Later for longer: the U.S. bull market tests its endurance

Key takeaways

- We think continued economic growth—powered by a healthy consumer— can support healthy U.S. stock performance in 2019.

- The primary thing standing in the way of this continued expansion would be the advent of a deeper and prolonged trade war between the United States and China.

- Whether risk appetite is strong or weak, we think investment opportunities will persist—particularly in the communication services, financials, healthcare, consumer discretionary, and information technology sectors.

As 2019 begins, the U.S. economy should be moving ahead at a “normal” rate of roughly 2% to 3% growth. Unemployment stands at multidecade lows, and wage growth could remain healthy. Interest rates will likely be climbing at the gradual pace to which markets have become accustomed over the past two-plus years, and consumer and business confidence may remain close to multidecade highs. While U.S. corporate earnings may experience slower year-over-year growth in 2019, we think they’ll be climbing at healthy rates, with lower taxes and lighter regulation continuing to boost prospects across a number of sectors. Inflation should hew closely to the U.S. Federal Reserve’s (Fed’s) target level of 2%, especially if commodity prices remain in check. We think these conditions, while tempered in strength relative to recent history, will still be powerful tailwinds to have at your back as an investor in U.S. stocks.

"While U.S. corporate earnings may experience slower year-over-year growth in 2019, we think they’ll be climbing at healthy rates, with lower taxes and lighter regulation continuing to boost prospects across a number of sectors.”

Much has been made of the lower-for-longer nature of the economic expansion following the 2007/2008 financial crisis, and now market observers anxiously regard the length of the economic expansion, the unprecedented duration of the asset recovery, and the potential for overheating conditions. All of this culminates in the question of whether today’s later-stage conditions mean we’re poised for a decline. If we do experience a meaningful deceleration in economic growth, we don’t believe it will be as a result of an overheating economy or because the Fed has overshot in its effort to normalize rates. Rather, we think it will be because of compounding policy mistakes in the area of international trade—specifically the potential for a real, rather than threatened, trade war to commence between the United States and China. If that happens, business confidence would likely begin a prolonged decline that would broadly affect the global economy and supply chains, and that would destabilize the later-for-longer scenario virtually overnight.

Key risk: business confidence falters due to a trade war

The potential for trade disruptions between the United States and China is no longer a temporary risk that can be ignored—even after the supposed détente between the two powers at the G20 meeting in Argentina on December 1. While the threat of worsening conditions in international trade periodically troubled markets in 2018, for some markets, they were more of a sideshow that appeared to resolve itself in unexceptionable recalibrations (e.g., NAFTA reimagined as the U.S.-Mexico-Canada Agreement). For other markets and segments of the global economy, it was more serious. But even with the advent of the recent truce, the threat of deepening problems between the United States and China hasn’t gone away; indeed, the market’s volatile reception of the promise of the truce has underscored that it could be rescinded or violated for a variety of geopolitical reasons—and by either side. This would likely precipitate a much more damaging pause in business confidence that could affect many areas of the global financial markets.

In late 2018, we’ve already seen a foreshadowing of this potential turn of events. We’ve noted a softening of lending among global banks and more widespread concerns about the overall capital investment cycle. While capital expenditure plans for newly tax-advantaged U.S. companies remain expansionary, there’s now hesitation as our covered companies allocate capital. In terms of specific industries, the potential impact of a protracted trade war would be significant for large consumer durables: original equipment manufacturers, auto companies, and recreational vehicle makers. Whereas companies in these areas today may have shown momentum in growing revenue at double digit rates and delivering a return on capital in the area of 20%+, the advent of 25% tariffs on 30% of their components from China—which could still happen if the countries re-escalate trade tensions—would have a contagion-like force.

