China fixed income: the impact of FTSE Russell inclusion and relative attractiveness of China bonds

The recent announcement by FTSE Russell to include China government bonds (CGBs) in its flagship index has deepened investor interest in the asset class. While the structural theme of index inclusion should drive foreign inflows over the medium term, investors should also be aware of other positive short-term drivers. We analyze the impact of FTSE Russell’s inclusion on CGBs and look at the constructive cyclical factors supporting the relative attractiveness of China’s bond market.

On September 24, 2020, FTSE Russell announced that China's renminbi (RMB)-denominated government bonds (CGBs) are scheduled to be included in the firm’s flagship World Global Bond Index (WGBI) from October 2021, pending a final confirmation of inclusion date in March 2021.¹ CGBs' inclusion into the index will be phased in over a 12-month period.

CGBs had originally been placed on the firm’s WGBI inclusion watch list in September 2018, but were ultimately rejected in 2019, as the country’s bond market didn't meet the firm's selection criteria. However, in making its most recent decision, FTSE Russell cited key progress in numerous areas, including improvements to secondary market bond liquidity, enhancements in the foreign exchange market structure, and the development of global settlement and custody processes.²

CGBs are already included in several large global bond indexes, such as the J.P. Morgan and Bloomberg Barclays index suites;³ the asset class's inclusion in the FTSE Russell WGBI is arguably more significant due to the large amount of passive investor flows expected from the decision.

What does FTSE Russell’s index inclusion mean for fund flows into China bonds?

While FTSE Russell won't release the implementation details of the inclusion process until March 2021, estimates suggest that CGBs will make up around 5.7% of the WGBI upon full inclusion.⁴ Based on an estimated US$2.5 trillion (from both passive and active funds) that tracks the WGBI, it's predicted that inclusion in this index could lead to around US$140.0 billion entering China’s government bond market over time.⁵ In the first seven months of 2020, China’s onshore bond market had attracted RMB474.0 billion of foreign inflows, representing a year-over-year increase of 61.0%.⁶

Over the full year, foreign inflows into China bonds are seemingly on track to be between RMB800.0 billion and RMB1.0 trillion. This figure could potentially rise to between RMB1.0 trillion and RMB1.2 trillion in 2021. While foreign ownership of CGBs is currently around 8.5% of the total market, it could increase to around 20.0% by the end of 2022.⁶ Foreign ownership of the overall China bond market could grow from the current 2.6% to almost 4.0%.⁶

Why are China bonds attractive in the short to medium term?

Clearly, the index inclusion theme, including the latest FTSE WGBI announcement, has been important in drawing investor interest into China bonds. This momentum is likely to continue over the medium term, as investors progressively reallocate from other bond markets into China bonds. As this structural theme plays out, the increased demand for China bonds should be supportive for the asset class.

In reaching its decision to include CGBs in the WGBI, FTSE Russell has acknowledged the progress made in improving the market infrastructure for Chinese bonds, which has made market participation by international investors easier.

One recently announced improvement is that regulators have extended trading hours in the China Interbank Bond Market to 8:00 P.M. (12:00 GMT) to facilitate greater access for Europe-based investors. Looking ahead, we believe the Chinese authorities will continue to make further enhancements to facilitate access for international investors, which will further broaden the appeal of the country’s bonds.

