Asian bond markets reach a tipping point

Key takeaways

- Taken together, ex-Japan, the Asian bond markets have grown rapidly over the past decade, driven by improved credit ratings and economic performance, along with a surge in new issuance.

- China’s bond market is positioned to receive a major injection in inflows as the country becomes eligible for inclusion in global bond indexes in Q2 2019.

- High relative yields, low correlation to other bond markets, and the rise of Asian-based institutional investors are some of the reasons we believe investors may push Asian bonds into global prominence in the year ahead.

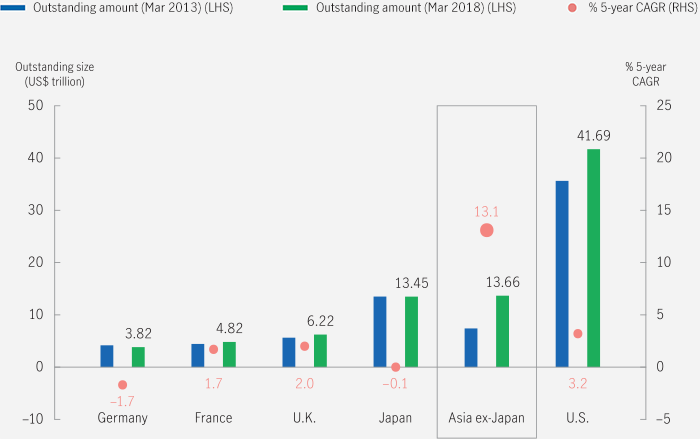

Over the past decade, the Asian bond market (which includes primarily local currency bonds but also U.S. dollar, or USD, bonds) has grown rapidly to become one of the largest regional bond markets in the world, with an estimated size of US$13.7 trillion. While still smaller than the U.S. bond market (which remains the world’s largest at US$41.7 trillion), the Asian bond market ex-Japan has already overtaken its Japanese counterpart, expanding at a compound annual growth rate of 13.1% over the past five years—outpacing all other regional bond markets.¹ The region’s USD credit market, in particular, has grown more than fivefold over the past decade and is fast approaching US$1 trillion in market value.²

The Asian bond market has significantly grown over the past five years

Source: Bank for International Settlements (BIS), Asian Development Bank, European Central Bank, Bloomberg, 2018. All amounts outstanding by residence of issuer. Manulife Investment Management, as of March 31, 2018. Asia ex-Japan includes China. CAGR stands for compound annual growth rate. LHS refers to left-hand side, RHS refers to right-hand side.

Although Asian countries and territories are at different stages of economic development, the region is still largely considered an emerging market (EM) and holds significant weight in EM bond indexes. Today, Asia accounts for the largest regional weight (60.7%) in the J.P. Morgan Government Bond Index-EM Broad Index, indicating the region’s dominance within the world of EM.³ The continent also occupies an increasingly important position within the EM credit space, accounting for nearly 45% of the Corporate Emerging Bond Index, which is priced in USD.⁴

An eye on China: an emerging bond market with vast potential

The growth of China’s onshore bond market is one of the key regional developments in the past decade. The market has doubled in size—growing at a compound annual growth rate of 16.6% over the past five years alone—to become the world’s third largest.⁵

Despite rapid growth, we believe the market remains underdeveloped; specifically, foreign participation remains relatively low. However, this is gradually changing due to growing investor interest, partly as a result of China’s inclusion in major global bond indexes, as of Q2 2019. As much as US$600 billion of passive funds could flow into the Chinese bond market as a result of index inclusion.

“As much as US$600 billion of passive funds could flow into the Chinese bond market as a result of index inclusion.”

We believe onshore Chinese bonds should be considered by global investors for numerous reasons: their attractive yields, China’s strong A+ sovereign rating, and their unique diversification benefits due to China’s monetary policy cycle running differently from G10 countries and demand being driven by its domestic investor base.

