India’s path to economic recovery

India hasn't been spared from the global damage caused by the COVID-19 pandemic, with the country’s lockdown contributing to a precipitous drop in economic activity.

However, we believe that the worst is likely behind us; the slowdown in growth is bottoming out, government policies remain supportive, and virus-related health metrics are stabilizing. Despite the setback, India should benefit from a path of economic normalization in the short term and an acceleration of existing structural drivers—such as formalization and government reinvestment—over a longer timeframe.

Our consistent view on India, even before the COVID-19 outbreak, was that the economy faced a cyclical downturn driven by a deceleration in the informal economy and a credit slowdown among the nonbanking financial companies due to tighter monetary conditions.

While we had expected an economic recovery in the first half of 2020 on the back of policy support from the three Rs,¹ the pandemic and the subsequent government lockdown stifled any upturn. Consequently, second-quarter GDP fell by approximately 24% year over year.

Despite this sharp dip in growth, GDP is a backward-looking number, reflecting the damage of the strict lockdown implemented in India until June. Since then, the economy has gradually reopened, and many activities are normalizing. In our view, the worst is likely behind us for three reasons:

- The adverse economic conditions have bottomed out.

- Monetary conditions remain benign due to supportive flows and supportive policies.

- A more stable COVID-19 situation

These factors augur well for an ongoing rebound in activity and a sequential improvement in economic data. While the upcoming recovery is expected to be uneven, we remain positive on India’s medium-term growth potential since formalization should continue to boost the digital economy, and the government’s reinvest policies should herald a revival in manufacturing.

The decline in growth has bottomed out, and will likely improve

We believe that the decline in GDP growth has bottomed out, and we should see sequential improvements going forward. In fiscal year 2022,² we expect double-digit growth in real GDP. However, the recovery will remain uneven across sectors and geographies. That said, with most urban centers now operating almost normally, our confidence in a resumption of activity has subsequently increased.

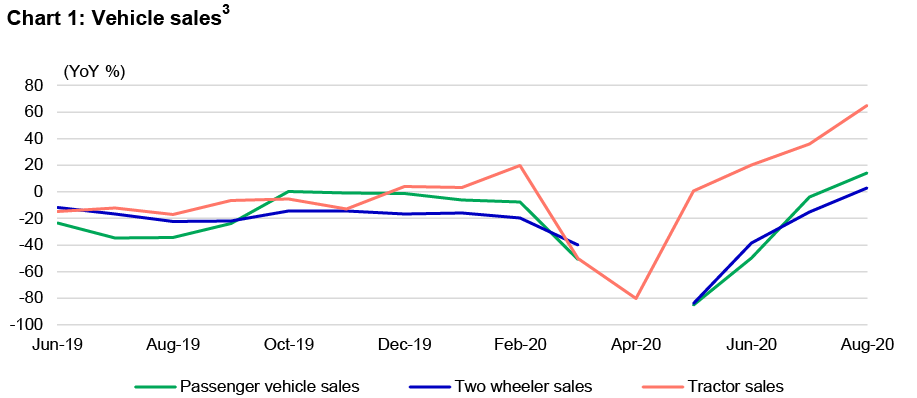

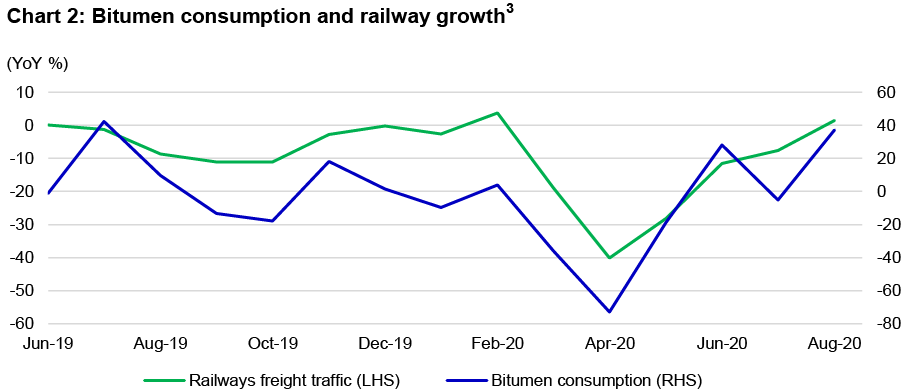

Many bottom-up indicators on demand and supply support this thesis. Vehicle sales across all categories have improved. In addition, a rise in demand for bitumen points to a pickup in the construction sector, while positive rail freight growth signifies that industrial activity has also started to normalize, albeit gradually.

