India: the long-term outlook remains compelling, despite notable short-term challenges

The global spread of the coronavirus (COVID-19) has sent shockwaves through global equity markets. The impact, however, has been unevenly distributed, providing opportunities for investors. We offer our outlook on Indian equities. Overall, we believe that despite near-term volatility, the country’s robust foundation—built on structural reform, the domestic nature of the market, and prudent monetary and fiscal policy—should help it to navigate the current challenging market environment.

India currently faces notable short-term challenges, including the outbreak of COVID-19 and the preceding slowdown of the informal economy. We take a look at the current situation, the response from policymakers, and how both issues affect our views. Finally, we explain why investors should remain focused on positive long-term themes in India.

COVID-19: an unexpected but ultimately manageable shock

The COVID-19 pandemic is an unprecedented global health crisis, and its impact is likely to dominate global markets and policymakers’ attention at least in the near term.

Until February, India was relatively less affected by COVID-19 than other countries. After the World Health Organization declared it as a pandemic, the Indian government imposed several restrictions¹ and subsequently announced a nationwide lockdown on March 24 that’s scheduled to end on May 3. The total number of confirmed cases in India has reached 29,451.² This aggregate number is still low on a per capita basis given India’s substantial population. While there may be concerns that the case number is underestimated due to the low per capita testing level in India (around 492 tests per million people), the percentage of positive results (infections/tests) remains low at 4.4%, despite the testing of mostly higher-risk cases.³

The lockdown seems to be working as the five-day compounded daily growth rate in infections has slowed to 7.0% (April 27) from 18.0% (March 31). In terms of geography, the infections are quite concentrated: On April 21, there were 61 districts—out of total 717 districts in India—that had more than 50 cases.⁴

We acknowledge the vast uncertainties associated with a pandemic; however, there are some positive signs emerging in India: (a) a lower incidence of positive test results, (b) a falling rate of growth in new infections, and (c) quick identification of hotspots and the robust measures taken to stop the spread of the virus.

In the near term, we still expect the number of new infections to rise, albeit at a decelerating pace. That said, over the next month, we expect to see a gradual exit plan from the lockdown. Indeed, some businesses have already been allowed to resume operations with social distancing for some of the lesser affected districts.

Policy maker’s response: fiscal stimulus was underwhelming, we expect more measures

In response to the economic impact of the lockdown, March saw the government announce a stimulus program worth approximately US$23 billion, or around 0.8% of GDP, which provides food and income security to low-income households. The package was distributed through cash transfers, employment support, credit support, and food support.

While these are critical initial moves to support the economy, we believe policymakers need to take bolder steps to address this unprecedented economic threat. The size of the current stimulus package is inadequate to effectively counter the estimated loss of output, which is approximately 6.0% to 8.0% of GDP.

"While a valuable debate about whether India has the fiscal room to afford a substantial stimulus is taking place, it’s important to note that the size of India’s support program is by far the lowest, as a percentage of GDP, among the top 10 global economies."

We think that more measures will be announced in the coming weeks, as the exit strategy from the lockdown is formulated. This will be vitally important: Without adequate countermeasures, a substantial loss of output may create a second-order impact in consumption patterns and amplify the cyclical pressures that were already visible in the economy even before the lockdown.

While a valuable debate about whether India has the fiscal room to afford a substantial stimulus is taking place, it’s important to note that the size of India’s support program is by far the lowest, as a percentage of GDP, among the top 10 global economies.⁵ We believe that policymakers can find a way in such unprecedented times by adopting unconventional policies.

If policymakers make it abundantly clear that unconventional policies will be time- and event-specific, and would be unwound once its objectives are achieved, we think financial macro stability won’t be affected. On the brighter side, investors could also start focusing on whether economic growth can return in the medium term should a targeted fiscal package be able to contain the immediate downside.

RBI: focused on providing adequate liquidity

The Reserve Bank of India (RBI) has also stepped in to provide adequate liquidity to counter a sudden stop in economic activity, which would negatively affect firms’ revenues and cash flows.

Recent actions include:

- On March 27, the RBI reduced the policy rate by 75 basis points (bps) to 4.4%. To boost liquidity, the RBI unveiled total liquidity support of INR 3.75 trillion (roughly US$50 billion or 1.7% of GDP) across programs such as the targeted longer-term refinancing operations (TLTRO).⁶

- The RBI also ordered all lending institutions to allow a moratorium of three months to borrowers on repayment of all term loans.

- On April 17, the RBI further added to its liquidity measures by announcing another set of TLTRO measures aimed at providing liquidity to nonbanks. To encourage the transmission of credit, the RBI further reduced the rate that it pays to banks when they place surplus liquidity with the RBI.