Foreign investment in China’s bond market doesn’t match its global economic power

A stable and local ownership base

Asian institutional investors are key buyers in the region’s USD bond market, providing a stable ownership base for the asset class. Ownership of USD bonds originating from the region among Asia-based investors has risen from 56% to 79% in just five years. In contrast, the share of U.S. and European investors participating in new Asian USD bond issues dropped from 44% to 21% over the same period.³

The rise in Asia-based investors is significant, as they can act as anchors and help to reduce volatility in times of market stress. This, we believe, goes a long way to explaining why volatility among Asian corporate bonds—on a three-year rolling basis—is lower than that seen elsewhere within the EM universe.⁷

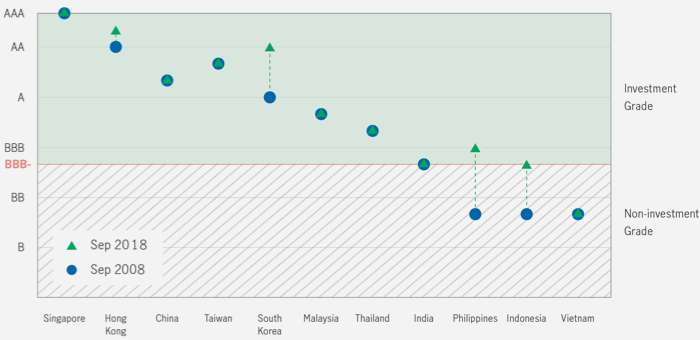

Improved credit ratings track economic performance

Asia’s increased prominence in global fixed-income markets is due to the region’s improved credit ratings and dynamic economic performance. Indeed, with the exception of Vietnam, almost all Asian countries and territories boast investment-grade sovereign ratings and are generally higher rated than other EM regions and many EM stalwarts, including Brazil (BB–), South Africa (BB+), and Turkey (BB–).⁷

Burgeoning foreign exchange reserves partially explain the disparity in credit ratings. The total foreign exchange reserves for Asian countries (US$5.7 trillion) far exceed the combined reserves for countries in Latin America (US$834 billion) and EEMA (US$2 trillion).⁸

The total foreign exchange reserves for Asian countries far exceed the combined reserves for countries in Latin America and EEMA.

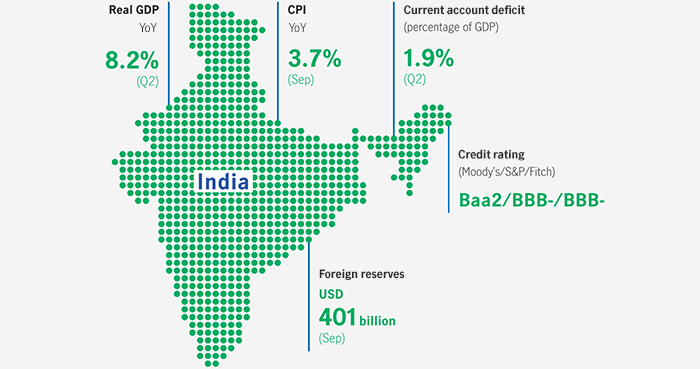

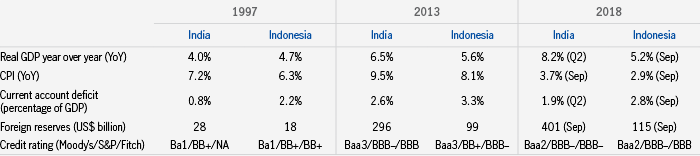

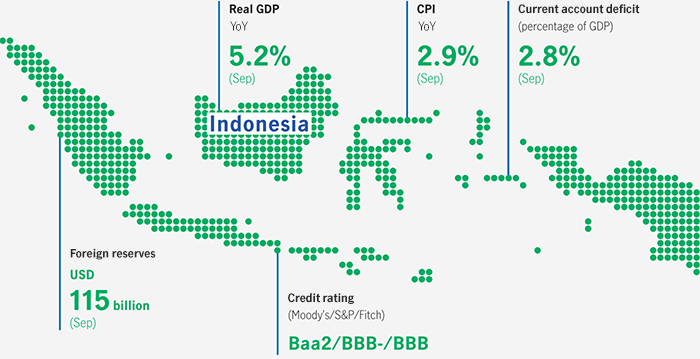

EM in general has experienced a challenging year in 2018, largely a result of rising U.S. interest rates and a stronger USD. Nonetheless, we remain constructive on emerging Asia for the medium term. Indeed, in contrast to the 1997 Asian financial crisis, countries such as Indonesia and India have since adopted a more proactive approach to monetary policy to help navigate market volatility. Indonesia, for example, has raised rates six times in 2018, while India has lifted rates twice. As economic fundamentals for both markets remain sound, we believe the currencies and bonds of these two countries hold significant upside potential, which may unlock once sentiment improves for EMs.

