Investing in an evolving China with an All-China approach

In our view, investing in an evolving China can be both challenging and rewarding. Global investors experienced volatility and rapid changes in the regulatory environment for China equity in 2021. Some may ask: is the risk-reward profile for China equity still appealing enough to justify meaningful exposure in a diversified global equity portfolio? And how should investors navigate the changing dynamics of China equity for those who wish to participate in the country’s long-term growth prospects?

To put things into perspective, China equities are typically defined as either onshore or offshore. The former covers mainland China listed A-shares, while the latter encompasses Hong Kong or US-listed China companies, with different sector exposures. We explore why investors should consider adding China equities to their portfolios via an All-China approach. And for those who wish to participate in the long-term growth of China through China equity, how to navigate the changing dynamics in the world’s second largest equity market.

Section 1: China still offers global investors an attractive proposition, and we advocate an All-China approach.

A. Where does China stand today?

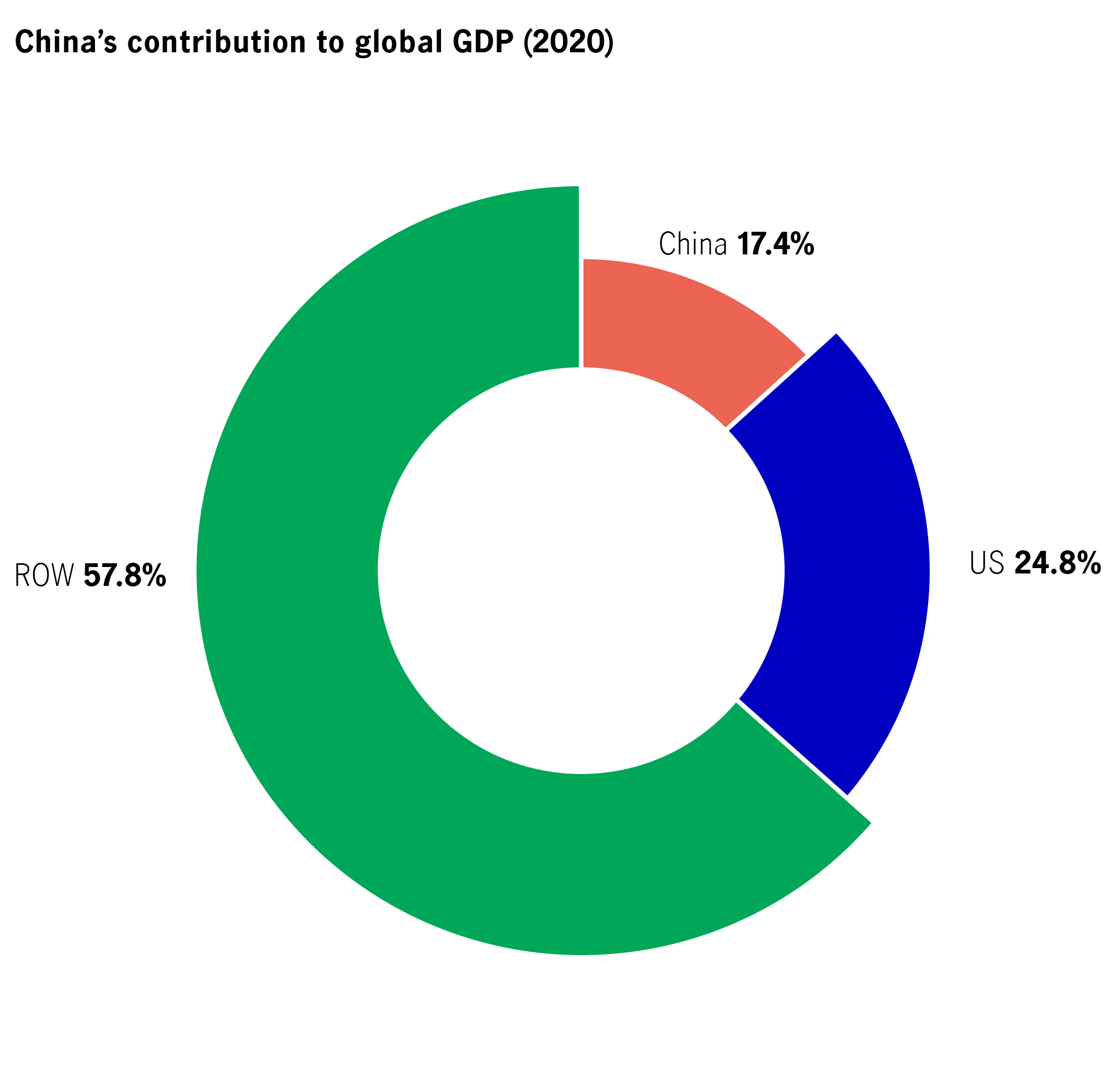

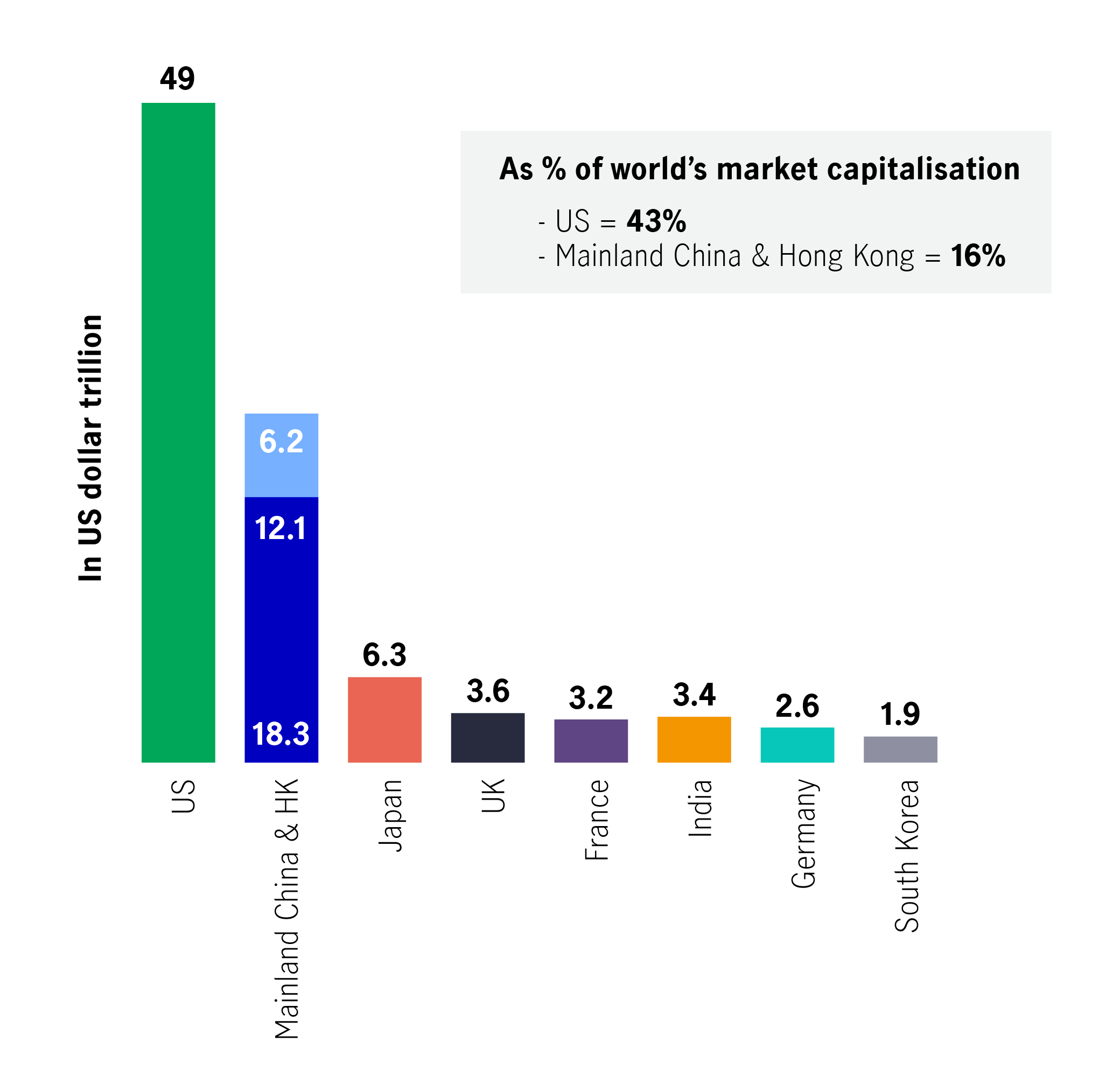

For investors, China is simply too big to ignore. It is the second largest economy in the world1 and one of the key growth engines globally. China represented roughly one-fifth of global economic output in 2020 (see Chart 1) and accounted for around 16% of the world’s total market capitalisation (inclusive of Hong Kong), making it the world's second-largest contributor (see Chart 2) after the United States. Meanwhile, China’s weight in the MSCI All Country World Index is only 3.6%2. As a result, China’s economy and growth contribution to the world is underrepresented by most international market-capitalisation weighted indices.

