Global healthcare: thrust into the spotlight amid the pandemic

2020 was a volatile year for the global equity and fixed-income markets, as the COVID-19 pandemic affected economies across the world. Although global healthcare companies faced their fair share of uncertainties, the sector has demonstrated the ability to address similar clinical challenges with profound health implications. Through the development of diagnostics, therapeutics, and vaccines, healthcare companies worldwide are striving to develop solutions that identify, treat, and contain COVID-19.

In a challenging year, global healthcare equities turned in a resilient performance with solid risk-adjusted returns. Early in 2020, as prevention policies to contain the spread of COVID-19 led to global lockdowns, the outbreak ravaged the world’s economies and the overall market. The healthcare sector offered relative protection during the downturn, once again proving itself as a defensive stalwart. With the pandemic upending everyday life as well as the financial markets, the importance of healthcare came to the forefront.

Scientists, healthcare executives, and government organisations across the world devoted significant time and resources in an attempt to curtail the virus. This led to significant breakthroughs in diagnostic testing, therapeutics, and vaccines. These monumental advancements, along with unprecedented monetary and fiscal stimulus, facilitated economies and global markets to stage a strong recovery throughout the year.

While these COVID-19-related advancements may be unique due to the compressed timeframe, addressing similar clinical challenges with profound health implications is nothing new for these innovative companies. Leading healthcare firms pursue treatments and cures for unmet medical needs every day, including cancer, metabolic syndrome, rare/orphan diseases, and central nervous system (CNS) disorders, to name just a few. Indeed, the ability of healthcare companies to address such unmet medical needs is one of the three guiding principles by which we assess investment opportunity. It also helps shape the sector’s bright outlook.¹