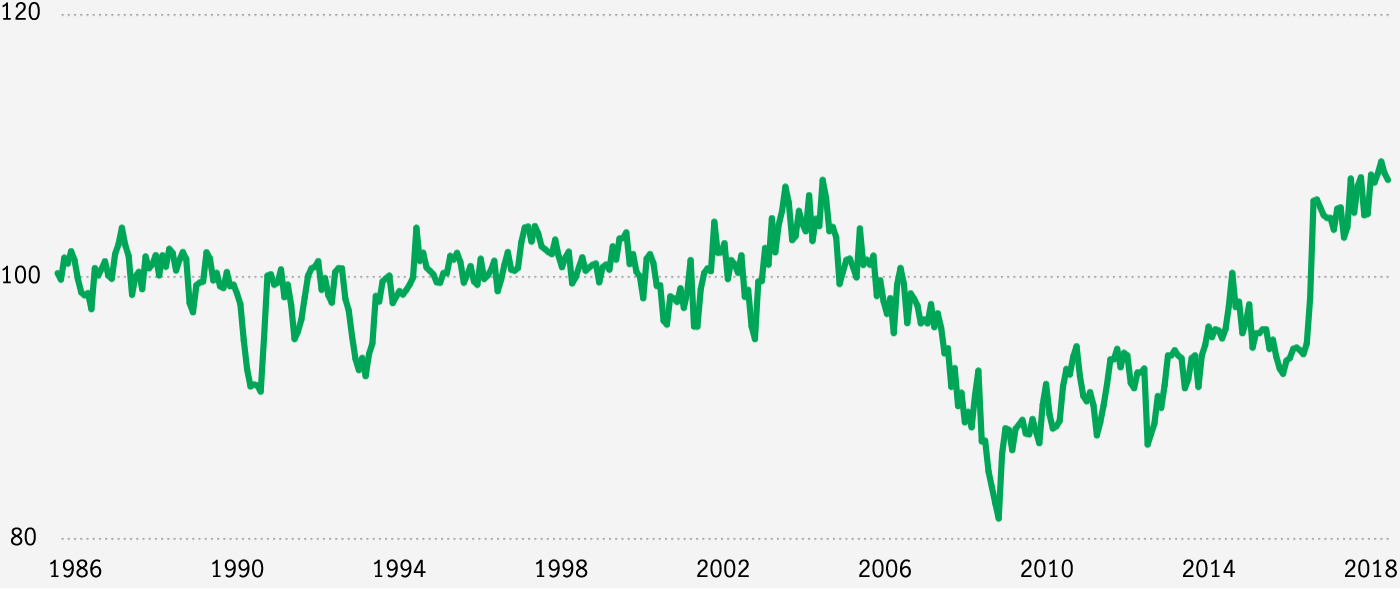

Small business optimism has been strong

Optimism index is based on 10 survey indicators, seasonally adjusted (January 1986–November 2018)

This would affect myriad industries, although the magnitude will differ greatly among disparate industryand company-specific supply chains. Profitability would take an immediate hit if tariffs steepen, as would future business prospects, as a pass through of tariff costs to consumers could easily soften demand. In turn, if these effects are felt across a sufficiently large portion of the economy—and China’s ability to inflict pain should not be underestimated—that would likely exert upward pressure on inflation and interest rates.

It’s academic that neither China nor the United States wants a recession. And it goes without saying that U.S. companies that have built global supply chains over the past decade don’t want tariffs. In general, all sides have an interest in finding a middle ground. The question is whether cooler heads can prevail, particularly when the titular heads (Presidents Trump and Xi Jinping) of both countries aren’t known for—and feel they have a lot to lose by—backing down and making substantive concessions.

Five areas of investment opportunity

While 2019 will be a year for keeping a close watch on international trade, as the trade war headlines may continue to dominate the news flow, we feel confident in pointing out five areas that we consider to have particularly attractive investment opportunities. If the negative theme prevails and business confidence slides, we anticipate that a dispersion of performance results would favor the most fundamentally sound companies in each of these segments. If, on the other hand, the positive theme wins out and the full force of the tailwinds comes into play, we believe winners in each area will be widespread, but led by the highest-quality, most innovative, and best-capitalized names.