Chart 1: China is under-owned compared to its global size and influence

Source: IMF, World Bank, the World Factbook, March 2021.

Chart 2: World stock exchanges by market capitalisation (US$ trillion)

Source: Bloomberg, as of 26 January 2022.

B. Policy goals: transitory impact for the long-term good

The changes in China’s regulatory environment since late 2020 have surprised many global investors. From launching antitrust investigations into e-commerce platforms and placing restrictions on youth playing video games to banning afterschool tutoring for profit, the rapidly shifting landscape of reforms in social and regulatory matters has introduced uncertainties into China equity's risk-reward profile.

It is important for investors to remember that this is not the first time the Chinese government has engaged in a regulatory shake-up of economically important industries. Recent efforts include supply-side reforms and price cuts for generic pharmaceuticals from centralised bulk purchase orders. It will probably come as no surprise if more such measures follow.

While reforms can create short-term volatility and uncertainty for equities, their goal is to create better-functioning markets for the long-term benefit of society. The strict measures and regulatory clampdown via anti-trust legislation have led to operational changes by internet blue-chip giants. This could foster a more open and competitive business environment for the internet sector as a whole, and create opportunities for smaller niche players.

Indeed, these regulatory reforms are part of a larger policy push for “common prosperity”, an idea espoused by President Xi Jinping in 2021. The pursuit of common prosperity may raise questions among global investors as to how companies, corporates, and the investor community will benefit from this policy.

We believe that common prosperity aims to reduce the differences between individuals, regions, and urban/rural areas to acceptable levels; corporate profitability and capital accumulation would remain. Increasing the overall pie is the foundation of common prosperity. Indeed, a key goal of common prosperity is to further rebalance the domestic economy towards consumption and away from a reliance on exports, while lowering the import/export share of GDP to 25% from 35%3. Longer term, it seems clear that government policy will aim to reduce the real estate sector's contribution to economic growth; the sector is currently the single largest in China’s GDP composition4. Another key goal from China’s common prosperity pledge is to increase GDP per capita from $10,000 in 2020 to $23,000 by 20355. Sustainability-driven capex investments and domestic consumption growth are therefore to be promoted, supported, and prioritised.

To achieve this, we believe that the Chinese government will need to foster the development of other industries such as biotech and industrial automation. This is even more important due to the chronic friction in the Sino-US diplomatic relationship. From this perspective, we see compelling structural opportunities across many sectors that can ride on key secular trends, such as domestic consumption and localisation of the semiconductor supply chain, advanced manufacturing, and the push for electric vehicles (more in Section 2).

"As a fundamental bottom-up driven investment manager, we use our analytical lens to look through short-term volatility and noise, and ensure that our investment theses are robust enough to capture mispricing opportunities in different market conditions."

C. Benefits of the All-China approach

For investors interested in the opportunities offered by China equities, there are a variety of different ways to gain exposure. We advocate an All-China approach to the asset class. Indeed, while some funds offer products that access mainland China or Hong Kong equity markets separately, we believe that a hybrid approach offers greater flexibility and opportunity for investors. Thus, based on our conviction, we invest in equities listed in mainland China and Hong Kong, and in depository receipts listed in overseas markets, including the United States. (See the Appendix for a brief description of the different ways investors can invest in All-China equities.)

In our view, China equities offer an exciting and rapidly expanding investment universe. The total number of onshore and offshore listed Chinese companies, with a market capitalisation exceeding US$500 million, had grown significantly to over 4,325 as of the end of 20216, an increase of nearly 57% from 2018. This was driven by a buoyant IPO market, which recorded a healthy number of China listings on key stock exchanges. The large number of listings, coupled with an ever-expanding investor base, gives rise to opportunities from potential mispricing.

