Asian equities: greater than the sum of its parts

Despite a challenging 2020 for investors, Asian equities was one of the few bright spots in the global markets. After the COVID-19 outbreak, parts of the region contained the virus more effectively than others, leading to a divergence in economic and stock market performance in the second half of the year. We believe that while Asia (ex-Japan) is tapped to strongly rebound in 2021, divergences should remain, providing investors with attractive opportunities in a region that is greater than the sum of its parts.

The past year posed unprecedented challenges and opportunities for investors. The global outbreak of COVID-19 in the first quarter of 2020 roiled markets and economies alike. Although North Asian economies were the first affected, they were also among the first to effectively contain the spread of the virus, with some managing to avoid entering a technical recession.¹

In contrast, South and Southeast Asian economies were affected later, but due to higher population density and relatively less developed health systems, bore a heavier cost from the pandemic. India and some Association of Southeast Asian (ASEAN) economies, most notably Indonesia, fell into a technical recession for the first time in decades.

Robust fiscal and monetary stimulus globally and in Asia allowed equities to recover, with regional equity indexes posting a nearly 19.0% return,² but with significant dispersion in performance across the region.³

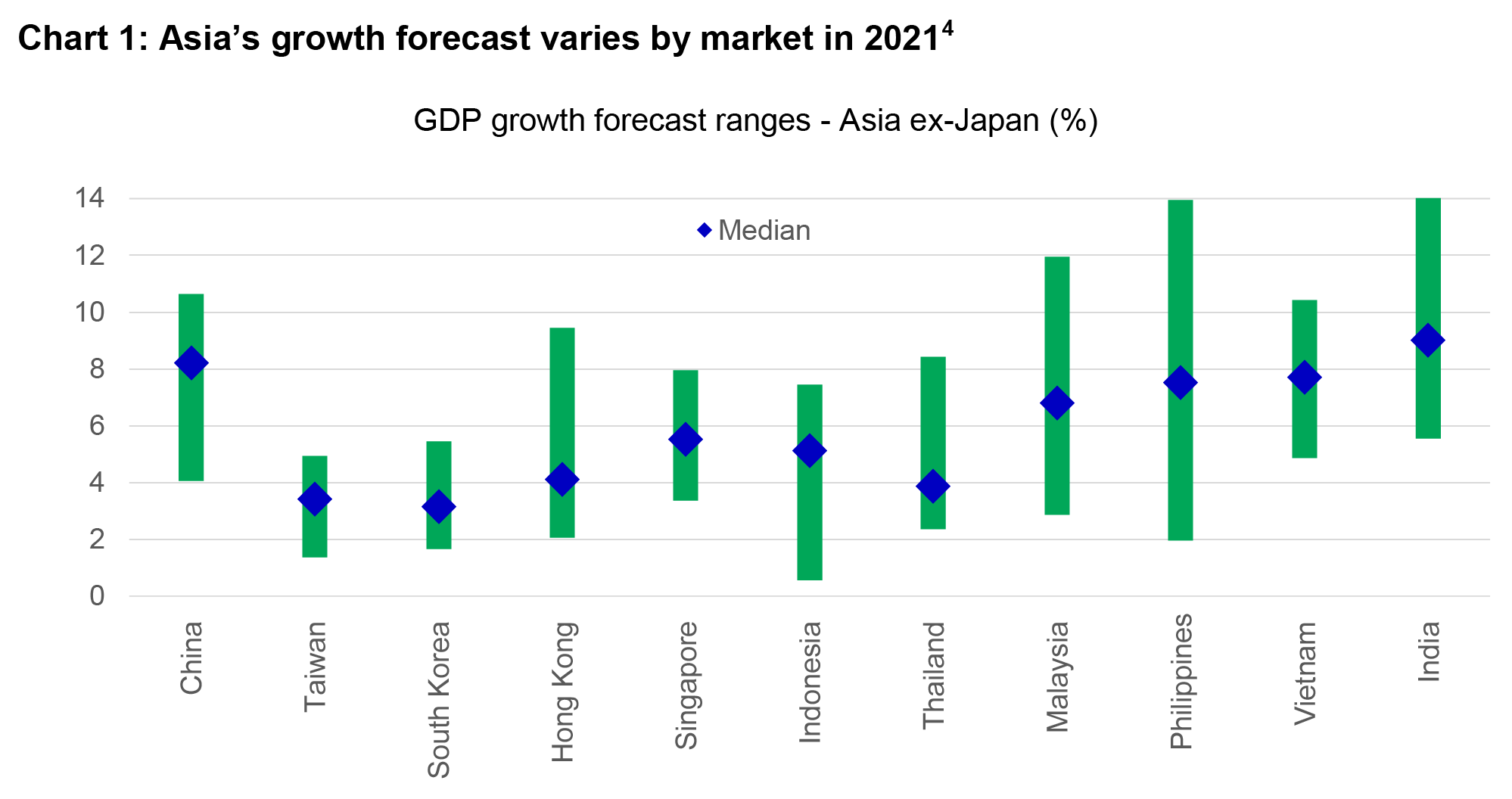

Moving into 2021, the region is tapped to strongly rebound at roughly 5.5% growth overall;⁴ however, this is due to base effects and we anticipate economic recovery to be gradual and uneven due to varied policy responses as well as divergent access and rollout of vaccines in Asia.

Asia: a region of diverse economies and strengths

Before exploring the major regional themes for 2021, it’s important to understand how we view long-term investment opportunities in Asia. Indeed, investors should be vigilant—given the optimistic economic growth forecasts and elevated valuation in some regional equity markets, it’s necessary to understand where sustainable, long-term growth can be achieved rather than a cyclical upswing as economies recover from the shock of COVID-19.

