Taking a second look at Asian High Yield

Since the downturn in 2021-2022, Asian High Yield (HY) has rebounded on the back of numerous factors, including a more diversified universe, strong performance among major markets, and robust technicals. In this investment note, the Asian Fixed Income team analyses the transformation of the asset class over the past three years and explains why investors searching for attractive yield amid a favorable risk-reward profile should now take a second look.

The past three years have been transformative for Asian HY bonds. The collapse of the Chinese property sector in 2021-22 served as a pivotal catalyst, effectively resetting the market. Since that time, the universe has become much more diversified, balanced, and higher quality. However, this shift may have been overlooked by investors, possibly due to negative experiences during the drawdown.

The Asian HY market has seen a significant rally since its lows in November 2022, but we do see compelling reasons to believe that the asset class can continue to offer attractive returns, reminiscent of its performance before the COVID-19 pandemic. We feel now is an opportune time to revisit this unique asset class, looking at it from a renewed perspective and capturing the attractive yields offered.

We did not see a “V-shaped recovery,” but we got much better than an “L-shape”

Considering that Asian HY has lost more than 40% of its market value from the peak back in 2021-22, many believed that it would take a prolonged period of time (i.e. a “L-shaped recovery”) before we could see the highs once again – the leading cause of the drawdown (Chinese property) was unlikely to be the main recovery driver that would take the asset class back to its highs given the number of defaults and lack of access to capital markets for Chinese property developers.

Yet, in just three years since the asset class hit its lows in November 2022, we are now around 5% away from historical highs. However, is this recovery sustainable, and what did many investors overlook?

Chart 1: Asian HY historical performance1

Asian HY is not limited to China, it has some of the fastest-growing markets in recent years