Healthcare’s resilience in volatile markets

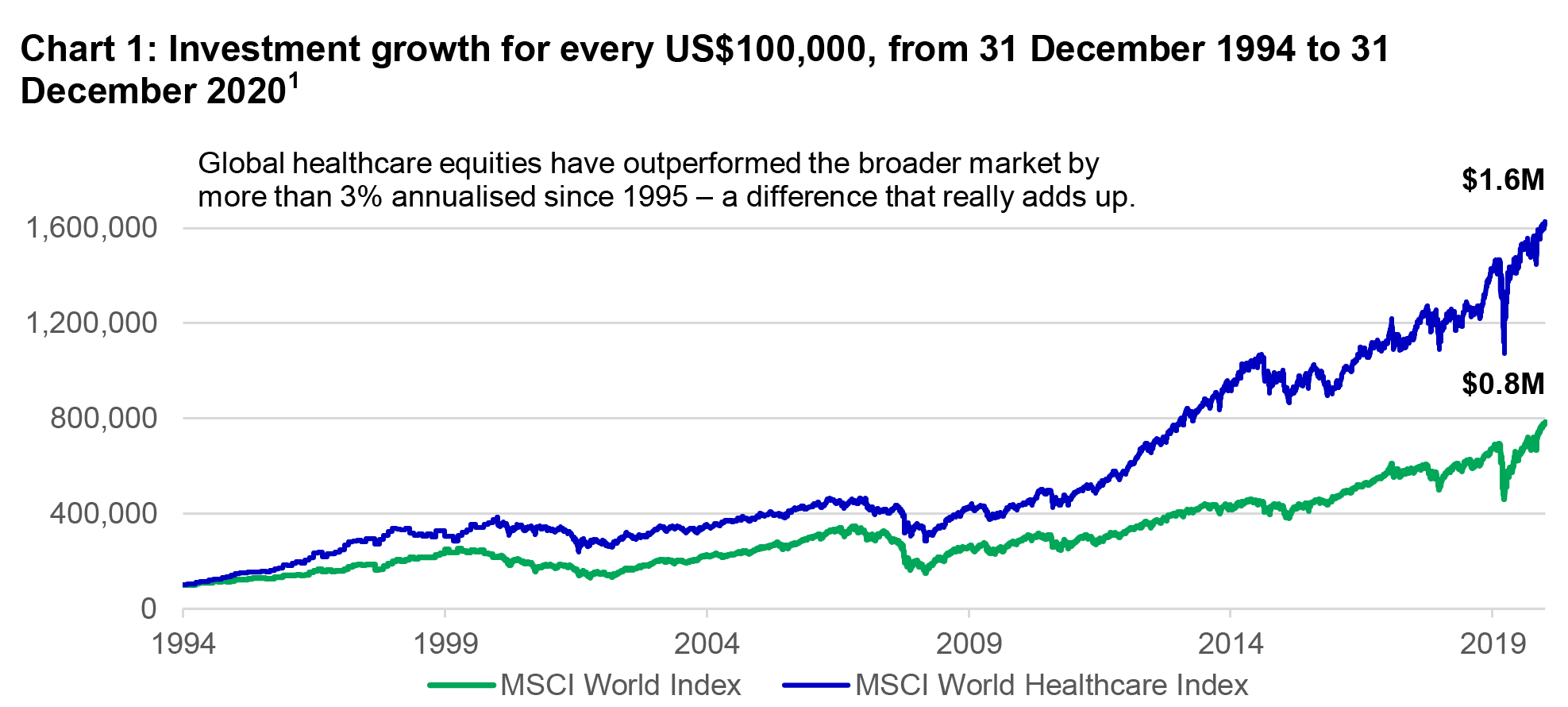

The healthcare sector has historically delivered strong performance, particularly during economic downturns. For more than 25 years (1995–2020), global healthcare equities have, on average, significantly outperformed global equities.

These excess returns have been more pronounced during periods of heightened market volatility and economic distress. The pandemic-induced drawdown experienced in the first quarter of 2020 was no different, with the sector exhibiting its defensive nature and delivering solid excess returns.