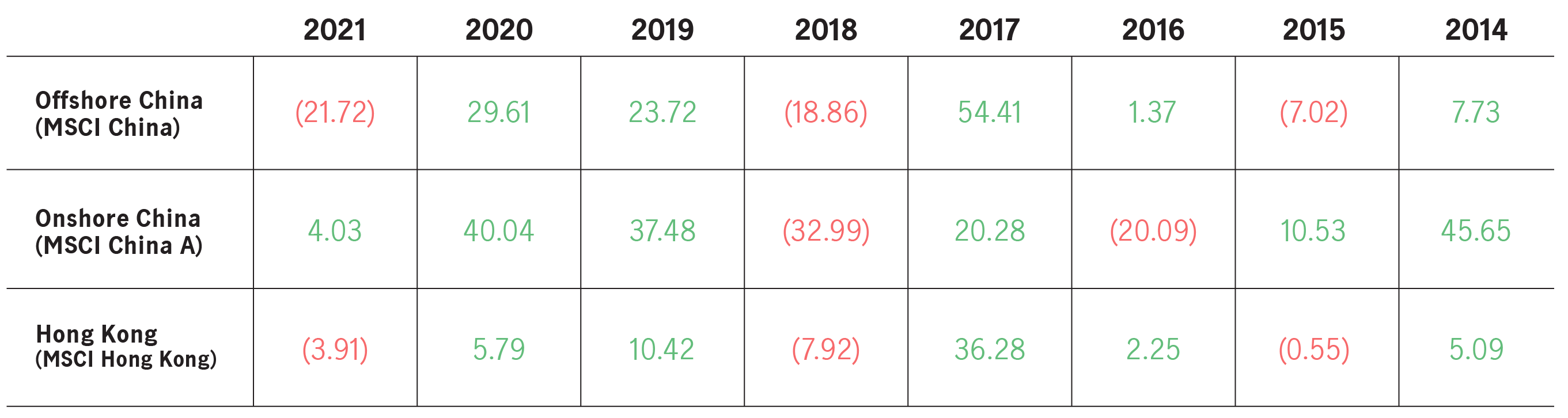

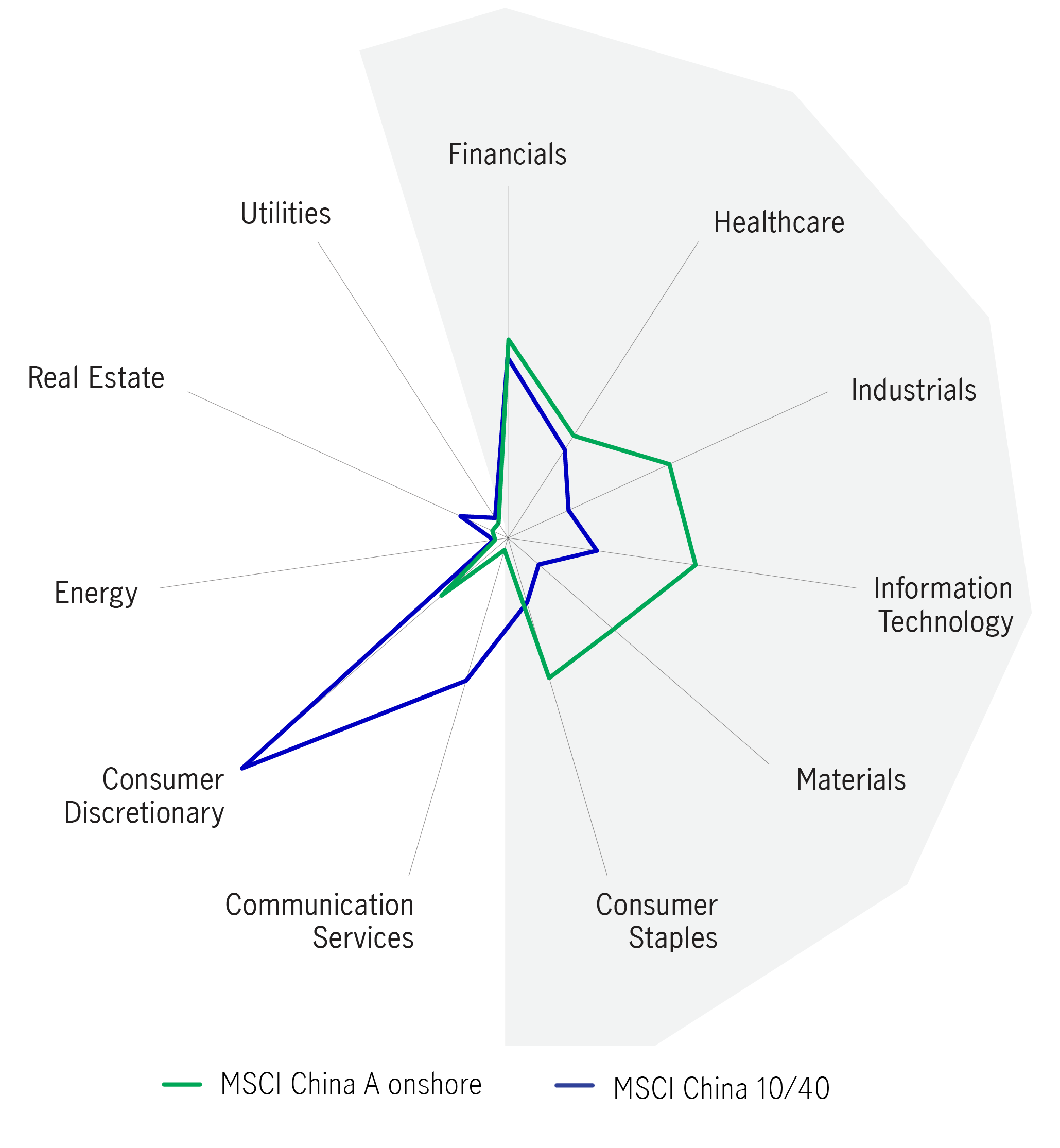

For global investors, the All-China approach has led to attractive returns (See Chart 3). In addition, with financial markets more volatile, the All-China approach to investing in China equities allows investors to benefit from a variety of sectoral and market-capitalisation opportunities (Chart 4). This is particularly so if investors include Hong Kong equities as part of their overall exposure to enhance stock selection opportunities for companies deriving growth from China but with different macro and micro drivers. Hong Kong looks set to continue benefitting from various IPO pipelines and from being a capital raising hub for institutions such as international banks and insurance giants.

Chart 3: Attractive returns from navigating both onshore and offshore China equities

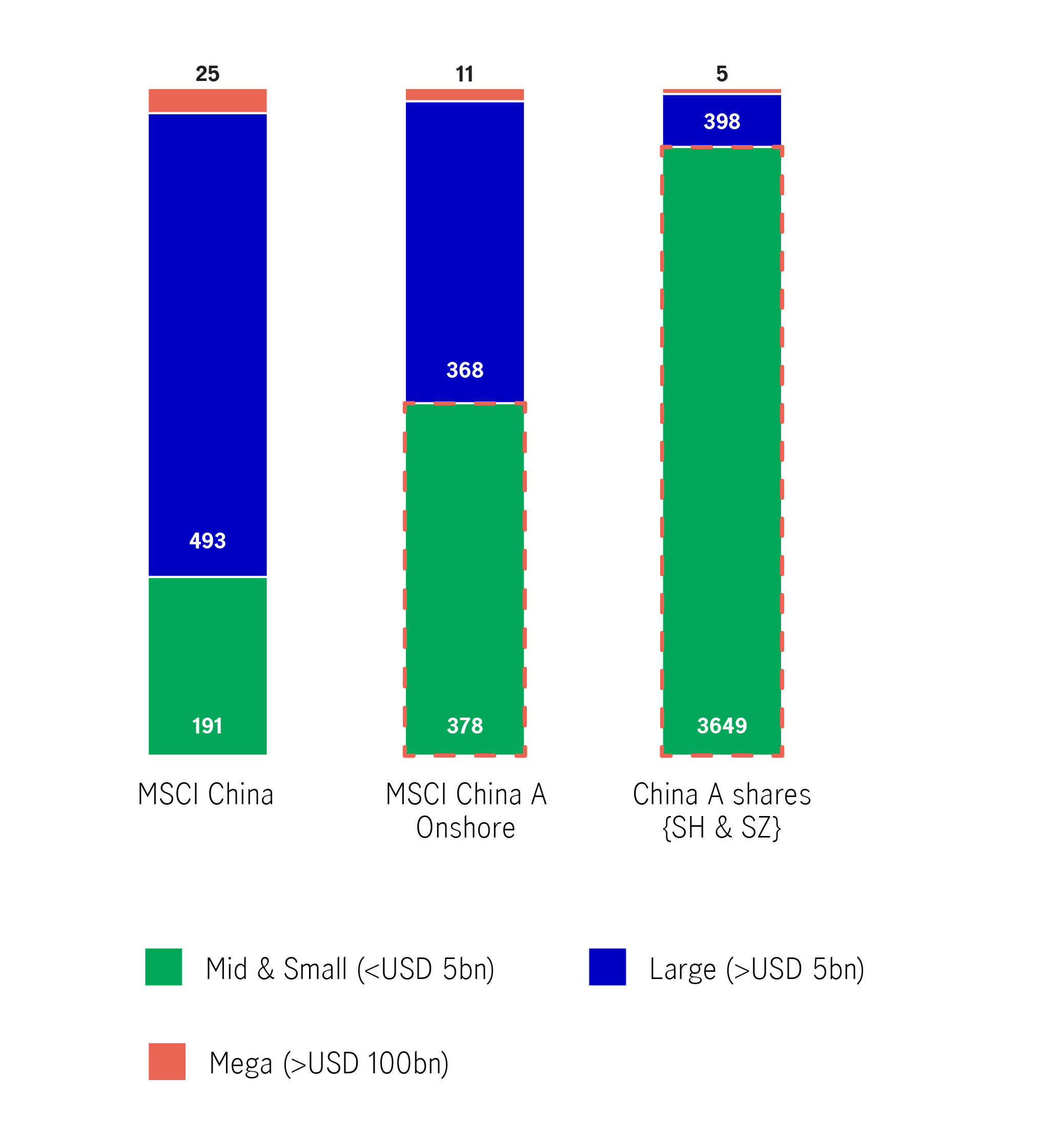

Chart 4: Broader sectoral opportunities and market-cap opportunities

Opportunities set by sector % of index weight

Source: MSCI, S&P, Bloomberg, as of 30 September 2021.

Opportunities set by market capitalisation, by number of stocks

Source: Bloomberg, Shanghai Stock Exchange, Shenzhen Stock Exchange, as of 31 March 2021.

Opportunity for alpha and diversification

Empirically, alpha opportunities are evident in China equities. Nevertheless, the ability to capture them requires on-the-ground resources and informed perspectives. This is especially so in a complex and fast-developing market like China, where informational advantages and mispricing opportunities arise from the dislocation from fundamentals. Therefore, we believe that on-the-ground research, stringent stock selection, and active management are critical to capturing alpha.