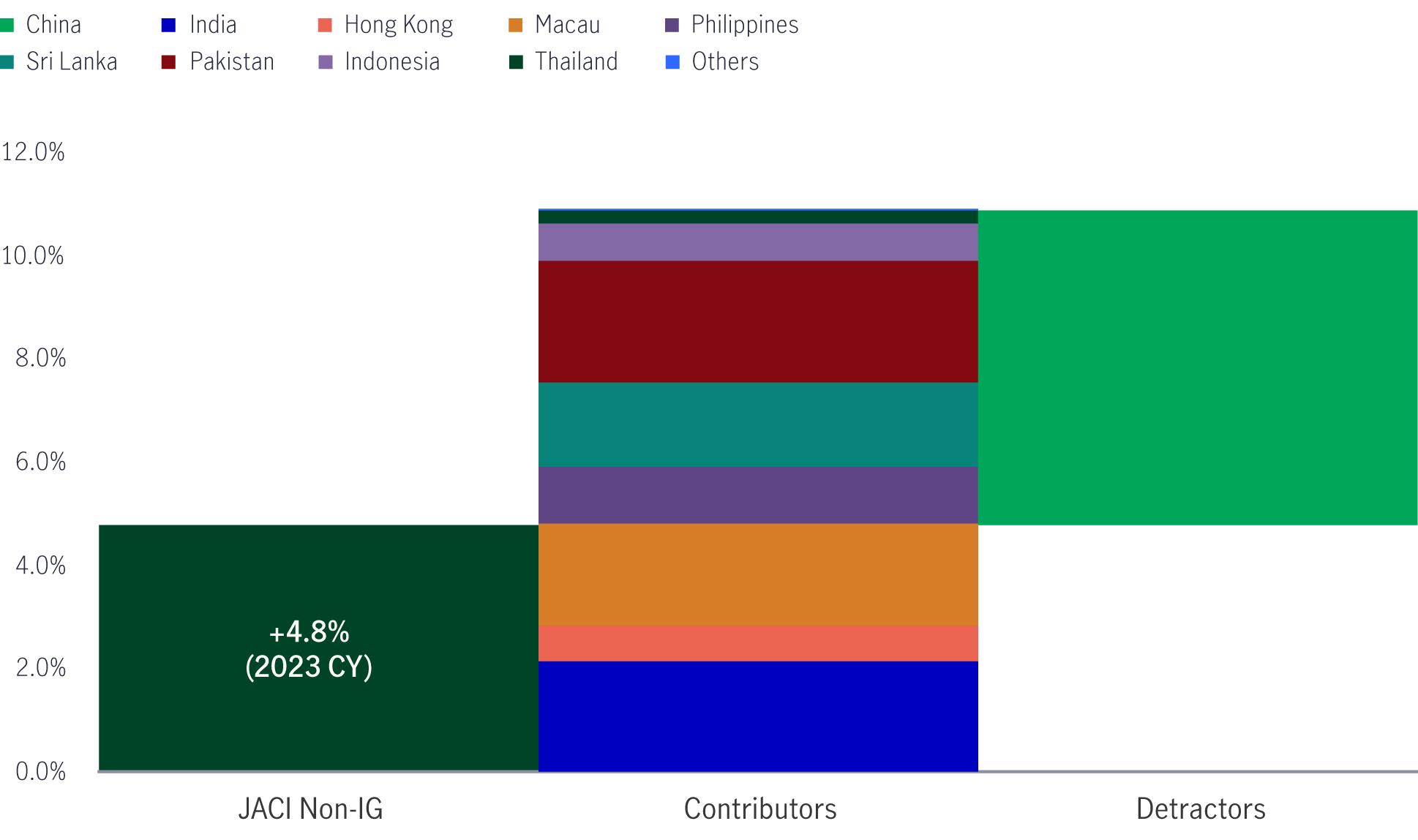

Negative headlines around the downturn of the Chinese property sector may have taken the spotlight for a few years, but under the surface, other parts of Asia were growing steadily and have become greater drivers of the market.

Asian HY is now a more diversified asset class where aggregate performance has, for some time, been driven by the combined contributions from different markets and segments, rather than from any individual dominating cohort.

Asian HY’s 2023 performance was a perfect example of this. While China continued to deal with a series of headwinds and challenges related to policy and a slowing economy, other markets stepped up and contributed, helping the asset class deliver a net positive performance for the full year. We saw notable contributions across different segments, including Macau gaming, frontier sovereigns, and selective Indian credits.

Chart 2: Asian HY total return performance by contribution (2023)2

The asset class has also been much more diversified following the reset from the Chinese property downturn.

At one point, China accounted for over half of the Asian HY market – approximately 54% in market value terms as of December 2019; however, by August 2025, this number had declined to less than a quarter, at around 22%. China property has also declined to less than 7% of the JACI Non-Investment Grade investment universe. Meanwhile, other markets, including Hong Kong, India, the Philippines, and frontier sovereigns, have gradually taken a greater share over time.

While investors may be aware of the developments within the asset class in recent years, it is important to remember that Asian HY is not just China; it is, as the name suggests, all of Asia.