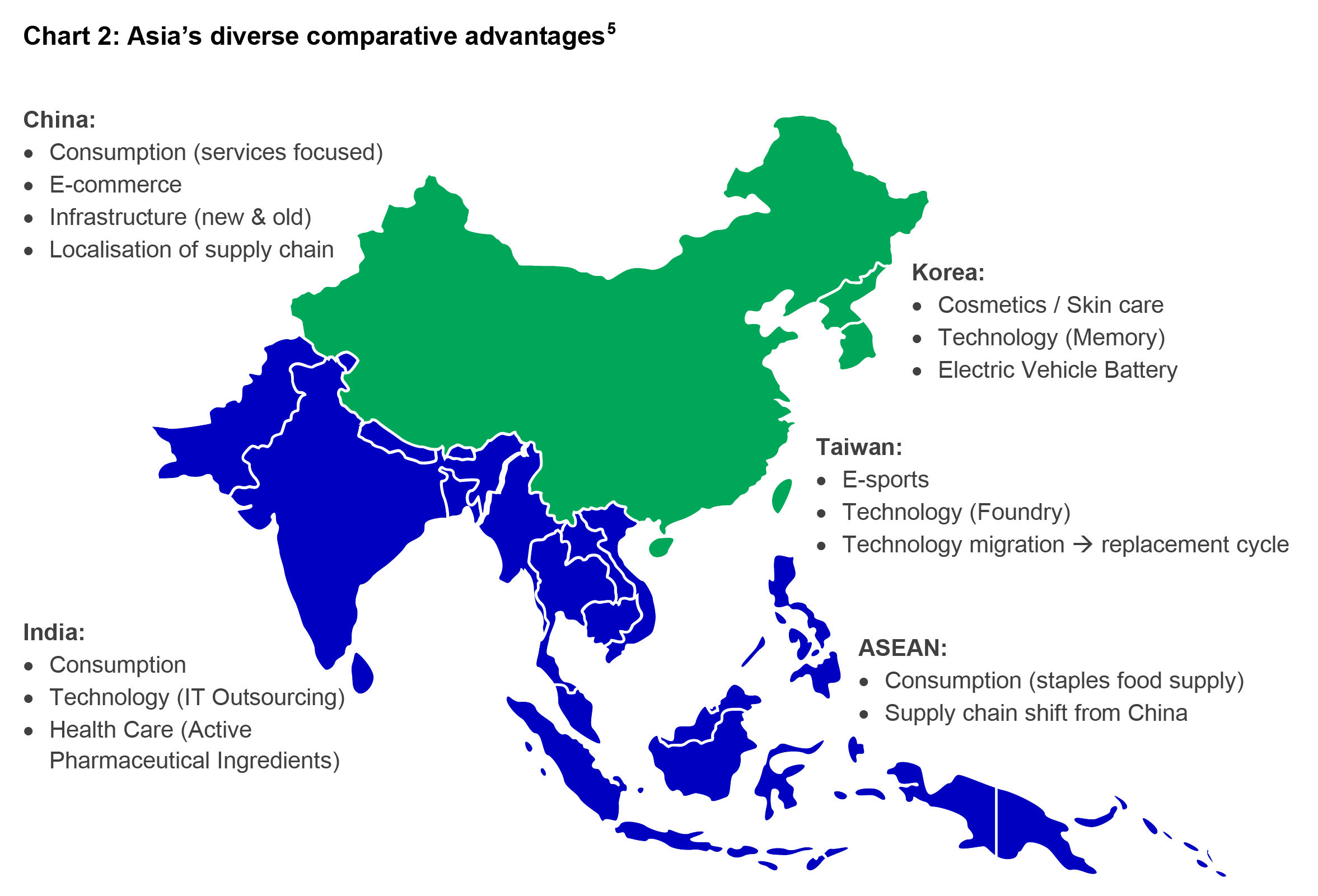

We envision the region as possessing a diverse array of strengths that offer opportunities for investors with different needs.

China: China has adopted a robust policy response in answer to fractious economic relations with the United States that will deepen existing competitive advantages.

The Chinese government’s newest five-year plan (2021–2025) emphasizes cultivating domestic consumption (over exports) and innovation in key strategic technological industries. This should mean continued emphasis on developing already advanced e-commerce and internet platform capabilities. At the same time, the government wishes to develop technology for electric vehicles (EVs) as well as 5G technology to boost the country’s technological base.

South Korea: South Korean companies remain leaders in the memory chip, EV, and renewable energy storage sectors. We believe these companies will be at the forefront of the development and structural growth trend of migration to 5G technology, EV, and renewable energy.

India: We remain optimistic about the outlook of the information technology outsourcing and pharmaceutical sectors. These sectors represent India’s core comparative and competitive advantage globally, and we believe the demand for its products and services is structural in nature.