We think these measures will stabilize market functioning and ease financial conditions. Once the government decides on the final fiscal package, we’d expect more steps from the RBI, including how to manage the bond supply.

We expect a gradual return of economic activity, but the landscape will be different

While the administrative lockdown is necessary to avert a public health crisis, it’ll come at a notable economic cost as it has disrupted activity in most sectors. Our base case remains that under the current lockdown assumptions,⁷ we expect an output loss of 6.0% to 8.0% of annual GDP and a higher fiscal deficit as tax collection should be lower.

We expect the economic recovery to be gradual because a certain amount of social distancing will continue over the medium term to avoid another wave of infection. In turn, this will cause an uneven recovery across different sectors. Businesses that depend on the gathering of people, such as retail, hospitality, tourism, cinemas, exhibitions, and construction sites, may see ongoing restrictions and weaker activity. On the other hand, sectors that cater to social distancing, including personal mobility, packaged foods, telecom, and home improvement, automation, white goods, and consumer electronics, are likely to recover faster.

Existing cyclical slowdown of the informal economy

Despite the favorable long-term backdrop for Indian equities, the economy faced specific cyclical challenges even before the COVID-19 pandemic:

- Government reforms have bolstered the formal sector over the past few years; however, income levels in the informal areas have suffered as a result.

- Credit growth among nonbanking financial companies has steadily declined due to a freeze in the wholesale money market during most of 2019. This has affected overall credit growth, particularly in the informal sector.

The ongoing lockdown in India will amplify these existing cyclical challenges. Unless the economy is supported by adequate stimulus measures from the government, the sudden stop in economic activity will affect income and savings.

Policymaker’s response: complementary fiscal and monetary policies

Before COVID-19, the government and the RBI had already started to address the cyclical challenges. The government focused on longer-term structural policies to encourage investment and job creation, while the RBI offered support with monetary policies to cut rates and push out liquidity to the real economy.

Fiscal measures that focus on the long term:

- A reduction of corporate tax rates on new investments to incentivize capital formation and attract foreign investment.

- The removal of the dividend distribution tax to encourage private sector investment.

- A simplified personal income regime with reduced rates—a move that’s in line with the streamlining of the tax code.

- Expansion of the PM-KISAN scheme, which directly transfers money to farmers in a targeted way.

- Higher spending on long-term initiatives, such as rural roads, irrigation, warehousing, and transportation, to improve the productivity of the economy.

Supportive monetary measures:

- Operation Twist—In mid-December 2019, the RBI announced a simultaneous purchase of long-term bonds and sale of short-term government bonds under its open market operations program. This is a tool that closely resembles Operation Twist that was used by the U.S. Federal Reserve from late 2011 to the end of 2012 to manage the yield curve, a policy that effectively brought down long-term rates.

- Long-term repo operation—At its policy meeting in February, the RBI announced the long-term repurchase of one-year and three-year bonds, a program that amounted to INR 1 trillion (0.5% of GDP) to keep short-term rates aligned with the recently cut policy rate.⁸ Coupled with Operation Twist, these policy initiatives should not only lower rates but also inject more liquidity out to the real economy.

- Targeted credit easing—Despite higher liquidity and rate cuts by the RBI, credit transmission has remained a persistent issue over the past few quarters in both quantum and the pricing of credit. Against a policy-rate reduction of 135bps (until February 2020), the weighted average lending rate of banks on fresh rupee loans had declined by only 69bps.⁹ To ease this situation, the RBI lowered reserve requirements for auto loans, lending to micro, small, and medium enterprises, and allowed banks some flexibility, delaying classification of commercial real estate loans by one year where the projects were deferred due to reasons beyond the control of developers.

The situation should gradually improve, but some unconventional measures are necessary due to COVID-19

Despite these two short-term challenges, we retain our long-term view on India. Indeed, we have detailed in our past commentary that our constructive Indian equity outlook is founded on the structural reforms that the current administration undertook in its first term. These measures laid the foundation for a formalization-led growth. .

We also argued that with these fundamental building blocks in place, the reelected Indian government has a unique opportunity to revitalize economic growth through the “3Rs”:

- Recycle—Funding government spending needs through the privatization of state-owned enterprise assets.

- Rebuild—Aggregating savings by providing tax cuts to the private sector and households.

- Reinvest—Providing incentives for manufacturing firms to reinvest such savings to substitute imports and increase the country’s global market share of exports.

We believe the 3Rs should help address India’s cyclical growth challenges through higher government spending, increased savings for the private sector and households, and create more job opportunities by encouraging new investment.