Credit ratings have trended upward over the past 10 years

Improving economic fundamentals in India and Indonesia over time

Source: Bloomberg, World Bank, as of September 30, 2018.

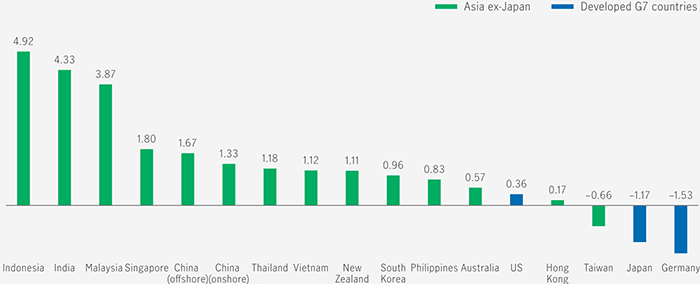

Attractive real yields provide tailwinds

Real yields are commonly used to assess prospective bond investments. The real yield is simply the nominal yield of a bond (at a given point in time) less the annual inflation rate. We believe it’s important to consider real yields, particularly for EM, as the nominal yields may be misleading: High inflation rates can mean investors actually earn a negative return once inflation is factored in.

The cases of Indonesia and India are particularly worth noting. Ten years ago, while both countries offered high nominal yields, monetary policies in both countries were also relatively inefficient, which meant higher rates of inflation and lower real yields. Today, we believe both countries have more effective monetary frameworks, driving their bonds to the top of the return table. Of note, Indonesia raised interest rates several times in 2018 to protect its currency amid increased financial volatility, while India also raised rates to stem inflationary pressures. Today, the two countries offer the highest real yields in Asia.

Finally, investors may also note the range of yields available across different markets in Asia. China and Malaysia, which are both currently A+ rated, can offer attractive real yields given their strong ratings, while mature markets such as Singapore and South Korea, which today are rated AAA and AA, respectively, can still offer competitive, positive real yields above those of similar developed markets. With many real yields in developed markets offering negative returns (such as Japan and Germany), investors are turning to Asia for higher yields.

Real yields of major global bond markets ex-Japan

1 Bank for International Settlements, Asian Development Bank, European Central Bank, Bloomberg, as of March 31, 2018. 2 J.P. Morgan, as of September 30, 2018. 3 J.P. Morgan, as of September 30, 2018. The J.P. Morgan Government Bond Index—Emerging Market (EM) Broad Index tracks the performance of local currency EM government bonds. 4 J.P. Morgan, as of September 30, 2018, total market value of the CEMBI with a market value of US$223.5 billion. The Corporate Emerging Market Bond Index series (CEMBI) track U.S. dollar-denominated debt issued by emerging-market corporations. 5 Asia Development Bank, as of March 31, 2018. 6 Bloomberg Barclays announced that it will add Chinese RMB-denominated government and policy bank securities to the Bloomberg Barclays Global Aggregate Bond Index. The inclusion will be phased in over a 20-month period starting April 2019. When the exercise is complete, the index will include 386 Chinese securities, representing 5.49% of the index based on data from January 2018. 7 Manulife Investment Management, Bloomberg, as of September 30, 2018. 8 Bloomberg, S&P local currency long-term rating, as of September 30, 2018.

Important disclosures

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowed to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers, or employees, shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment, or legal advice. Past performance does not guarantee future results.

This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer, or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeim.com/institutional.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Asset Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. Thailand: Manulife Asset Management (Thailand) Company Limited. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Hancock Capital Investment Management, LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.