Asia Pacific REITs: long-term fundamentals should not be overshadowed by short-term flux

The global spread of COVID-19, coupled with a notable deceleration in economic activity, are posing challenges for Asia-Pacific Real Estate Investment Trusts (AP REITs). We believe active, bottom-up fundamental research is more important than ever, especially when constantly changing government policies are leading to short-term price dislocations. Furthermore, the defensive properties of the asset class could make it more resilient in an economic downturn.

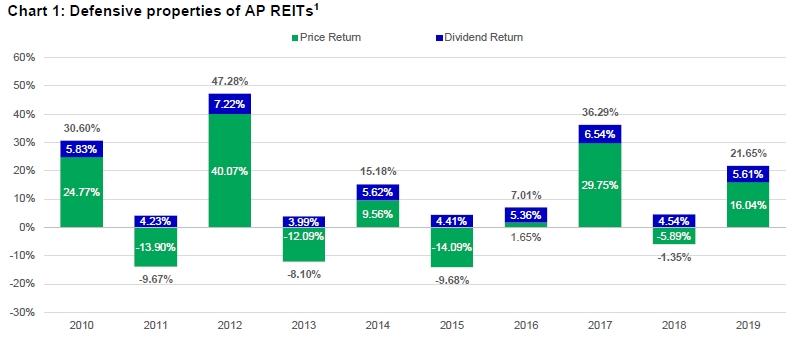

Before discussing the current challenging market environment, it is important to remember why people invest in REITs in the first place. REITs are a hybrid security. That is, even though REITs are traded like equities, with the possibility of price depreciation (loss), they also offer investors a regular income payout. As illustrated in chart 1, the income feature of REITs gives them their defensive properties, providing a buffer when markets move lower and enhancing your total return when markets appreciate.

Drilling into the fundamentals

From an economic perspective, the initial outbreak of COVID-19 led to a notable slowdown in Asian economic activity, centred on China. As time has progressed, the global spread of the virus has raised the spectre of a more prolonged economic downturn, including the possibility of a recession.

In addition to the assorted directives that aim to offset the burden on businesses, governments in the region have introduced various fiscal and monetary policy measures. These policies are constantly being updated given the efforts being made to contain the spread of the virus. This backdrop has created short-term uncertainty and resulted in share-price pressure for REIT managers.

During these times, we believe that fundamentals matter more than ever. Our focus remains on capital strength, the pedigree of the sponsor, and drilling down to the details of lease terms and structure.

We also think that AP REITs are better positioned to face the current economic downturn than they were after the global financial crisis (GFC). Stronger balance sheets mean that the risk of REITs breaching debt covenants is lower, which suggests that the need for dilutive equity fund raising will be minimised.

We believe that AP REITs are more robust in three main areas:

- A decade of low interest rate has reduced the cost of debt in major regional REITs.

- AP REITs have generally locked in financing costs for a longer time period, which has reduced the risks associated with short-term refinancing – an issue that that plagued REITs during the GFC.

- Lower overall leverage ratios and diversified funding sources has also decreased the risk of covenant breaches.

Lower interest rates as key tailwind

Although this economic environment will inevitably pose challenges to AP REITs, particularly in the hotel and retail sectors, as well as REITs with a high exposure to small-and-medium enterprises (SME), we believe the asset class is still better positioned than it was during the GFC.

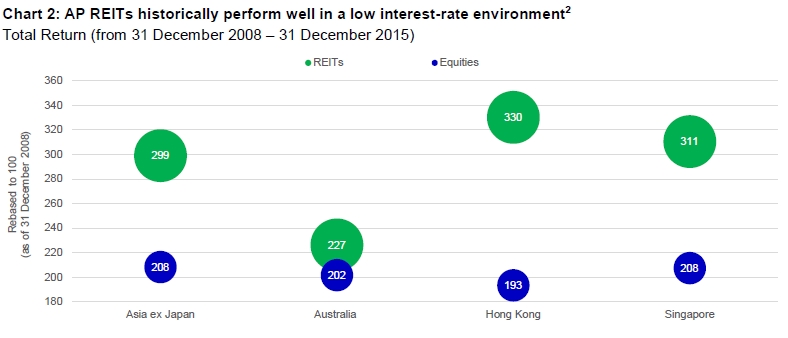

Historically, AP REITs have outperformed equities during periods of low interest rates (see Chart 2), which we have re-entered after the simultaneous demand-and-supply shocks imposed by the global spread of COVID-19.

