China fixed income: a safe haven asset in uncertain times?

The COVID-19 outbreak has created an increasingly uncertain outlook for the global economy, accompanied by extreme market volatility. In response, central banks have introduced massive stimulus measures to help counter the swift decline in financial markets. How did China’s bond markets fare during the market sell-off?

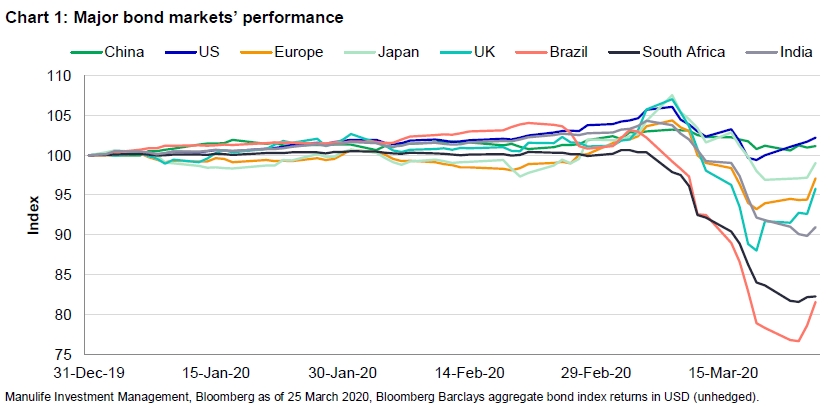

How have China bonds performed year-to-date?

Aggregate bonds in China and the United States are the only two major fixed-income markets to deliver positive returns this year. As of March 31, U.S. aggregate bonds were up by 2.23%, while China’s aggregate issues were up by 1.14%.¹

Over the same period, Chinese government bonds returned 0.93%, while Chinese corporate bonds have risen by 0.22%.² In local currency terms, China’s aggregate bonds were up by 3.02%, with the country’s government bonds gaining 2.81% and corporate bonds moving 2.08% higher. The renminbi (RMB) depreciated by 1.24% against the U.S. dollar (USD) during this time.

Volatility and correlations remain low

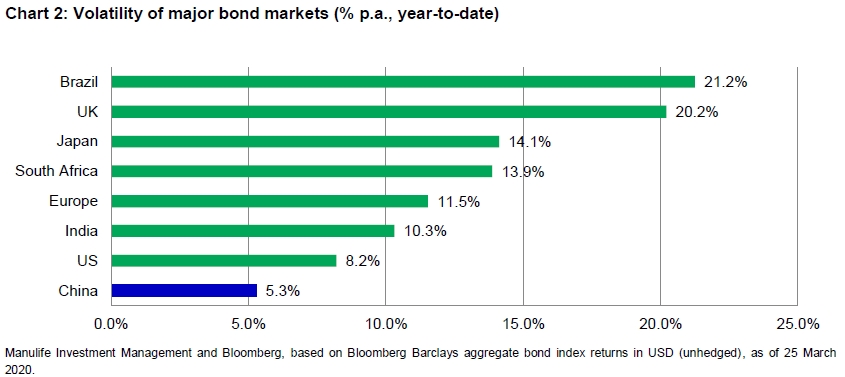

Volatility for Chinese bonds has remained relatively low, despite extreme market conditions. Based on daily returns since the beginning of the year, the annualized standard deviation for the country’s bonds was 5.3% per year, the lowest relative to other global bond markets; similarly, correlations with other major bond markets have also been low during this period. Again, looking at year-to-date daily returns, the correlation between Chinese bonds and U.S. bonds was 0.16, and the asset class’s correlation with European bonds was 0.26.³ These levels are comparable with longer-term correlations (10 years of returns).

What's been happening to China government bond yields?

The People’s Bank of China’s (PBoC’s) initial response to the economic impact of the coronavirus outbreak was one of restraint. The bank made only minor adjustments to monetary policy and refrained from engaging in the more aggressive monetary stimulus that we’ve seen elsewhere, particularly in the United States where the U.S. Federal Reserve (Fed) first cut rates by 50 basis points (bps) on March 3 and then quickly followed up with a second cut of 100bps on March 15, bringing its target rate to between 0% and 0.25%.

Toward the end of March, the PBoC reduced the interest rate on seven-day repurchase agreements, from 2.4% to 2.2%, lowering the rate it charges on loans to banks by the largest amount since 2015 and signaled that there could be larger monetary policy moves ahead.