At the same time, some elements of the 3Rs may face delayed implementation due to COVID-19, such as recycling (the privatization of state-owned enterprises). In our view, policymakers will need to adopt innovative solutions to bridge the gap, which we believe they’ll find through increased government spending and other policy measures.

"Our estimates suggest that each US$10 drop in crude oil prices helps the country’s current account balance by roughly US$13 billion."

We believe Indian policymakers are in a relatively good position to accomplish this due to the country’s ample foreign exchange reserves and the low level of short-term foreign debt, which lends to a robust capital account. In addition, the country’s inflation outlook remains benign, and while the fiscal situation could deteriorate, the recent sharp fall in crude prices could turn the current account deficit to a surplus.

Indeed, the sharp correction in crude oil prices should remain a key positive catalyst for markets, as India is a large importer of crude oil. India will benefit from a lower import bill and improved current account balance. Our estimates suggest that each US$10 drop in crude oil prices helps the country’s current account balance by roughly US$13 billion.¹⁰ This translates into higher domestic savings and provides room for the RBI to remain accommodative, as a US$40 fall in oil prices could result in approximately US$50 billion of total savings.

Positive long-term market view

Overall, the COVID-19 pandemic will accelerate the formalization-led growth story that underpins our long-term bullishness on Indian equities. The listed market, which is represented by the organized sector, should emerge more robustly and gain market share. It’ll require financial strength to overcome this difficult period and management bandwidth to pivot corporate strategy and operations as economic activity resumes under the shadow of social distancing.

In the current environment, we believe the following type of companies and sectors are likely to succeed:

- Companies that benefit from new social distancing and work-from-home norms after economic activity resumes post-lockdown. Sectors include personal mobility plays (two-wheelers), home automation and improvement plays (consumer electronics, white goods, decorative paints), personal hygiene products, packaged foods, and telecom.

- Import substitution plays benefiting from government policy of encouraging domestic manufacturing (electronics manufacturing services companies), as well as a diversification of production away from China due to the trade war (specialty chemicals and pharma). We also expect select information technology service exports to benefit as they’re enabling remote working across the globe.

Finally, we also believe that some companies are less likely to succeed—sectors likely to suffer from social distancing are retail, leisure and travel, hospitality, and commercial real estate. Companies with high fixed costs and debt on their balance sheet should face a disproportionate downgrade risk during the lockdown.

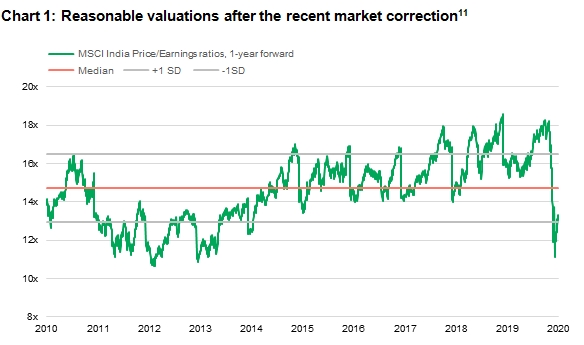

Valuations are below historical median after recent correction

The correction in India’s equities market is in line with its global counterparts in March and April, and the market’s valuation is now below the 10-year median level. While more earnings downgrades are possible in the near term, we believe it’ll normalize in the medium term. We believe that India remains a growth story that is local, defensive, and its exports have a good opportunity to gain global market share.

Lastly, investors should also be aware of the risks to our medium-term constructive view. These include a rebound in the COVID-19 infection curve or a second wave of infections as the economy reopens. Risks could also emerge if the current lockdown period is extended, or if the government were to provide a lower than expected level of fiscal support.

1 Measures included are border closures through the suspension of visas and domestic measures, such as the closure of schools, colleges, and public places. 2 MOHFW India, as of April 27, 2020. 3 Data as of April 22, 2020, MOHFW India. 4 Credit Suisse Research, as of April 21, 2020. 5 “Policy responses to COVID-19: Policy tracker,” IMF, as of April 27, 2020. 6 The facility allows banks to borrow at the policy rate and buy commercial paper, investment-grade bonds, and cut the cash reserve ratio by 100bps (giving more liquidity to banks). 7 The strictest form of the lockdown will be in place for roughly one month. 8 “RBI Announces Two Long-Term Repo Operations in March,” Bloomberg, February 25, 2020. 9 RBI, Citigroup, February 2020. 10 Manulife Investment Management, March 12, 2020. 11 Bloomberg, as of April 24, 2020.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. Past performance does not guarantee future results. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeam.com.www.manulifeim.com/institutional

Australia: Hancock Natural Resource Group Australasia Pty Limited., Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Asset Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. Thailand: Manulife Asset Management (Thailand) Company Limited. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

514316