Monetary conditions are benign

Divergence in monetary conditions is the critical difference between the earlier cyclical slowdown and the postpandemic recovery phase. The Reserve Bank of India (RBI) has aggressively cut rates by 115 basis points since March 2020. It has also provided the banks with additional long-term repo operation and targeted long-term repo operation liquidity (roughly 4.5% of GDP) at this lower policy rate. It's also continued to intervene in the bond market to ensure that it functions smoothly.⁴

Domestic monetary conditions have also improved, as India’s external account situation remains favorable: The capital and current accounts are in better health, with the country’s balance of payments in surplus. From a current account perspective, this is primarily due to a rising share of net exports in electronics and chemicals as well as falling crude oil prices. Robust inflows are driving the capital account recovery in foreign direct investment and foreign portfolio participation in India’s digital economy and manufacturing revival. As a result, India’s foreign-exchange reserves increased from US$457 billion in December 2019 to US$541 billion by the end of August 2020.⁵

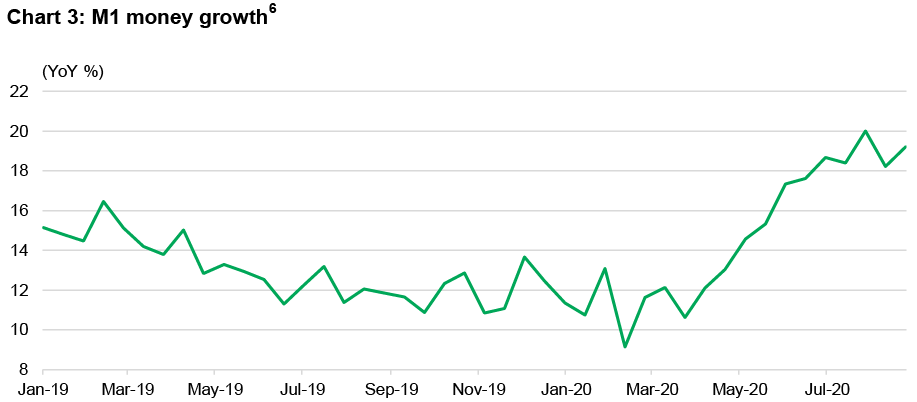

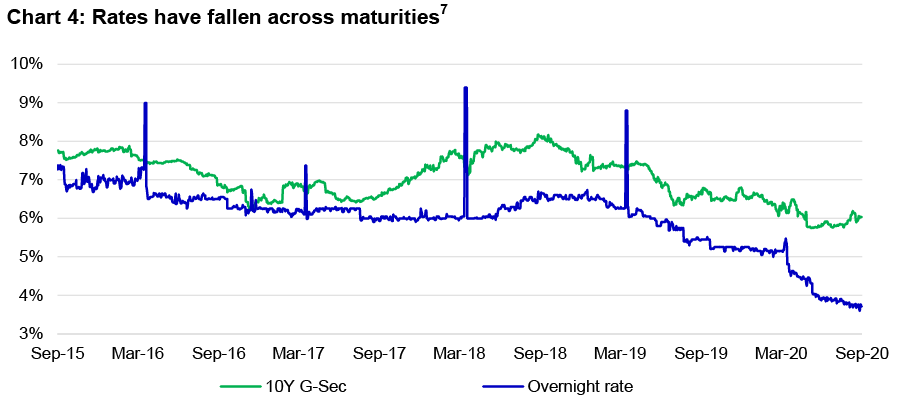

Benign liquidity conditions are reflected in money-supply (M1) growth and lower rates on both the short and long end of the curve. In fact, real rates are now in negative territory for the first time in five years.