During the initial phase of its policy response to COVID-19, China acted quickly by focusing on alleviating liquidity pressure on firms, particularly small and medium-sized enterprises, and sought to provide targeted support for the regions and sectors hit hardest by the outbreak. To this end, the PBoC injected around RMB 1.3 trillion of net liquidity through open-market operations in early February⁴ and followed up with additional programs that included a reserve-requirement ratio cut of 100bps for joint-stock banks⁵ and a 10bps reduction in the medium-term lending facility rate in February.⁶ The country’s loan prime rate was also guided 10bps lower in February, but was left unchanged in March.⁷

One reason for the more muted response by Chinese authorities so far is that the reaction in domestic markets has been less acute. China’s equity markets sold off by around 10% in the last month,⁸ compared with losses of over 30% in other territories; consequently, China’s financial markets haven’t faced the same level of liquidity pressure that other developed markets have had to confront. In fact, we haven’t noticed any significant spread widening among onshore corporate bonds, and the country’s new issuance market has been functioning normally.

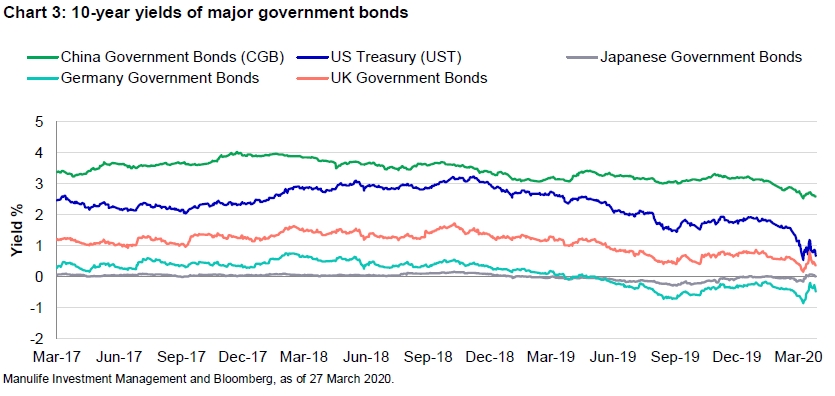

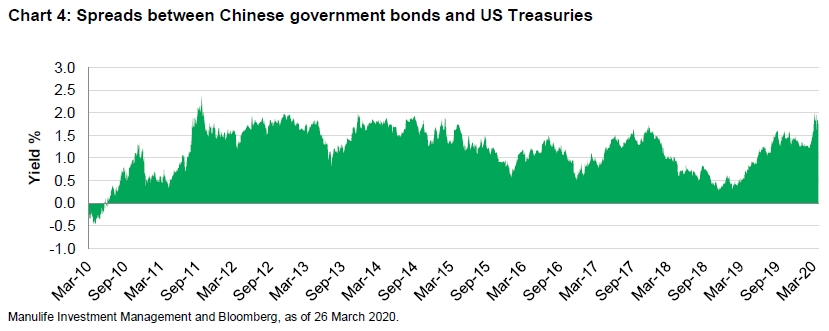

It’s worth noting that 10-year Chinese government bond (CGB) yields have only fallen by around 55bps—to 2.59%—since the beginning of the year, while U.S. Treasury yields declined by 107bps—to 0.84%—during the same period. Accordingly, the spreads between 10-year CGBs and U.S. Treasuries have widened by as much as 1.99%, its widest since late 2011.¹

Further monetary easing ahead

While initial policy efforts have been focused on alleviating liquidity pressures and helping industrial activity to rebound, we believe the Chinese government will have to expand its stimulus efforts to lift demand and support growth, particularly as the global economy appears to be heading toward a sharp recession given that economic activity has effectively paused. Market commentators believe the economy experienced a sharp contraction in the first quarter of 2020 but note that a recovery in the second half of the year is likely, although real GDP growth is likely to be in the low single-digit range. In our opinion, the outlook for Chinese economic growth will be particularly challenging, as demand for its exports is expected to contract significantly in the months ahead and further stimulus will be needed to support growth. At the same time, we believe that the amount of support is unlikely to approach the level we saw in 2008.

Overall, the Chinese government is committed to maintaining a balanced approach that will support growth while ensuring financial stability; furthermore, any new measures will likely combine both monetary and fiscal initiatives. The bottom line is that the PBoC retains significant headroom to trim rates further if the need arises, but should remain prudent and patient while doing so.

Outlook for China credits

The area where the impact of the pandemic will be most keenly felt in China’s economy will be in external demand. We expect China’s export sector to face downward pressure similar to what it experienced during the U.S.-China trade war, and we believe China is also likely to deliver more monetary and fiscal support to drive the economic recovery. In our view, the recent decline in oil prices will be a net positive for China, as the country imports around 70% of its oil; cheaper oil will therefore be helpful to its current account and foreign exchange reserves. Additionally, lower energy prices should help alleviate inflationary pressures and give the country more room to ease monetary policy.