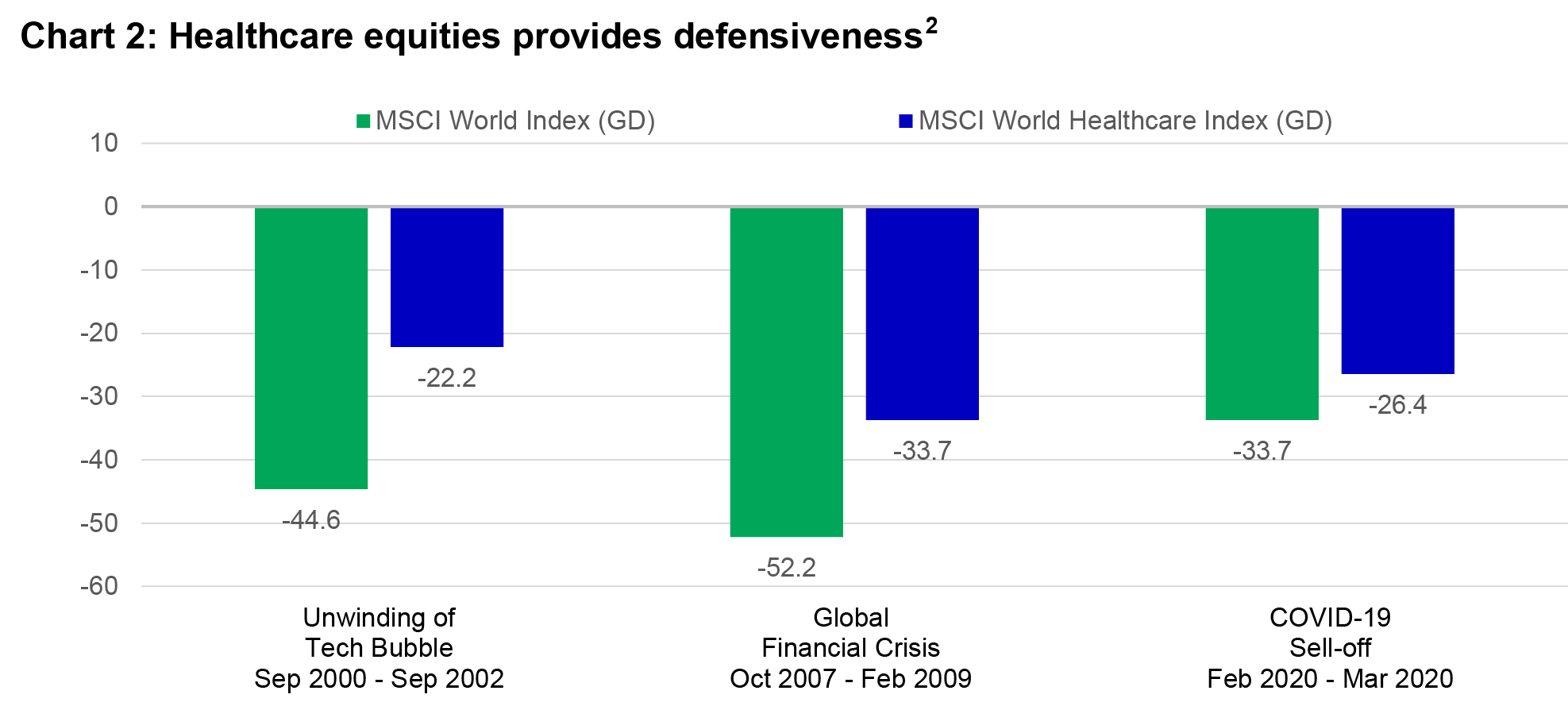

The sector’s defensiveness stems from the supply-and-demand dynamic of healthcare products and services.² While cyclical industries usually experience a sizable reduction in demand during economic downturns, healthcare demand generally remains resilient, with consumers’ needs for medical goods and services being relatively inelastic. This has been even more prominent during the COVID-19 pandemic, with many healthcare products and services experiencing a surge in demand.

Organic growth underpinned by multiple secular drivers

Healthcare is unique in that it’s a defensive sector that provides a buffer to general market volatility while still producing impressive organic growth. This is exemplified by earnings per share and sales growth that have, on average, been historically superior to the broader market.³

This strong organic growth is fueled by long-term secular trends that should propel demand for healthcare products and services higher over the long term, regardless of the global economic cycle.

- The aging population is driving increases in expenditures

Irrespective of location, the world’s population is aging rapidly, and life expectancy is forecast to continue climbing. This should translate into greater demand for health-related services, rising costs, and an expanding array of treatments and therapeutic options.

- Medical advancements

As evidenced by the progress seen with the approvals of COVID-19 treatments, diagnostic tests, and multiple vaccines, medical advances continue to drive the sector forward.

- Profound unmet medical needs remain

As previously mentioned, healthcare companies continue to pursue unmet medical needs beyond COVID-19. These include cancer, metabolic syndrome, rare/orphan diseases, and CNS disorders.

Attractive valuation levels

Healthcare equities are also attractively valued based on forward price-to-earnings (P/E) multiples versus the broader market indexes. Global healthcare companies are currently trading at a discount to the overall market (18.28x vs. 20.56x).³ We think this presents a unique opportunity, as healthcare companies have historically traded at a premium to the overall market as a result of their defensive nature and aforementioned growth prospects.

Valuation metrics (P/E) |

Long-term average³ |

As of February 19, 2021 |

|---|---|---|

MSCI World Healthcare Index vs. MSCI World Index |

106% |

89% |

Source: FactSet, from January 1, 2005, to February 19, 2021.

COVID-19 persistence and the recent U.S. election outcome should provide tailwinds to healthcare equities

Early vaccine efficacy data proved promising and flooded the market with optimism late last year. Although robust data and the strides being made in vaccine distribution are very encouraging, we believe there are still some challenges that the market doesn’t fully appreciate. This view is validated by our proprietary fundamental and scientific research, including, but not limited to, frequent conversations with immunologists/epidemiologists and real-time and detailed reviews of emerging scientific literature, along with dedicated analysis of case reports, hospitalisation data, and mortality data. Given this perspective, we believe the general market is underappreciating the likely duration and impact of COVID-19 on the economy and the healthcare sector.

What’s more, the general population may not fully understand the utility of COVID-19 vaccines. Many common vaccines provide sterilising immunity (protection from infection and transmission). COVID-19 vaccines are estimated at 70% to 95% effective in preventing the disease, depending on the version; however, there’s limited data to suggest that they’re able to stop transmission as well (i.e., sterilising immunity). This, coupled with the various mutations of the virus emerging across the globe (the U.K., Brazil, South Africa), may present further challenges.

The current vaccines may not confer robust levels of protection against these emerging mutants, therefore potentially necessitating the development of booster versions of existing vaccines. Early data also suggests that these variant strains may drive 50% to 70% more transmissions, with extended duration of viral loads found in infected patients.

Due to the reluctance of some individuals to receive the vaccine, the expected time it will take to vaccinate the global population, as well as the vaccine’s inability to provide sterilising immunity, we won’t—according to our research—reach herd immunity as quickly as the general market may anticipate. We believe a therapeutic cure will be necessary to eradicate this virus. We expect the global economy will eventually get back to normal, although it may require several more months (if not years) for that end goal to be realised. As such, investors should position their global healthcare allocations with this thesis in mind. In particular, we believe that some market participants are underappreciating the likely persistent need for breakthroughs in COVID-19 treatments, testing, and vaccines beyond 2021.