While we expect credit costs to rise from these levels, they won't be debilitating for the banking sector due to lower rates and ample liquidity. An active and vigilant RBI is likely to prevent any systemic refinancing issues. Most major private banks have also raised capital recently, and their balance sheets are adequately capitalized.

Overall, we expect the credit-transmission mechanism to pick up. This will be driven by a gradual reopening of the economy, the containment of asset-quality deterioration, and the well-capitalized balance sheets of the large private-sector banks. It's worth noting that nominal rates and negative real rates are also lower.

Finally, we don't anticipate any substantial depreciation in the value of the rupee, as better capital flows will help to revive growth. In addition, we don't believe that India's trade deficit will expand meaningfully, as the share of domestic manufacturing has improved and should continue to do so.

Confidence in an economic reopening is rising

Beyond the headlines about the high number of confirmed cases of COVID-19 infections, there are a few positives to take away from the pandemic situation in India: Case recoveries have notably increased over the past three months, while mortality rates have declined—this has brought the curve of active cases under control. Since July, these factors have combined to increase confidence among the government and the people to resume economic activity, even as cases continue to rise at the headline level.

Overall, despite rising infection numbers, we also sense that the COVID-19 situation is stabilizing. Our base case doesn't foresee any further national lockdowns.

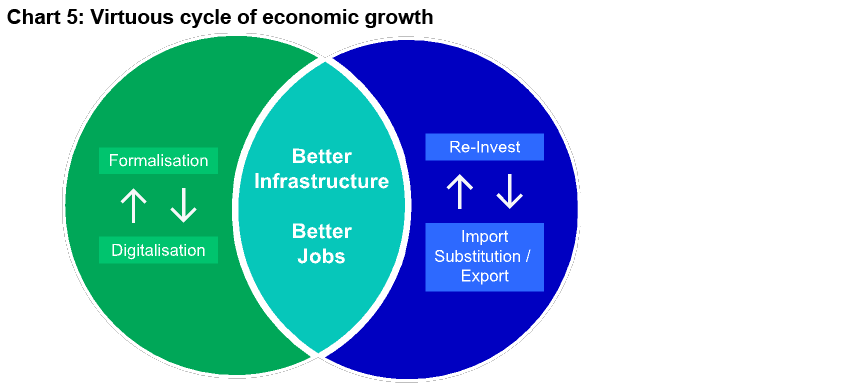

Economic formalization and reinvestment should drive growth

Over the short to medium term, we retain an optimistic cyclical view based on the gradual reopening of the economy. From a mid- to-long-term perspective, we're positive on the structural economic changes driven by the powerful themes of formalization through the digital economy and reinvestment in manufacturing. If anything, the pandemic has accelerated these trends; companies across sectors—from consumer staples, retail, healthcare, media, banking, financial services and insurance, and even automobile companies—have launched innovative digital platforms to engage with customers and find new ways to catalyze revenue growth. These developments have the potential to feed off each other and create the kind of virtuous cycle we’ve seen in China and other East Asian economies.

On the one hand, economic formalization is driving the growth of India’s massive digital economy. In turn, the digital economy is itself propelling the formalization process by boosting productivity.

We also believe that manufacturing growth is at an inflection point, led by the government’s supportive reinvest policies (through incentives and tax cuts for domestic production) and a conducive global environment, specifically international firms that are looking for a supply base outside of China. We've already seen a significant amount of investment by international firms, and believe this structural trend should continue to attract global capital to India, helping the country realize its potential.⁸

As formalization grows, government revenues should increase, which in turn will lead to higher spending on infrastructure. As manufacturing expands, the creation of more formal jobs will drive income growth and consumption, thereby unleashing a virtuous cycle. Together, these themes will serve as strong drivers over the medium term, notwithstanding the recent cyclical challenges.