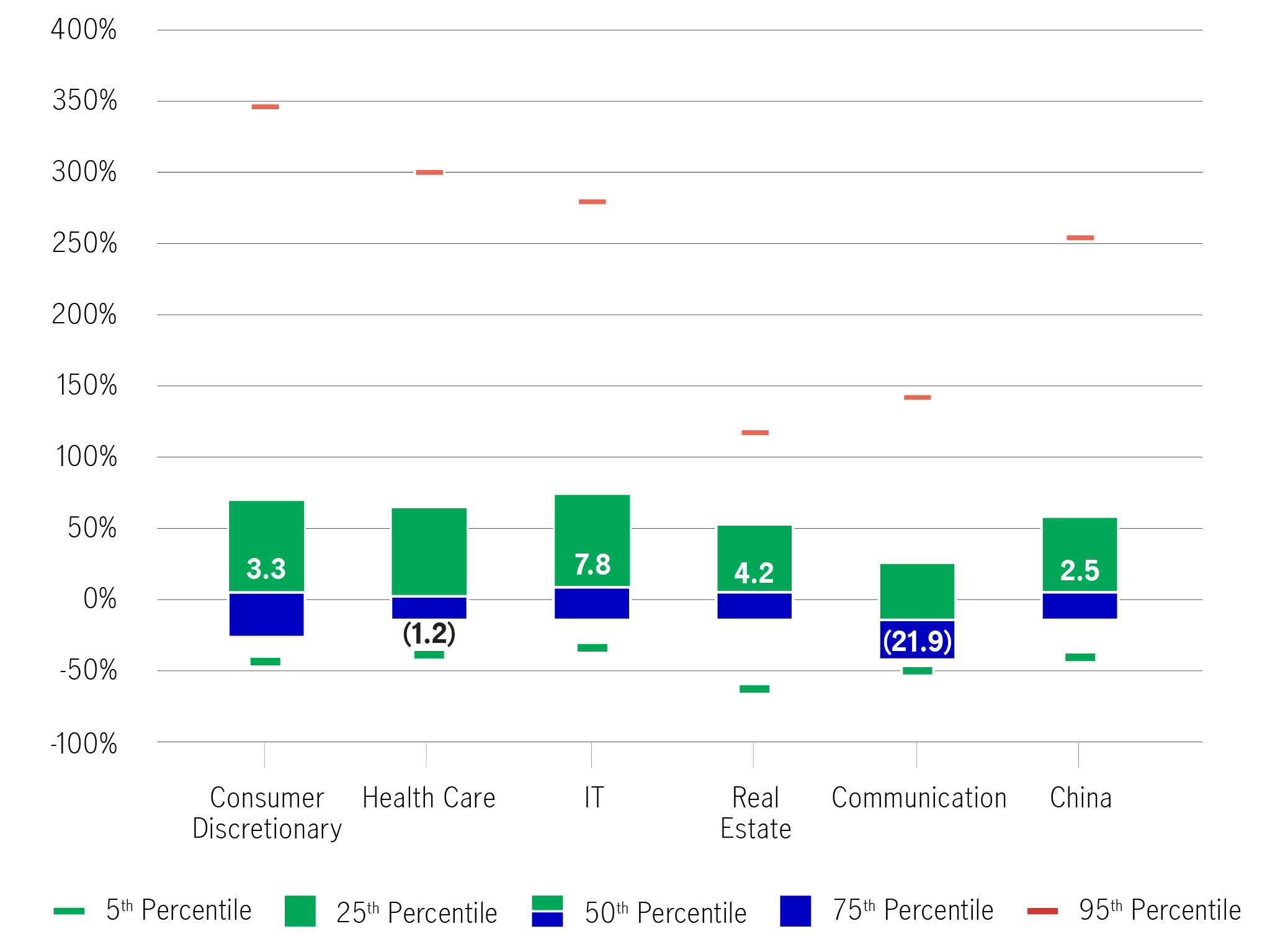

While not all stocks are winners, China equities could offer ample alpha opportunities. Chart 5 shows the five-year excess return dispersion of key equity markets. As can be seen, China equities generally offer a wider dispersion of returns compared with their developed and developing market peers. This means that historically, the range of potential returns for this asset class is wider, allowing discerning stock pickers to capture higher upside potential.

Chart 5: China equities have generally offered a wide dispersion of returns over the past five years

Wide return dispersion for China equity, even within sector

Total cumulative return dispersion per sector over past 5 years (%, p.a.)

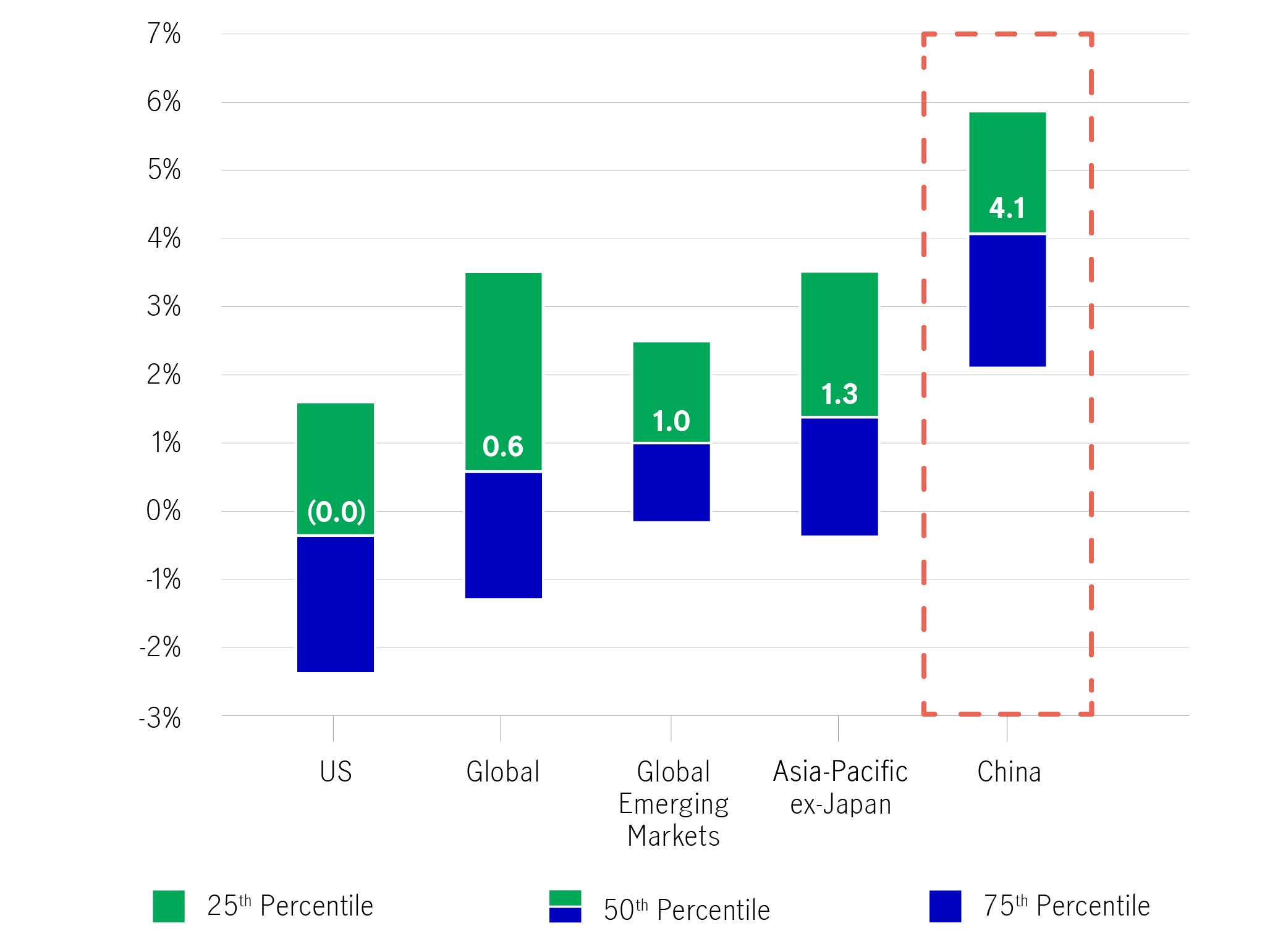

China equity presents more alpha opportunities

Five-year excess return (p.a. %) over manager benchmark

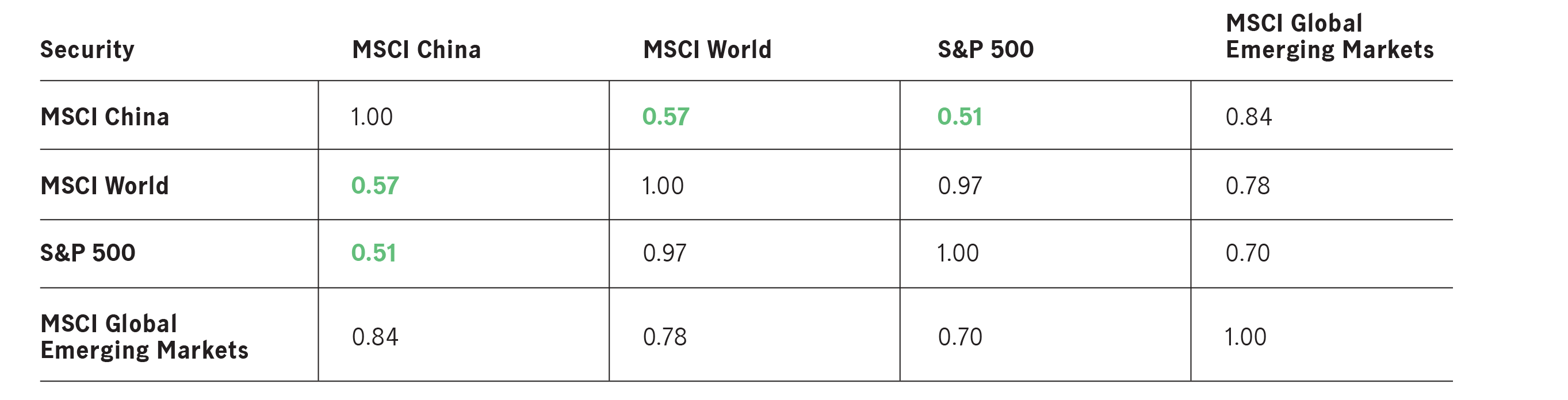

Foreign investors in China equities may benefit from portfolio diversification. From a tactical perspective, China has been decoupling from developed markets and other emerging economies alike. The low correlations stem from the fact that government policy in the country has been significantly different from other markets, rather than stemming purely from flows and liquidity. China’s decoupling from the US and countercyclical fiscal and monetary policies can provide attractive alternatives to global investors who would like to diversify from the Fed’s policy moves. Over the past ten years (see Chart 6), investors in China equity have benefitted from lower correlations of their investments to both developed global and emerging markets.

Chart 6: From a longer-term perspective, foreign investors have benefitted from lower correlations in China equities over the past 10 years

Section 2 – What to expect from China’s growth story and China equity? We take a look at the opportunities in key sectors.

A. Growth still solid and diversified across industries

Despite a volatile 2021, we believe that China’s growth story is still vibrant. Indeed, while government regulations may continue to change in key sectors, investors should look to broader, longer-term opportunities in essential areas such as domestic consumption/innovation and sustainability-related themes, including carbon neutrality and changing demographics.

