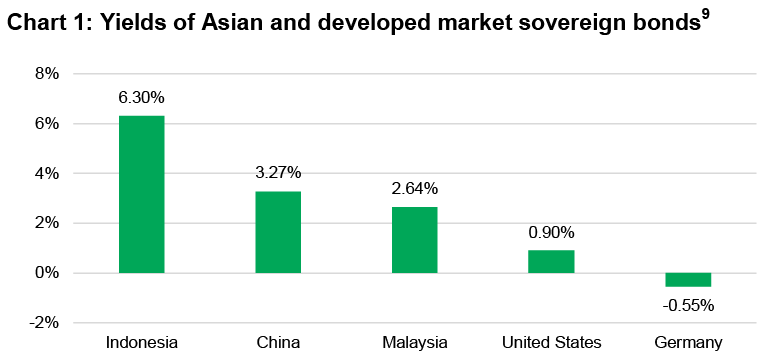

Finally, Asian bonds can offer relatively attractive nominal and real yields compared with their developed-market counterparts. U.S. Treasuries and European sovereign debt are currently yielding below 1%, with some returning negative real yields.7 In contrast, sovereign bond yields across Asia remain higher—such as in China, Malaysia, and Indonesia—with limited levels of inflation.⁸

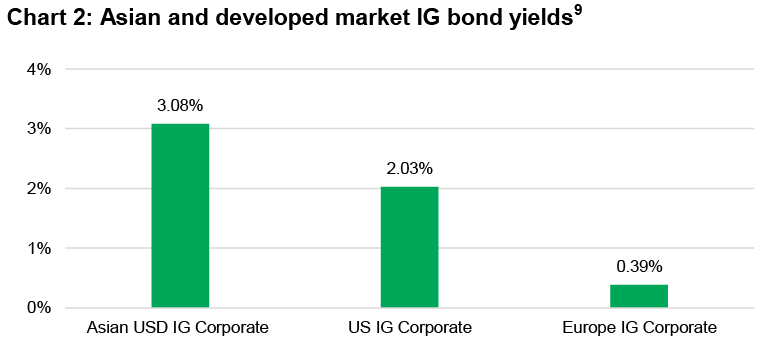

The Asian yield premium can also be observed when comparing U.S. dollar-denominated Asian IG corporate bonds with U.S. and European IG corporate bonds.

Conversely, higher real interest rates could also imply that there may be room for monetary easing. With inflation at bay, nominal interest rates in select parts of Asia could do with further monetary easing, which is supportive of select bond prices.

Conclusion

Assuming the current base case expectations for the U.S. presidential election plays out, we envisage a positive impact on Asian fixed income. The clarity of the results coupled with the possibility of improved policy consistency from Washington should be well received by markets as investors can now focus on fundamentals and take advantage of the growth and rate differentials uniquely present in Asia.

1 On Saturday, November 7, 2020, The Associated Press declared Joe Biden as the victor in Pennsylvania at 11:25 a.m., Eastern time. The victory won him the state’s 20 electoral votes, pushing him over the 270 electoral vote threshold needed to prevail; “Biden Declares Victory, Calls on Americans to Mend Divisions,” Bloomberg, November 8, 2020; “Donald Trump refuses to concede defeat as recriminations begin,” The Guardian, November 7, 2020. 2 “Fed Signals Low Rates Likely to Last Several Years,” Wall Street Journal, September 16, 2020. 3 IMF 2020 Outlook (October version): “Asia and emerging Asia” is forecast to contract by 1.7% in 2020, the smallest rate of contraction among global regions. ”Low-income developing countries,” as a category, is forecast to contract less at 1.2%, but this category comprises markets aggregated from across the world. In 2021, “Asia and emerging Asia” is projected to grow 8.0% in 2021—the highest rate of any region. 4 The J.P. Morgan Asia Credit Index represents Asia IG credit performance, while the JP Morgan Corporate Emerging Market Bond Index represents EM fixed-income performance, and the ICE BofA U.S. Corporate Index represents U.S. IG credit performance. 5 Moody's baseline scenario predicts a trailing 12-month Asia Pacific (APAC) high-yield nonfinancial corporate default rate of 6.0% in 2020, up from 1.1% in 2019. 6 Standard and Poor’s, as of June 30, 2020. The APAC region only recorded one fallen angel so far through the first half of 2020. 7 The 10-year U.S. Treasury yielded 0.90% as of November 12, 2020. 8 The Indonesian 10-year government bond yielded 6.30% as of November 13, 2020. 9 Bloomberg, as of November 13, 2020.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication and are subject to change based on market and other conditions. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers, or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment, or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment, or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer, or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against a loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams, along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by and are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd., which is authorized and regulated by the Financial Conduct Authority; Manulife Investment Management (Ireland) Ltd., which is authorized and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U). Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G). South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC, and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates, under license.

526428