So far, fiscal stimulus measures announced in response to the pandemic have primarily focused on liquidity (roughly 4.5% of GDP) and credit-guarantee measures (approximately 2.0% of GDP).⁹ There has been less of direct fiscal impulse (about 1% of GDP)9. Fiscal measures have focused instead on the provision of basic foodstuffs and income to the most vulnerable sections of society. It's possible that the government may announce additional fiscal measures when the economy is operating at a higher utilization level to ensure those measures will have a better multiplier impact.

More importantly, the government has concentrated its policy efforts on catalyzing a longer-term manufacturing revival and increasing import substitution. These range from introducing additional duties on imports and investment-linked incentives, as well as long-needed simplification of labor laws to improve the ease of doing business in India and incentivize more domestic manufacturing which is in line with the government’s reinvest policies.¹⁰ The aim is to boost domestic manufacturing in sectors such as chemicals, active pharmaceutical ingredients, mobile phones, and consumer durables.

Such moves should lead to an increase in fresh investment leading to a recovery in the capital-formation cycle, improvements in employment opportunities, and gains in net exports for India.

Our latest sector views

Based on these changes in the Indian economy, we've updated our sector views.

More constructive on:

- Financials: We expect banking asset quality to remain under control, as large private banks have raised capital to strengthen their balance sheets, and the RBI has actively intervened in the market to prevent systemic issues. The outlook for financial services is positive because the sector benefits from higher spending through the formal channels—such as digital (e.g., credit cards)—and a revival in car and housing sales (e.g., general insurance).

- Consumer discretionary (auto, apparel, and food services): The recently concluded earnings season, which saw the sector deliver better results, showed that many consumer-related companies implemented impressive cost control. As the recovery gathers pace, many of these firms should operate with greater efficiency. We should also see auto companies do well as consumers opt for personal mobility over public transport to maintain safe social distancing.

- Materials: This is a play on both a resumption in industrial activity in India, through cement, as well as global recovery through metals.

- IT services: The sector continues to benefit from faster digital transformation initiatives, as companies across the globe try to reimagine their business models and processes in response to the pandemic.

- Structural themes: We're still constructive on macro themes, such as import substitution plays that benefit from the Indian government's policy of encouraging domestic manufacturing (e.g., electronic manufacturing services companies, auto ancillaries), and the gradual diversification of production away from China due to the trade war (e.g., specialty chemicals and pharma).

Less constructive on:

- Communications services and consumer staples where valuations have rerated ahead of growth expectations, as they were seen to benefit from the lockdown.

The key risk to our view remains a second wave of infection in India, pushing up the active case growth curve and new lockdowns.

1 The three Rs are: recycle (privatization of state-owned enterprises), rebuild (tax cuts to corporates and middle-income households), and reinvest (a lower tax rate for investments on the ground). 2 The period from April 1, 2021, to March 31, 2022. 3 CEIC, Kotak Institutional Equities, as of September 12, 2020. The April 2020 data for passenger vehicles and two-wheelers wasn't released by the Society of Indian Automobile Manufacturers. 4 GDP estimates were calculated by Manulife Investment Management. The remaining analysis is sourced from the Reserve Bank of India, as of August 31, 2020. 5 Reserve Bank of India and Bloomberg, as of August 31, 2020. 6 Bloomberg, as of August 28, 2020. 7 Bloomberg, as of September 15, 2020. 8 “$20 billion and counting! Investments attracted by India in 3 months during Covid-19,”, www.timesnownews.com, July 16, 2020. 9 Manulife Investment Management estimates, as of September 21, 2020. 10 “Labour reforms intend to put India among top 10 nations in ease of doing business,” The Economic Times, September 22, 2020.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication and are subject to change based on market and other conditions. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers, or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment, or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment, or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer, or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against a loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams, along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by and are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd., which is authorized and regulated by the Financial Conduct Authority; Manulife Investment Management (Ireland) Ltd., which is authorized and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U). Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G). South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC, and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates, under license.

PPM 523361