Electric-vehicle batteries: Innovation on the global stage

We believe that domestic drivers such as consumption and investment will be the key catalysts for economic growth and equities, with innovation in the digital economy and biotech as the anchors. Furthermore, as China aims to strengthen its position as a high-value global manufacturing hub, industrial automation and manufacturing upgrades led by advanced technology will also be in focus as the country faces future demographic and productivity challenges.

After all, digitalisation and consumption growth are critical for China to progress. In the Politburo's October 2021 study session, the central government called for co-existence of regulation and development for internet platforms and stated that the digital economy is crucial for enhancing productivity and international competitiveness. In January 2022, the Chinese government also published a plan for the development of the digital economy as part of its 14th five-year plan, aiming to boost the sector’s share in the national GDP to 10% in 2025 from 7.8% in 2020.

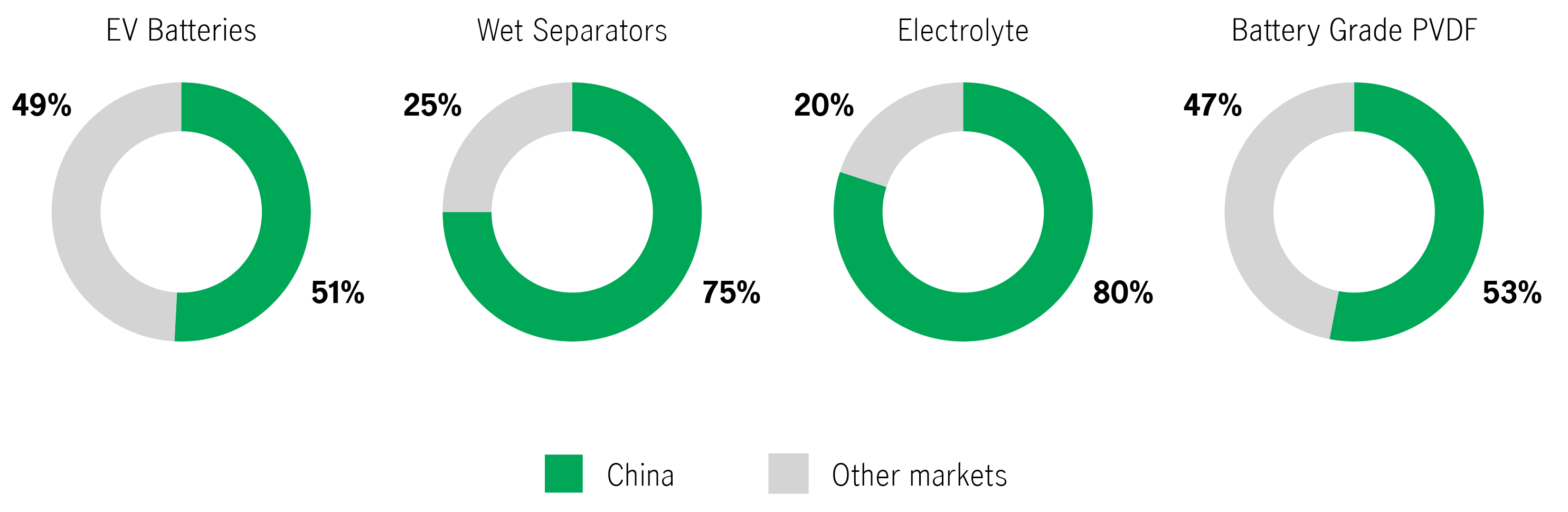

We believe that electric-vehicle battery manufacturers are a key part of the innovation agenda. As shown in Chart 7, Chinese manufacturers already account for over half of production in global markets.

Chart 7: Importance of China’s battery supply chain in global market (2021 market share)

Source: "China Battery Supply Chain" research report from Morgan Stanley, as of 3 January 2022. PVDF stands for Polyvinylidene Fluoride and is a component commonly used in lithium-ion batteries.

Renewable energy: The peak of carbon emissions and the pursuit of net-zero

In October 2021, the State Council proposed the Action Plan for Carbon Dioxide Peaking before 2030. Under the plan, by 2030, the share of non-fossil energy consumption should reach around 25%, and carbon dioxide emissions per unit of GDP should drop by more than 65% (compared with the 2005 level), successfully achieving a peak of carbon dioxide emissions before 2030.

We see solid growth drivers in the renewable-energy sector, which is a strategic priority for policy-directed funding. The construction of wind and photovoltaic bases has already been accelerated thanks to the elevated pace of government bond issuance and policy support. Over the longer term, we expect a roadmap that will help China’s journey towards peak carbon emissions by 2030, placing the country’s decarbonisation efforts under a more structured framework. Overall, we believe that if China can convert this energy problem into a manufacturing one, this would help the country greatly in achieving peak carbon emissions, and ultimately carbon neutrality.

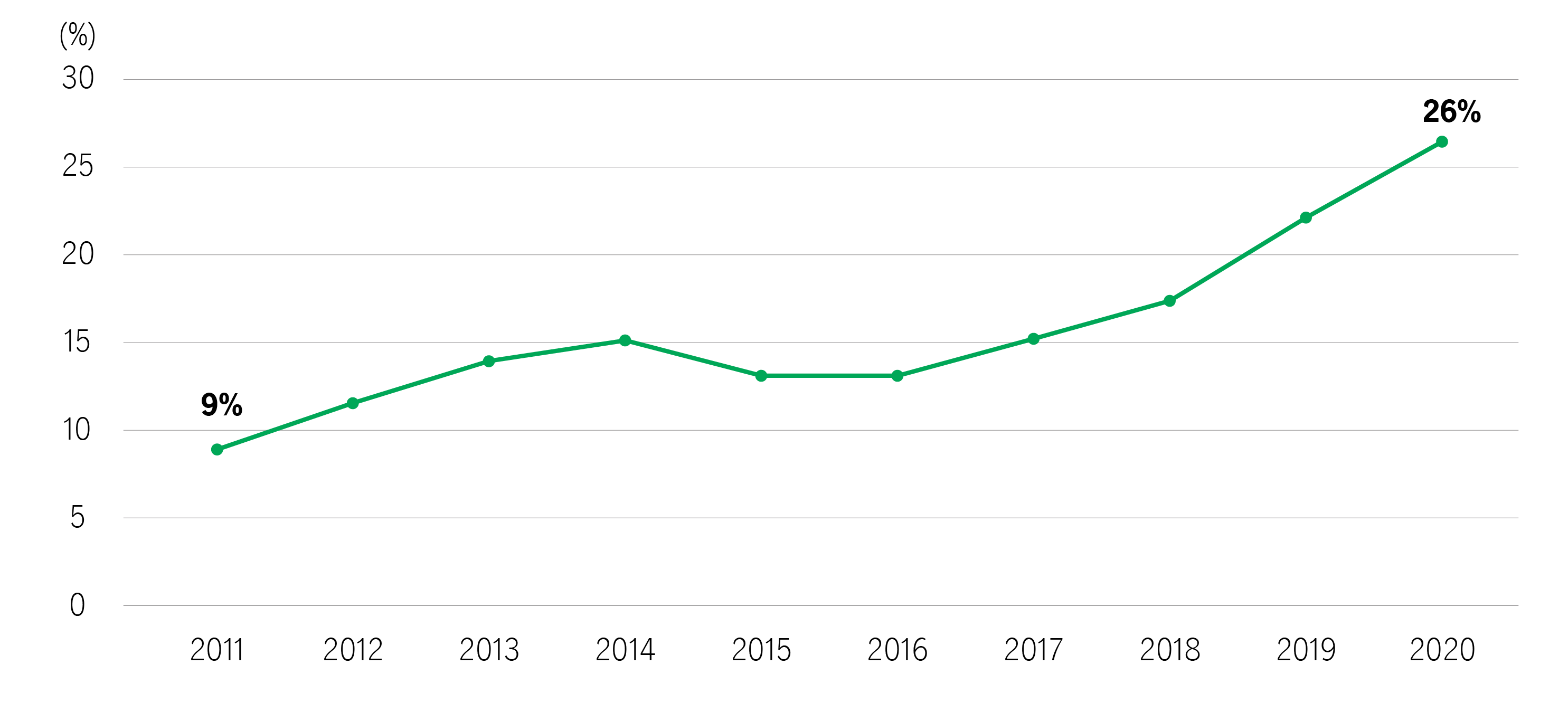

Cosmetics: Opportunities in shifting demographics

Changing demographics are reshaping the investment landscape and available opportunities in China. Importantly, this change is in tune with local tastes. We already see this in the evolution of products and brands aimed at old and young alike. The consumption upgrade for China’s population, especially the middle class, is demonstrated by the shift in demand from goods to high-quality lifestyle services like property management and ‘experiences’ such as travel. For consumer products, the commercial winners will likely be determined by those that can adapt quickly to local tastes. We have seen Chinese brands gain market share from foreign equivalents in multiple categories such as sportswear, skincare, and cosmetics.