We believe China’s state-owned enterprise (SOE) and local government financing vehicle (LGFV) sectors will remain instrumental in carrying out the government's fiscal stimulus, although with much less headroom compared with the last cycle in 2015, owing to the higher level of local government debt. We expect newly injected liquidity to flow primarily to higher-quality SOEs/LGFVs, while lower-rated SOE/LGFV and private enterprises (onshore AA rated or lower) could face more significant liquidity stress that will likely see default rates tick higher.

"Compared with other major economies, the Chinese financial system should remain relatively resilient as it already went through a deleveraging process in 2017 (to 2019)."

In the Chinese property sector, developers have been negatively affected by operational disruptions from the COVID-19 outbreak since reduced cash flow from property sales raises refinancing risks. So far, the government has remained supportive of the sector and has lifted local sales restrictions in addition to providing ample onshore liquidity. However, smaller developers with limited funding channels and heavy debt maturities will be vulnerable if property sales remain sluggish—we’ve already seen a growing number of defaults by private developers since the outbreak. On the other hand, we believe major developers that are also active issuers in the offshore bond universe are well positioned to weather the current downturn, as most of them have adequate liquidity to meet debt obligations coming due in the next 12 months. The resumption of sales and construction activities for developers under our coverage appears to be on track, although we don’t expect a V-shaped recovery, as property demand remains subdued. We also think that the current situation will accelerate market consolidation, with leading developers and state-owned companies acquiring market share from smaller-scale developers that are at risk of experiencing a liquidity crunch.

The Chinese banking sector is likely to face asset quality pressures given the weaker real economy, while insurers and securities companies may suffer from capital market underperformance. Despite this, we think China’s largest banks remain well positioned, given the quality of the assets on their books and the fact that capital adequacy is at multi-year highs; in addition, they carry little exposure to LGFVs and industries suffering from overcapacity. Compared with other major economies, the Chinese financial system should remain relatively resilient as it already went through a deleveraging process in 2017 (to 2019). Crucially, the Chinese equity market has weathered the crisis better than global markets so far, and the Chinese government has a strong track record of ensuring financial stability.

Renminbi view

While the RMB has weakened by around 1.24% against the USD,¹ we now expect the currency to remain rangebound over the next few months. With the Fed effectively cutting rates to zero, there should be less impetus for the U.S. dollar to appreciate much more from current levels. Additionally, with China applying monetary stimulus at a more measured pace, the RMB is likely to maintain an advantage over its peers in terms of interest-rate differentials, which will support the currency despite a much softer outlook for the Chinese economy.

Conclusion

The COVID-19 crisis has again illustrated the low correlation between China bonds and other global bonds; it also positions CGBs as a relative safe haven asset in these unprecedented times. In our view, the CGB market remains one of the most attractive from an absolute yield perspective and will likely maintain this yield advantage over other developed bond markets. Meanwhile, the Chinese government appears to be committed to taking a measured approach to monetary stimulus. Over the longer term, we expect that the demand for Chinese bonds will continue to grow, as the index-inclusion theme plays out and attracts more substantial fund flows, given that foreign investors remain underinvested in the asset class.

1 Bloomberg, as of March 26, 2020. Refers to performance of the Bloomberg Barclays U.S. Aggregate Bond Index and Bloomberg Barclays China Aggregate Bond Index from January 1, 2020, to March 25, 2020 in USD terms, unhedged. 2 Bloomberg, as of March 26, 2020. Refers to performance of Bloomberg Barclays China Government Index and Bloomberg Barclays China Corporate Bond Index from January 1, 2020, to March 25, 2020, in USD terms, unhedged. 3 Bloomberg, as of March 26, 2020. 4 “China to inject US$174 billion of liquidity into markets amid new coronavirus outbreak,” SCMP, February 2, 2020. 5 “China cuts medium-term rate to soften coronavirus hit to economy,” Reuters, February 16, 2020. 6 “China pumps $79 billion into economy with bank cash reserve cut,” Reuters, March 13, 2020. 7 “China keeps benchmark loan rate unchanged despite coronavirus,” SCMP, March 20, 2020. 8 Bloomberg, as of March 26, 2020. Refers to performance of the Shanghai Stock Exchange Composite Index.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect fund performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the fund’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeam.com.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Asset Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. Thailand: Manulife Asset Management (Thailand) Company Limited. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

513269