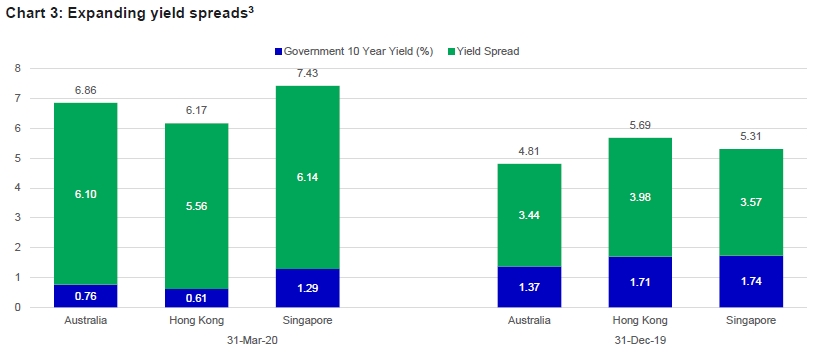

One of the main factors underpinning this outperformance is expanding yield spreads. A yield spread is the difference between the yield on, for example, a risk-free instrument (such as US Treasuries) and the yield offered by other issues. As risk-free rates move lower – they have been aggressively cut over the past month – investors are being compensated more for assuming risk.

Chart 3 shows yield spreads in the key AP REIT markets – Australia, Hong Kong, and Singapore – from the beginning of 2020 through early March: yield spreads have widened in all three, as the risk-free rate has fallen.

We believe that lower interest rates and the global search for yield among investors will continue to support the asset class.

Resilient spots emerge in AP REITs

Although REITs do have qualities that are defensive in nature, we believe that no segment in the REIT space should be considered “recession-proof”.

Given the current economic environment and recent government directives, there will be temporary disruption, particularly in the consumption and tourism-related industries. This has resulted in downward revisions to DPU estimates for 2020. However, we do believe that these revisions have been fully priced into share prices, as yield spreads are trading well above their 10-year averages4.

Investors may find opportunities in the following segments:

Singapore

Short-term dislocation is expected to impact Singapore’s retail sector due to government measures. While this may result in some near-term downside, the long-term fundamentals of the segment remain resilient for the following reasons:

- Retail space per capita in Singapore is lower than several developed markets, which highlights that the market is not yet oversupplied5.

- The government tightly regulates land supply and use. The lower increase in retail space safeguards against oversupply in the market.

- Given population density and the convenience of shopping malls, a physical retail presence is expected to remain highly relevant in Singapore.

Hong Kong

Retail

Hong Kong’s retail sector has battled numerous challenges over the past year, leading to a precipitous fall in retail sales. We believe that the market has priced in a significant amount of negative news flow, and that shopping malls providing necessary goods for consumers should remain resilient in the current challenging economic environment.

Australia

Office

We are constructive on Grade A office space in the Sydney CBD area, as demand is not expected to significantly deteriorate while new supply is forecast to be limited over the next two years.

Industrial

Overall, we believe that third-party logistics and ecommerce providers should digest existing local supply. The increased utilisation of online shopping during the COVID-19 outbreak should be catalyst in this segment.

Conclusion

AP REITs are not immune from the economic fallout from the spread of COVID-19. However, the defensive characteristics of the asset class suggest that investors should benefit from their hybrid nature. At the same time, the fundamentals of AP REITs, including relatively robust performance in low interest-rate environments and an improved financial position, augurs a greater resiliency compared to other investments.

1 Source: Bloomberg, 31 March 2020. 2 Bloomberg, as of 30 November 2019. Gross total returns in US dollar. Past performance is not indicative of future performance. Australia REIT – S&P/ASX 200 A-REIT Index, Hong Kong REIT – Hang Seng REIT Index, Singapore REIT – FTSE ST Real Estate Investment Trusts index, Asia ex Japan REITs = FTSE EPRA/NAREIT Asia ex Japan REITs Index, Singapore Equities = Straits Times Index STI Total Return Index, Hong Kong Equities= Hang Seng Index, Australia Equities = S&P/ASX 200 index, Asia ex Japan equities= MSCI AC Asia Ex Japan index (total return). 3 Source: Bloomberg, 31 March 2020. 4 Source: Bloomberg, 31 March 2020. Singapore REITs = FSTREI Index, 10 year Singapore government bond. Australia REITs = AS51PROP Index, 10-year Australian government bond. Hong Kong REITs = HSREIT Index, 10-year HK government bond (data as of May 2012). 5 CapitaLand Investor Day 2019, 29 November 2019.

513573

Important disclosures

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. Past performance does not guarantee future results. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeam.com.www.manulifeim.com/institutional

Australia: Hancock Natural Resource Group Australasia Pty Limited., Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Asset Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. Thailand: Manulife Asset Management (Thailand) Company Limited. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

513467