Chart 8: Chinese brands’ share in domestic cosmetic sales (makeup, %)

"The beauty of China equity is its breadth and depth, which allow us to dig deep even in niche growth areas. Greater Bay Area is an interesting example, where we see plenty opportunities for regional champions to flourish."

B. Capital market development and China equity listing

As China’s contribution to the global economy grows, institutional investors should consider participating in this growth via equity exposure, in our view. This would likely mean carving out a dedicated allocation to China, as the country is under-represented in industry benchmarks. As mentioned in Section 1, despite the country’s significant size and influence, China equities are still arguably under-owned by investors; their weighting in the MSCI All Country World Index is currently only 3.6%7.

The integration of China equities into the world financial system, through their addition to global indices, has raised the profile of many Chinese companies. The rise of corporate juggernauts in wide-ranging industries, from technology to manufacturing, has also caught the eye of global investors.

Under the common prosperity ideology, we believe that smaller companies will benefit directly from more balanced growth and the wider expansion of the middle class. The new onshore exchanges, such as the newly launched Beijing Stock Exchange and fast-developing listing regimes in Hong Kong, therefore look likely to enrich the universe of China equities as a whole, generating interest from investors looking to tap into structural growth opportunities, especially those at the early stages. Longer term, the enlarged investible universe will likely complete the opportunity set that is more reflective of the innovation and growth of China's underlying economy.

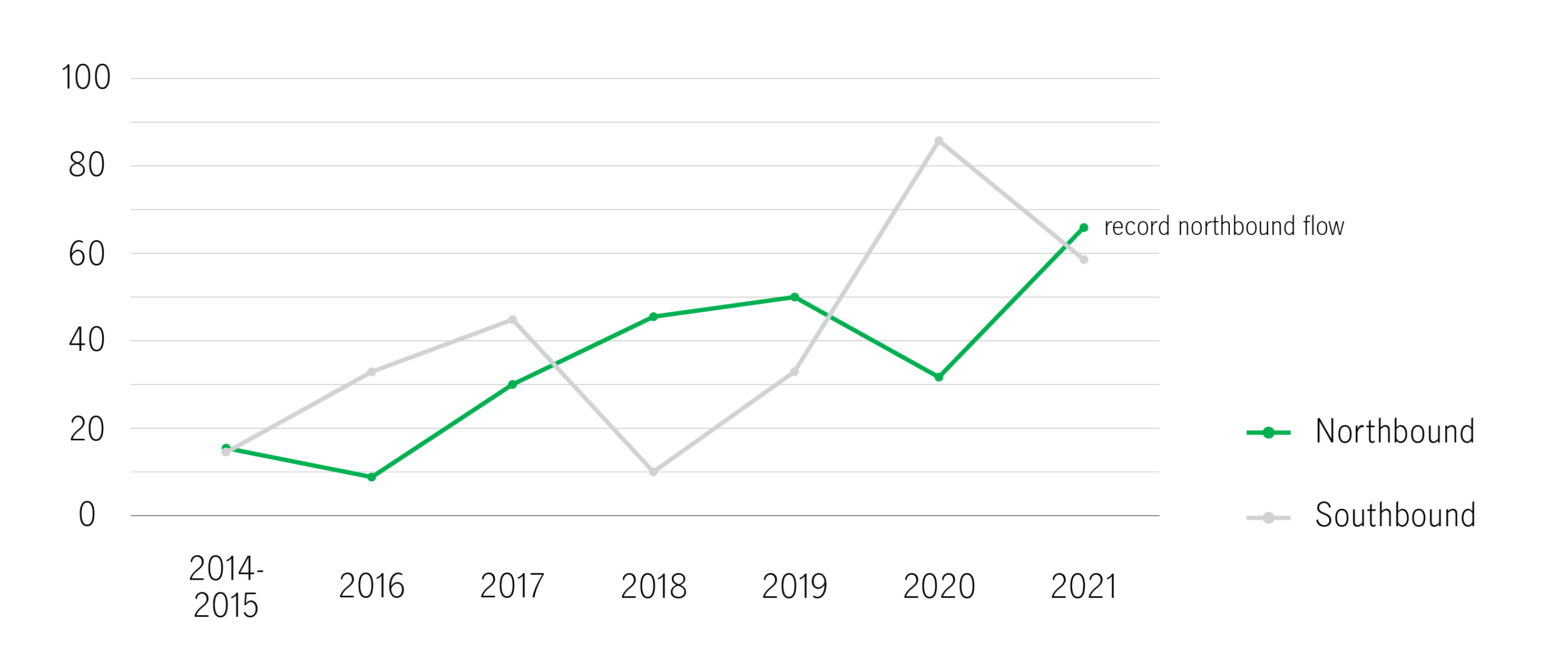

Furthermore, Stock Connect, which was developed as a mutual market access service between Hong Kong and mainland China, has seen vibrant capital flows between the two exchanges. The Shanghai-Hong Kong Stock Connect, launched in 2014, allows Hong Kong and foreign investors to buy China A-shares listed in mainland China (northbound trading), and mainland China investors to purchase securities listed in Hong Kong (southbound trading). Net accumulative buy balances for both northbound and southbound trading have risen steadily since the service was established, a trend set to continue over the longer term.

This increase in cross-border flows has driven liquidity and volumes in China equities, opening up the investment universe for global investors and increasing the likelihood of China equities being included in more global benchmark stock indices in the longer term.

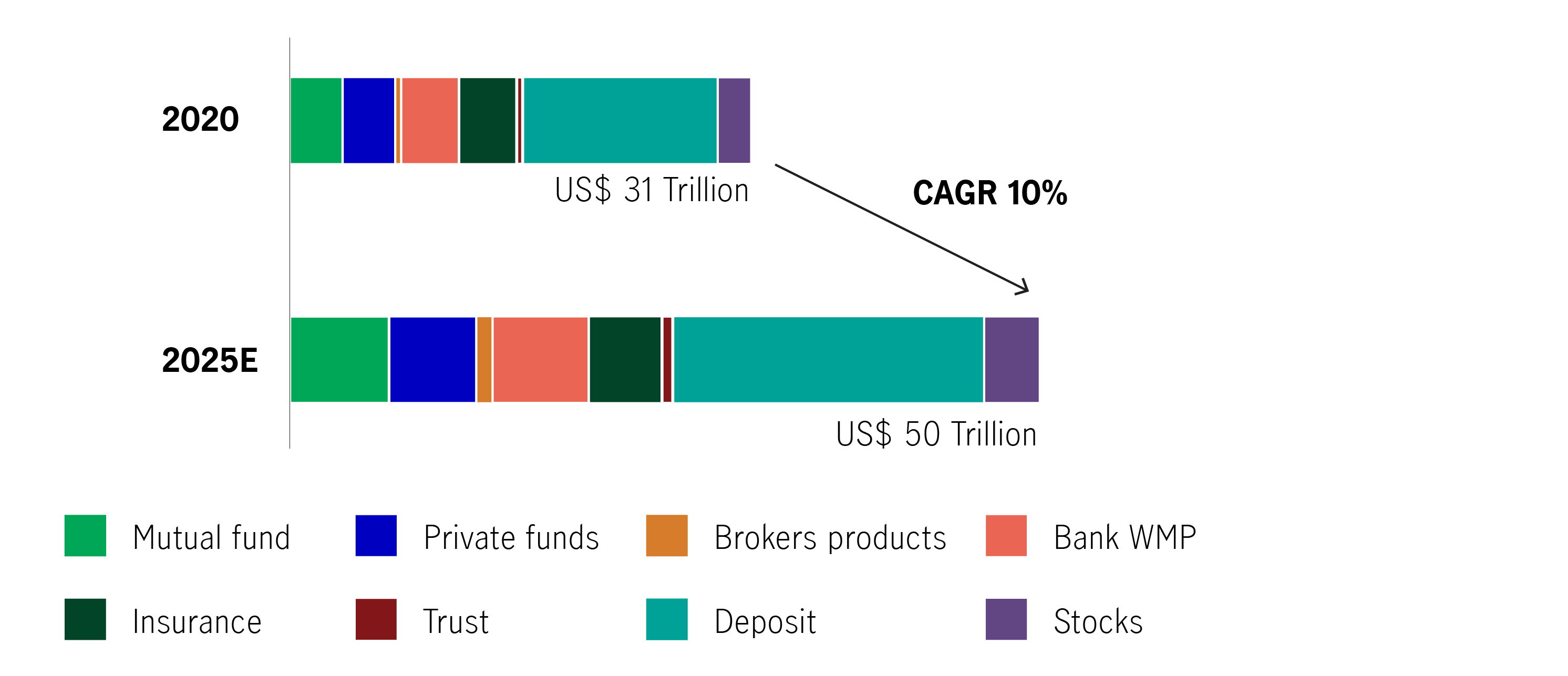

As Chinese households’ wealth grows, investible wealth in financial assets could also grow. The debt crisis in the property sector may increase mainland households’ willingness to diversify their investments from property to financial assets. We believe that this would also be in line with the government’s direction, which encourages more diversified, institutionally managed investment products for domestic investors and actively promotes financial market innovation through connectivity.