Several biopharmaceutical companies with market-leading COVID-19 therapeutic portfolios should warrant investors’ attention. In our view, these companies are expected to see consistently strong demand for their COVID-19 treatments over the next few years, well above street estimates. Specifically, there are established biopharmaceutical companies with approved COVID-19 treatments that have demonstrated utility in shortening infected patients’ recovery time. Select innovative biopharmaceutical companies that are currently developing potential COVID-19 therapeutic cures also present a positive outlook, as our research indicates that an end to this pandemic will likely result from a combination of multiple therapeutics and vaccines. On top of strong COVID-19 tailwinds, we believe this is an area of the healthcare sector that offers reasonable valuations with the potential for further price appreciation.

Additionally, we believe select emerging leaders in the COVID-19 diagnostics space can also offer a unique investment opportunity. For the world to truly open and return to normal (e.g., schools, small businesses, office environment, public events), on-demand and repeated testing will be needed over many months and possibly years. This will drive significant demand for COVID-19 diagnostic testing, and, as such, our proprietary cash flow models for this market segment are forecasting revenues well above sell-side estimates.

Last, we believe investors should pay attention to contract development and manufacturing organisations (CDMOs) with exposure to multiple COVID-19 vaccines, particularly from a risk/reward point of view. We believe that multiple versions of the COVID-19 vaccine will be needed to control this disease, and these CDMOs will be the beneficiaries of persistent sales and profits. In this regard, such companies may well see recurring revenues as the need for booster vaccines becomes clearer.

New U.S. administration

Preceding the U.S. election in November 2020, potential changes to the country’s healthcare system as well as policies surrounding U.S. drug pricing were frequently discussed. Given the outcome of the election, we believe the prospect for substantive U.S. healthcare legislation has been reduced. This should prove to be a positive for healthcare investors due to a lower risk of drug pricing reform or dramatic changes to the healthcare delivery/payment systems in the country. In brief, it seems likely that the new administration will focus on the pandemic to the detriment of any other sweeping changes to U.S. healthcare. Over the short term, we believe that the U.S. government will push for expanded Medicaid coverage and prop up the Affordable Care Act, both legislatively and through executive actions. Accordingly, we’re less sanguine on the likelihood of substantive drug pricing reform in the near to intermediate term; however, we continue to monitor these developments closely.

Governments worldwide seem cognizant of the fact that we’ll be reliant on healthcare companies’ efforts around treatments, testing, and vaccines to move past this pandemic. We expect this circumstance to mitigate any excessive pressure to enact sweeping regulatory changes to the sector.

Long-term implications warrant continued exposure to the healthcare sector

The ongoing COVID-19 pandemic heightens the urgency to effectively manage other preexisting disease states (e.g., cancer, metabolic syndrome, autoimmune disorders). New modalities in treatment and prevention will also continue to drive long-term governmental outlays toward healthcare products and services. Irrespective of COVID-19, the underlying secular trends of aging demographics, medical advancements, and profound unmet medical needs continue to support long-term investment exposure to the sector.

We believe select companies within the healthcare space offer the potential for strong long-term outperformance, and this is an opportune time to invest in the sector, with a focus on the importance of stock selection as a potential driver of outperformance. We believe these innovative and compelling companies have the ability to survive the next market downturn and, more important, create long-term value for shareholders. A bottoms-up, fundamental investment process informed by the assessment of emerging scientific and medical trends, coupled with a disciplined intrinsic valuation analysis, can uncover these robust opportunities. This approach will continue to ensure that an allocation of capital to companies tackling important unmet medical needs will be a key driver of portfolio construction, with deference to appropriate valuation discipline.

1 Morningstar, December 1994 to December 2020. 2 eVestment Alliance, as of February 19, 2021. 3 FactSet, from January 1, 2005, to February 19, 2021.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication and are subject to change based on market and other conditions. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers, or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment, or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment, or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer, or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against a loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams, along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by and are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd., which is authorized and regulated by the Financial Conduct Authority; Manulife Investment Management (Ireland) Ltd., which is authorized and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U). Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G). South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC, and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates, under license.

PPM 531571