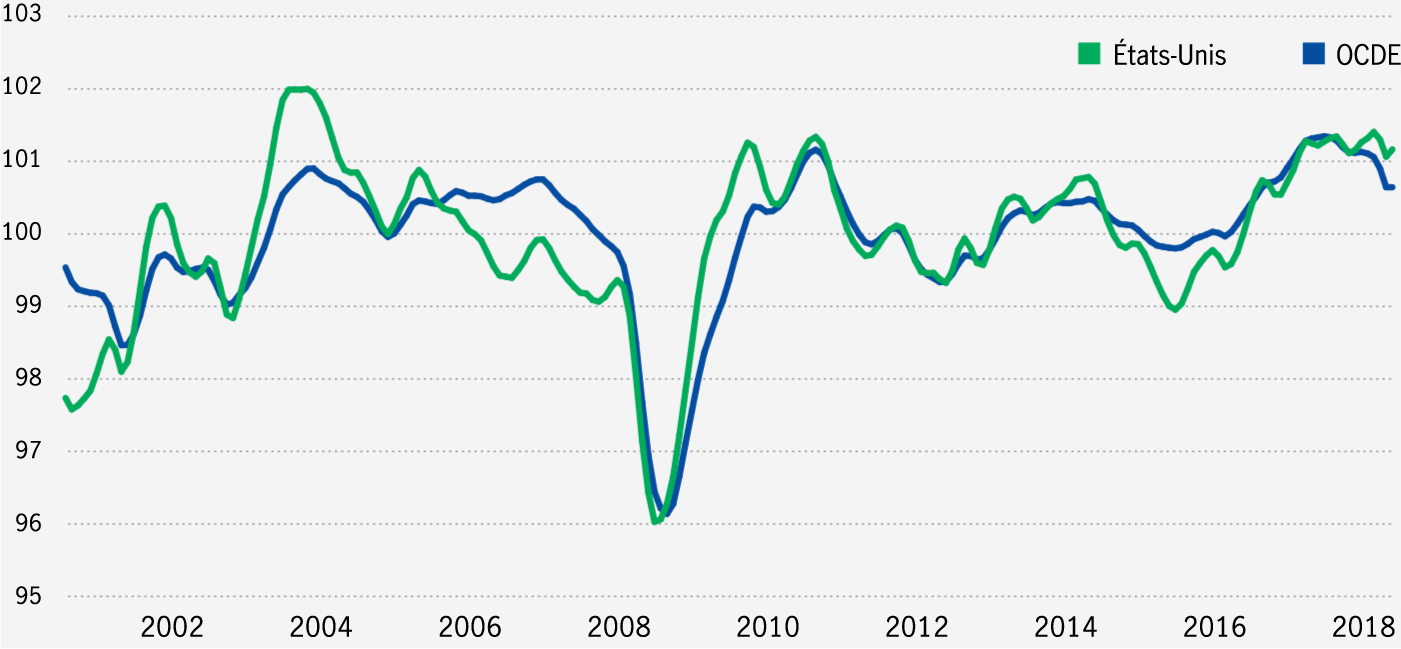

Broader measures of confidence reflect some uncertainty

Business confidence index (January 2000–November 2018)

Five areas of investment opportunity

1 Communication services

Expect digital advertising and media companies to weather the storm over cybersecurity. Well capitalized and still the platform of choice for targeted advertising in the United States, we anticipate these companies will consolidate market share and grow earnings while making steps toward improving oversight and security. The secular trend toward targeted digital advertising and marketing is a powerful and durable one.

2 Financials

Large-cap U.S. banks are better capitalized than they’ve been in a generation. As of early December 2018, we estimate banks are collectively trading at close to 60% of the S&P 500 Index price-to-earnings multiple—which is cheap relative to a historical range of 60% to 80%. We believe their fortress-like balance sheets, credit discipline, and valuations support the sector in the event of a trade war, while at the same time positioning them to participate in any return to more geosynchronous growth. In our research, we also find the biggest banks’ average return on tangible common equity is currently around 15%, which should allow them to compound book value growth at a high single-digit rate while also steadily delivering healthy and growing dividends.

3 Healthcare

The 2019 rebalancing of congressional power should help ensure that the Affordable Care Act remains in place, which should allow certain segments of the healthcare sector to prosper. In the context of an aging global population and pressure to lower healthcare delivery costs, scaled businesses with the ability to optimize patient health outcomes and pricing should do well. Companies with novel drugs and medical products also should remain attractive.

4 Consumer discretionary

The U.S. consumer is confident, employed, has continued to save, and remains underlevered relative to history. Economic growth has been healthy, yet many stocks trade at bear-case values that already discount a U.S. recession. With the millennial cohort aging to the point where it constitutes 40% of the workfore and is entering a credit formation cycle, we believe discretionary businesses that can offer this group online services, housing, and the experiences millennials desire will create economic value.

5 Information technology

Some segments within technology had looked extended before the recent underperformance of cyclicals in the latter months of 2018. But we believe there remains tremendous secular and cyclical opportunity in this sector as it continues to proliferate in our daily lives, and as businesses invest in productivity improvement—cloud services, software, and mobility—as a necessary growth driver in a fully employed U.S. workforce.

Important disclosures

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowed to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers, or employees, shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment, or legal advice. Past performance does not guarantee future results.

This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer, or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeim.com/institutional.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Asset Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. Thailand: Manulife Asset Management (Thailand) Company Limited. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Hancock Capital Investment Management, LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

482103