Chart 9: Stock Connect net buying (US$ billion)

Chart 10: China onshore household investable financial assets growth projection

Source: “China Capital Markets II - Wealth management the next growth engine” research report from Goldman Sachs, 14 July 2021. The above information may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations. There is no assurance that such events will occur, and the future course may be significantly different from that shown here.

Section 3: On-the-ground resources and an ESG-integrated approach to capture All-China opportunities

A. Importance of on-the-ground research

While alpha opportunities are available in Chinese equities, the ability to capture them requires on-the-ground resources and informed perspectives. This is especially so in a complex and changing market like China, where there is information asymmetry and market dislocation. Therefore, on-the-ground research, stringent stock selection, and active management are critical to creating investment value.

A keen understanding of a company’s business model is an important first step in the value-creation process. The Greater China equities team looks out for the potential of these companies, which are mostly at the infancy stage. Their potential may not be immediately apparent, and they are often open to broad interpretation. It takes an experienced, on-the-ground manager to pick out the crème de la crème among the China equities universe to generate alpha.

This section presents three case studies exploring how the team provides value to investors in China’s equity market through fundamental bottom-up investment analysis within a robust environmental, social, and governance (ESG) integrated investment framework.

Messages from the investment team

(From left to right)

Kai Kong Chay (Senior Portfolio Manager, Greater China Equities)

"As a fundamental bottom-up driven investment manager, we use our analytical lens to look through short-term volatility and noise, and ensure that our investment theses are robust enough to capture mispricing opportunities in different market conditions."

Ronald CC Chan (Chief Investment Officer, Equities, Asia ex-Japan)

"The continuous evolution and expansion of China’s equity investment universe presents both opportunities and challenges. Our team’s goal is to provide desirable solutions to allow global investors to take part in the next chapter of China’s growth story."

Wenlin Li (Senior Portfolio Manager, Greater China Equities)

"We can never be complacent when it comes to investing in China A-shares. We often benefit from our differentiated views by constantly challenging herding behaviour in the market and adhering to our stringent stock selection process."

Winson Fong (Senior Portfolio Manager, Greater China Equities)

"The beauty of China equity is its breadth and depth, which allow us to dig deep even in niche growth areas. Greater Bay Area is an interesting example, where we see plenty opportunities for regional champions to flourish."

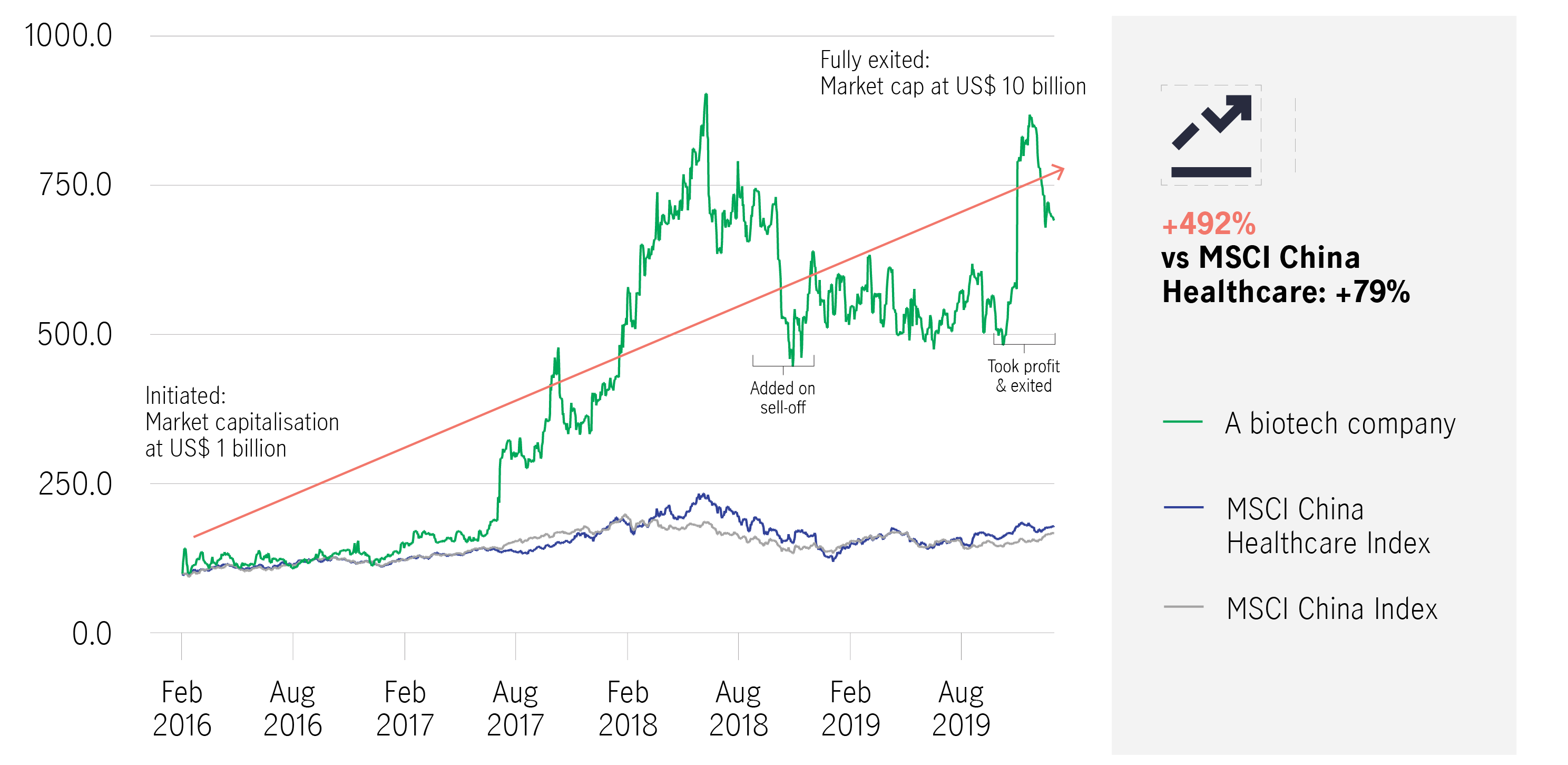

Case study I: Uncovering an R&D winner8

Company A is a biotechnology firm specialising in developing medicines for cancer treatment. Comprising industry experts, its strong management team has an established track record in bringing innovative drugs to the commercial phase.

Company A’s pipeline included four internally generated oncology candidates at various phases of trials or filing for regulatory approval in mainland China or the US. One drug candidate, which was on the brink of commercialisation, had a potential sales value of US$10 billion.

During the IPO in 2016, valuation was a challenge given that the company was at its pre-profit stage. Traditional P/E multiple analysis would therefore not have been applicable. However, with net present value (NPV) analysis and sum-of-the-parts valuation, our team concluded that the stock price at initiation offered over 40% upside potential to its fair value.

Using the Growth Cash flow Management Valuation (GCMV) framework, we identified the following advantages in the research process:

Growth

Four internally generated oncology candidates in the pipeline

One drug candidate ready for commercialisation had a potential sales value of US$10 billion at peak level

Cash flow

A successful IPO raised sufficient funding for further research

Management

Industry experts with established track records in bringing innovative medicines to the commercial phase

Valuation

The company was at the pre-profit stage upon IPO in 2016, rendering traditional P/E multiple analysis inapplicable

With NPV analysis and sum-of-the-parts valuation, our team concluded that the stock price at initiation offered attractive upside potential (>40%) to its fair value

Catalyst

Continuous development results for new drugs at various phases of trials or filing for regulatory approvals in mainland China or the United States

Chart 11: Price performance of Company A

As can be seen from Chart 11, following the IPO, the stock rose steadily and increased almost fivefold over the next four years, outstripping the MSCI China Healthcare Index, which increased by only around 80%.

Following our in-depth analysis and disciplined exit strategy, in November 2019, we divested the stock nearly four years after our investment, taking profit from uncovering this rare investment gem.

B. The team’s ESG integrated investment approach

With ambitious decarbonation goals and a common prosperity pledge, ESG considerations are critical when it comes to investing in China. Indeed, with the rise of ESG, the need has also intensified for investors to apply a rigorous framework and due diligence to uncover potential risks and opportunities.

We believe that investors can benefit from an All-China strategy that fully integrates ESG considerations into the investment process.

With a stable and well-resourced investment team of over 40 on-the-ground investment professionals, Manulife Investment Management’s staff in Asia generate alpha by focusing on under-researched ideas in the China market, providing differentiated exposure to opportunities. Our investment process fully integrates ESG considerations from end to end.