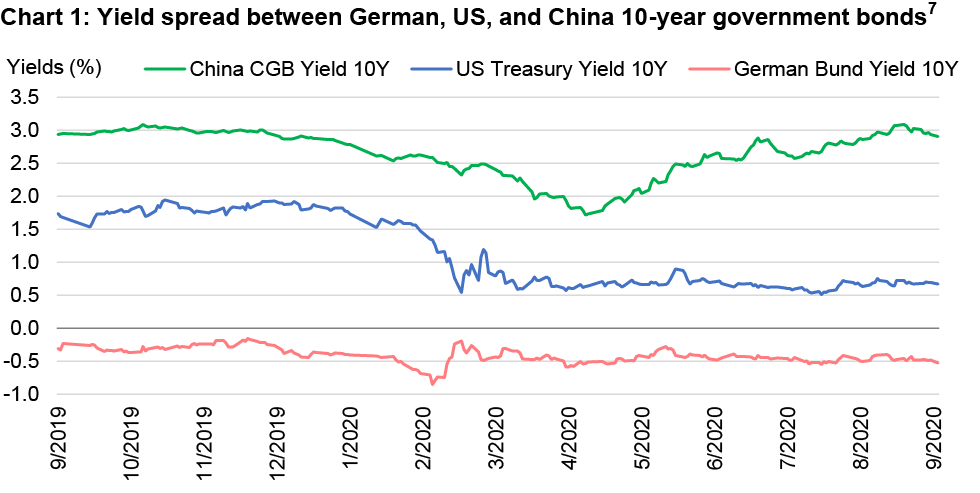

China bonds are also attractive relative to other bond markets from a nominal and real-yield perspective. The 10-year CGB is currently yielding around 3.1% in nominal terms and 0.74% in real terms.⁷ In response to the COVID-19 crisis, global central banks have been cutting interest rates aggressively, with the U.S. Federal Reserve effectively reducing its official rates to zero, while simultaneously signaling to the market its intention to keep interest rates low over the next two to three years. As a result, the 10-year U.S. Treasuries are now yielding around 0.67%.⁷ Consequently, the current spread between 10-year CGBs and 10-year U.S. Treasuries is around 2.4%, making China bonds attractive on a relative basis.⁷

Another attractive aspect of China's bond market is its historically low correlation with other global bond markets, meaning that it could offer diversification benefits. Currently, the correlation for CGBs versus global aggregate bonds is around 0.29.⁸

We believe that the People’s Bank of China (PBOC) will likely maintain a stable interest-rate environment over the next six months, during which it’ll focus on targeted easing and money market operations to ensure there's sufficient liquidity to support growth in the real economy. At the same time, the PBOC wants to underline that financial risks are also being adequately addressed. On the foreign exchange front, we expect the RMB to trade close to its current range of between 6.8 to 7.0 against the U.S. dollar into year end.

Conclusion

The FTSE Russell announcement of the inclusion of CGBs in the WGBI is an important and expected development that should lead to a further and gradual expansion in demand for this asset class from international investors—particularly as authorities continue to work on improving market access. In our view, China bonds also stand out in the current market cycle, relative to other global bond markets, due to their high nominal and positive real yields and diversification opportunities.

1 FTSE Russell, September 24, 2020. In March 2021, FTSE Russell advisory committees and some index users will give final affirmation of CGBs’ inclusion date and implementation timeline based on whether recently announced reforms have made the anticipated practical improvements to the market structure. 2 FTSE Russell, September 24, 2020. 3 In January 2019, Bloomberg Barclays announced that Chinese RMB-denominated government and policy-bank debt would be added to the Bloomberg Barclays Global Aggregate Index from April 2019. In September 2019, J.P. Morgan stated that Chinese government bonds would be included in its Government Bond Index Emerging Markets suite from February 2020. 4 Goldman Sachs, September 19, 2020. 5 Goldman Sachs, September 29, 2020, based on the estimated US$2.5 trillion in assets under management tracking the FTSE WGBI index. 6 Standard Chartered, as of August 31, 2020. 7 Bloomberg, as of September 21, 2020. 8 Based on 10 years, from 30 September 2010 to 30 September 2020. Aggregate bonds are represented by Bloomberg Barclays Global Aggregate Total Return index; China government bonds are represented by ICE BofA China Government Index.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect fund performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the fund’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeam.com.

Australia: Hancock Natural Resource Group Australasia Pty Limited, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Asset Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. Thailand: Manulife Asset Management (Thailand) Company Limited. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

523974