Over the longer term, we’re closely monitoring the opportunities created by the government’s Make in India initiatives. India has announced several measures aimed at boosting the economy’s self-reliance, including import disincentives, production-linked incentives, tax benefits, and digitization, to increase the manufacturing sector’s share in Indian GDP from 17% currently to 25% over the medium term.⁶

ASEAN: ASEAN countries are strengthening efforts to attract foreign direct investment and deepen their competitive advantages.

Countries in the region possess different strengths. Thailand has a strong automotive supply chain and a well-established food manufacturing industry. Malaysia possesses an advantage in the manufacturing of electronic and electrical products, rubber gloves, and wooden furniture. In contrast, the Philippines provides great service in terms of business process outsourcing, and Indonesia is positioning itself as the hub for the EV supply chain. Finally, Vietnam has established a niche in the manufacturing of smartphones and electronic components.

Taiwan: The technology supply chain in Taiwan is expected to continue to play an important role in supporting technological innovation in China and the United States over the medium term. The ability of local producers in key industries, such as semiconductors, to stay ahead of the technology curve has given them a competitive advantage over their global rivals. Taiwan has also developed world-class companies in servers, 5G components, and integrated circuit design.

2021: structural themes for investors

Based on this vision for Asia, we see the following four structural themes as being critical for investors in 2021.