We seek ESG opportunities that bode well under China’s push for sustainable growth, while also considering the ESG risks. For example, the requirement for e-commerce platforms to pay the social security contributions of delivery personnel can be quantifiable, and the additional operating costs are incorporated into our financial models and fair-value assessments. In addition, we always scrutinise corporate governance matters, especially how the company treats minority shareholders. For example, if the group or companies have engaged in any unfavourable related party transactions at the expense of minority shareholders, the risk/reward profile of such companies will be heavily discounted in our investment analysis, or the company may be avoided altogether.

Case study II – Identifying beneficiaries under China’s decarbonisation push9

Here is a compelling example of how the team integrates ESG factors into the end-to-end investment process. The journey begins with our team’s initial idea generation, then follows a path that encompasses our internal GCMV framework (a mechanism that determines a company’s intrinsic value), then concludes with the sale of the holding.

ESG risks and opportunities

The team owned one of China’s largest oil & gas groups. However, we were mindful of its more pollutive fossil-fuel business, and subsequently monitored the company’s energy transition efforts. Eventually, we concluded that from an ESG risk and opportunity perspective, the portfolio required greater exposure to the new-energy sector. After significant research, a leading renewable-energy project operator was identified as a suitable candidate.

The proposed candidate (Company X) is the only pure-play China-based solar-power operator listed in Hong Kong. Company X focuses on acquiring existing solar farms and acts as ongoing operator. At no point is Company X involved in the construction phase. We believe that the firm’s operating model is sustainable from a financial standpoint, and that looking ahead, it will benefit from policy tailwinds.

Higher revenue and earnings

Examining the numbers more closely, we identified that revenue and earnings should increase by more than 20% and 15% (CAGR), respectively, from 2020 to 2023. This will likely be driven by capacity acquisition (600W p.a. planned) from its parent company, which has more than 3GW of projects on hand.

From a cash-flow perspective, we expect the funding for capacity expansion to come from share issuance or low-cost bank loans. The company currently has a single-digit gearing ratio, so there is plenty of headroom for further capitalisation.

Also, as the group is not a state-owned enterprise (SOE), its management team focuses on downstream solar operations. In other words, it has less exposure to upstream construction risk and the impact of policy change.

The team’s discounted cash flow (DCF) model concluded that the purchase price of the stock offered attractive upside potential. Ultimately, our team believed that solar installation costs would be lower than the market expected, which is a key catalyst for growth. And cheaper borrowing should emerge from green financing initiatives, which should boost the candidate’s net profits.

Portfolio action

The team decided to focus on the new-energy sector by selling the oil & gas group, which lacked apparent growth catalysts and the scope for significant upgrades in its environmental efforts. The switch was made into the renewable-energy project operator, which we identified via our ESG-integrated investment analysis.

Case Study III – We are an active owner and exercise stewardship over our portfolio companies10

Our ESG-integrated investment approach does not end with a buy decision. At post-investment, we continue to exercise our stewardship via active engagement with our portfolio holdings on ESG matters with the goal of achieving better investment outcomes and value creation for the companies.

ESG Engagement – Seeking to create value for our portfolio holdings

The team does not penalise companies for a lack of ESG disclosure. Instead, we enhance our investment thesis by actively engaging with a business to understand risk factors, its readiness for disclosure, and whether there is a clear path to achieve long-term goals.

In 2020, we engaged with a fast-growing semiconductor producer (Company H) in China with a below-average ESG rating (from a third-party rating agency) of CCC. We believed that the low ESG rating could be due to a lack of public disclosure by the company and homogeneity on the part of the rating agency.

Background

Semiconductor producers consume huge amounts of water. According to China Water Risk (CWR), a large fab facility processes 40,000 wafers per month, consuming 4.8 million gallons of water per day, which equates to the annual water consumption of a city of 60,000 people. As part of our ESG-integrated research, we identified that one of our portfolio companies could be affected by the water shortage in the Wuxi region, which might delay semiconductor production, thus impeding financial returns. Therefore, we decided to engage with Company H to clarify the water shortage issue.

What we did

Firstly, we engaged with Company H, which was rated as an ESG laggard by a third-party ESG data provider. We asked the reasons for the increasing water usage and about the company’s mitigation and adaptation measures. The company’s management explained that this is due to the newly built fab in Wuxi. The construction period usually needs more water; the Wuxi fab has now reached 70% capacity, and the company expects the intensity to start declining in 2021.

Secondly, we encouraged the company to conduct water risk assessments, set targets to increase wastewater recycling, and reduce its overall water consumption.

Lastly, we conducted a benchmarking exercise to identify the disclosure gap between Company H and its best-practicing peers and to encourage the company to disclose physical climate risks based on recommendations from the Task Force on Climate-Related Financial Disclosures (TCFD).

Outcome

In response, the company utilised the WRI Aqueduct Water Risk Atlas tool to identify assets in areas of water stress in its latest sustainability report. It formulated a plan to conduct regular water balance tests and establish an emergency plan for tap-water rationing to prepare for any interruption in the municipal tap-water supply network. In addition, Company H also set targets to reduce water consumption for eight-inch wafers by 12% by 2030 from the 2015 level. Consequently, the company’s ESG rating was upgraded to B by the same rating agency after the company published its ESG disclosure report.

Through this engagement, we not only addressed the material ESG risks as part of our fiduciary duty and to protect our clients’ interests, but also helped the company to enhance its ESG performance. This strengthens our belief that our outcome-oriented engagements are essential and add value to some Chinese companies that are not familiar with the disclosure requirements, latest standards, or areas of concern in relation to ESG topics.

Conclusion

China equities have come a long way since the country opened its economy around 40 years ago. Today, the robust economic giant boasts a vibrant stock market, offering plenty of gems waiting to be picked out by eagle-eyed investors. An actively managed, bottom-up approach that aims to capture opportunities in all market environments by investing across sectors, share types, companies, and capitalisations can be rewarding for investors with long-term horizons.

With our longstanding experience and stringent stock selection, our team helps investors identify potential winners, some of which might otherwise have been overlooked. Our on-the-ground resources and informed perspectives have consistently defined our expertise in navigating China’s complex market, where information asymmetry and market dislocation are common. We offer an exceptional level of industry expertise, with our active and flexible investment approach to capturing alpha helping investors to harness the immense potential offered by China’s growth.

Appendix

Types of shares related to All-China equities:

Onshore

A-shares: Securities of Chinese incorporated companies that trade on either the Shanghai or Shenzhen stock exchanges. They are quoted in Renminbi.

B-shares: Securities of Chinese incorporated companies that trade on either the Shanghai or Shenzhen stock exchanges. They are quoted in US dollars on the Shanghai Stock Exchange and Hong Kong dollars on the Shenzhen Stock Exchange.

Offshore

Chinese stocks listed in Hong Kong

- H-shares: Securities of China-incorporated companies that trade on the Hong Kong Stock Exchange, they are quoted and traded in Hong Kong dollars.

- Red Chip: A company incorporated outside mainland China that trades on the Hong Kong Stock Exchange and is substantially owned, directly or indirectly, by mainland China state entities, with most of its revenue or assets derived from mainland China.

- Private enterprise: A non-state-owned Chinese company incorporated outside mainland China and traded on the Hong Kong Stock Exchange.

Hong Kong Equities: Other Hong Kong listed stocks are stocks that have substantial business interests (i.e. in terms of operations or revenue) based in Hong Kong.

American Depository Receipts (ADRs): Securities of non-US incorporated companies that trade on a US stock exchange. They are quoted in US dollars.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange-trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd., Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

550860

1 World Bank, 2020 nominal GDP estimates as of 1 July 2021. 2 MSCI, Bloomberg, as of 31 December 2021. 3 Source: 《中國統計年鑒2020》(2020 China Statistical Yearbook),《中華人民共和國2020年國民經濟和社會發展統計公報》(2020 PRC National Economic and Social Development Statistical Bulletin) 4 A research paper (published in August 2020) by renowned Harvard Professor of Public Policy and Economics Kenneth Rogoff and IMF Economist Yuanchen Yang estimated that the real estate sector accounts for around 29% of China’s GDP. This includes housing investment, services such as managing, renting, and buying, along with other inputs such as commodities and consumer durables. 5 Source: "Increased incomes, social mobility crucial to common prosperity", China Daily, 26 October 2021. 6 Bloomberg, as of 31 December 2021. 7 MSCI, as of 31 December 2021. 8 The historical success, or the investment team’s belief in the future success, of any engagement strategy is not indicative of, and has no bearing on, future results. The examples described do not represent all engagements. It should not be assumed that all engagements will be successful. 9 The sustainability case studies are intended for illustrative purposes only to demonstrate the approach of the investment team to integrating sustainability risk considerations into their investment decision-making processes. Each decision will vary depending upon our evaluation of unique sustainability risks, factors and opportunities. 10 The sustainability case studies are intended for illustrative purposes only to demonstrate the approach of the investment team to integrating sustainability risk considerations into their investment decision-making processes. Each decision will vary depending upon our evaluation of unique sustainability risks, factors and opportunities.