- Search for (positive) yield leads to Asia

We believe that major central banks will keep interest rates near zero over the short term. With inflation forecast to be in positive territory, this has, and should, continue to result in negative real rates and bond yields in many developed markets.

In contrast, many Asian markets currently offer positive real yields. With a relatively optimistic growth forecast in 2021 for the region, we expect the yield differential between developed markets and Asia to continue in the upcoming year. This dynamic should be constructive for capital inflows into Asian equity markets as global investors look to capitalize on the region’s robust economic rebound and attractive yields.

- Wider adoption of 5G technology

5G technology promises to transform the 2020s into a time of unprecedented connectivity and technological advancement, dramatically expanding the reach of the Internet of Things (IoT). Indeed, 5G and IoT will enable greater usage of connected devices that automate onerous business processes. This includes factory automation; many manufacturers have announced their plans to automate their factories to overcome the issues of labor shortages and enhance productivity.

We expect broader availability of devices developed with 5G to be launched in the next few years. This is expected to trigger a replacement cycle globally and we believe the supply chain in Asia, particularly the tech supply chain in North Asia (Taiwan, China, and South Korea), will benefit from this trend.

- Greater focus on climate change and sustainable development

With the risks of climate change becoming more apparent, countries are adopting ambitious policies to address the problems.⁸ These initiatives coupled with greater attention to environmental, social, and governance factors in investment decisions should lead to more climate-friendly and sustainable projects, such as renewable energy infrastructure and equipment. As a result, we envisage that the development and adoption of EVs and energy-efficient products should accelerate as well as the ecosystem of renewable energy and resources, such as energy storage, battery charging stations, energy-efficient semiconductors/chips, and recyclable materials. Investments in this area are expected grow significantly.

- More diversified China+1 sourcing strategy⁹

Global supply chains, and China’s role in them, have undergone significant changes due to the global spread of COVID-19 and the fallout from the prolonged China-U.S. trade conflict. Some firms may shift production out of China (production relocation) on concerns over the vulnerability of single production location or rising tariffs. Others might choose to diversify customers and redirect exports to other markets (trade redirection) in light of geopolitical risks. Southeast Asian countries, particularly Vietnam, have benefited from multinational and Chinese companies relocating or setting up new factories in the region. We expect this trend to continue, and governments in Southeast Asia have introduced incentives and amended regulations.¹⁰

Conclusion

Although parts of Asia have fared better than others after the global shock of COVID-19, the road to recovery—both physical and economic—should remain a key theme of 2021. For long-term investors, Asia offers the opportunity to not only participate in sustainable growth in world-class companies, but also to achieve diversification through exposure to different industries. Overall, the region’s opportunities add up to more than the sum of its diverse parts.

1 China and Taiwan didn’t enter a technical recession, while Hong Kong and Korea did. 2 Bloomberg, as of December 29, 2020. MSCI Asia (ex-Japan) posted a return of 21.84% (total return in U.S. dollars). 3 Bloomberg, as of December 29, 2020. MSCI Korea was the best-performing regional market index, up roughly 40.30% (total return in U.S. dollars), while MSCI Thailand was the worst-performing market index, declining by 10.79% (total return in U.S. dollars). 4 Bloomberg, December 15, 2020. 5 Manulife Investment Management. 6 Goldman Sachs, as of November 15, 2020. 7 Bloomberg, as of November 30, 2020. 8 In a September speech to the United Nations, Chinese President Xi Jinping put a 2060 end date on his country’s contribution to global warming. President-elect Joe Biden has also pledged to rejoin the Paris Agreement after being sworn in on January 20, 2021. 9 A China+1 sourcing strategy typically refers to supply chain management strategy where firms opt to diversify risks by establishing a factory in China, and another in a developing economy in Southeast Asia, such as Thailand or Vietnam. 10 Indonesia recently passed the Omnibus Law, while India passed the Production Linked Incentive.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. Past performance does not guarantee future results. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeim.com/institutional

Australia: Hancock Natural Resource Group Australasia Pty Limited., Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland. Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance

528487