Chart 3: Changes in Asian HY composition (from 2019 to 2025 YTD)3

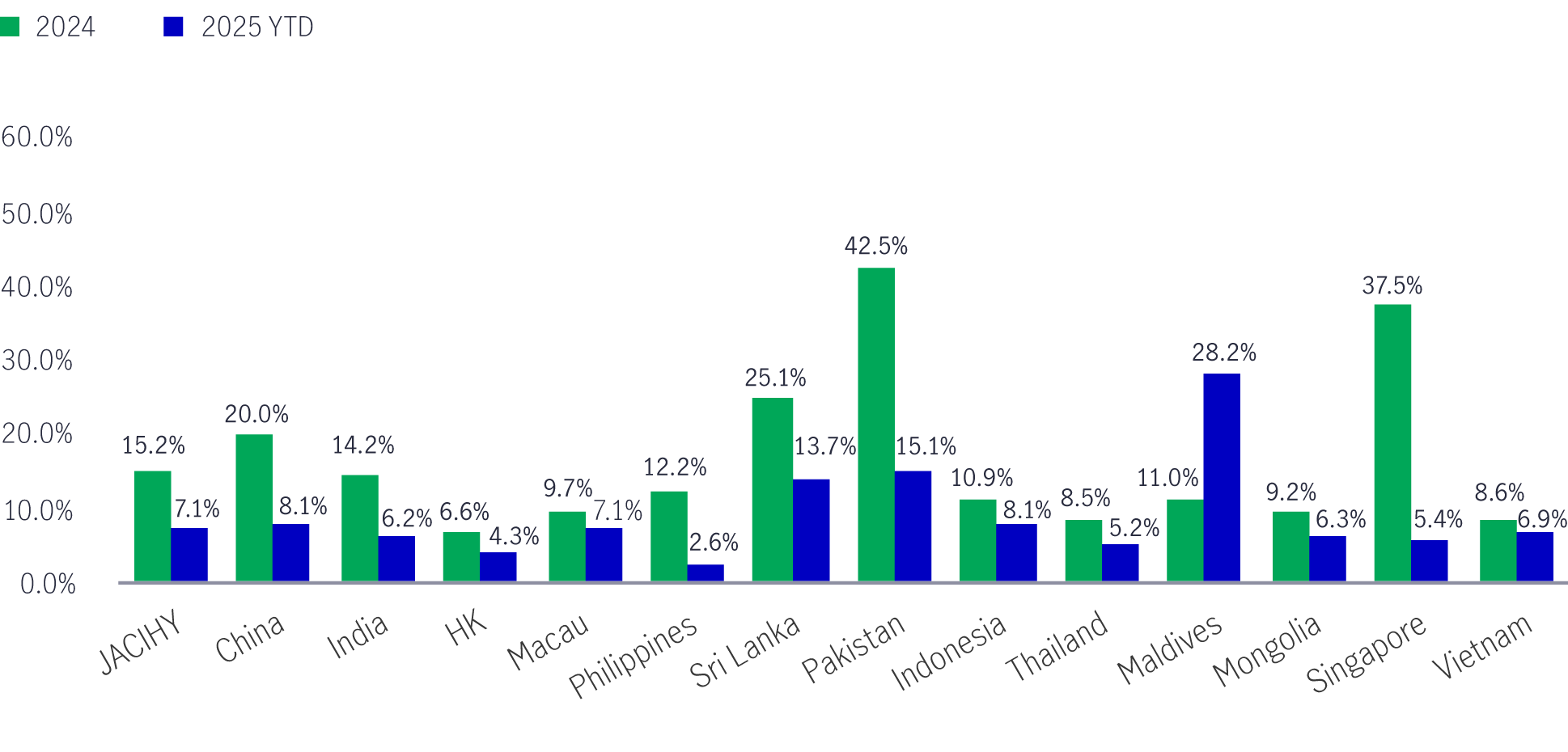

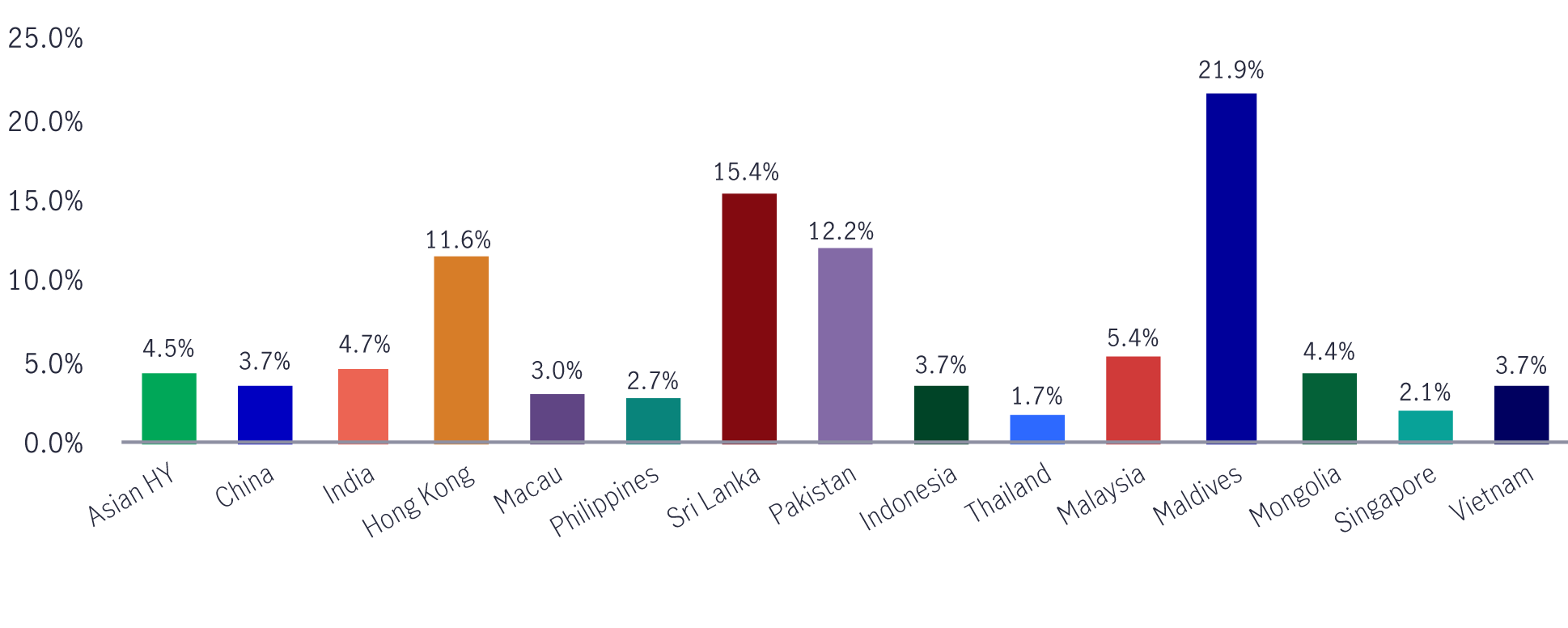

This recovery should be sustainable because of the strength in market breadth

If the rebound in recent years has been driven by just one or two key segments – like how the “Magnificent Seven” have bolstered returns in the US equity markets – we might question the sustainability of the rally.

However, what’s worth highlighting here, and certainly something we believe is underappreciated by the market, is that all major markets within the asset class have delivered positive returns for 2024 and year-to-date 20254 on the back of broader improvement in fundamentals and a supportive macro backdrop across the region.

Chart 4: Individual market Asian HY total return (2024 and 2025 YTD)5

One of the advantages of a market with strong breadth is that if certain segments face idiosyncratic challenges in the near future, the strength of other segments can likely offset any potential negative impacts. This resilience could enable the asset class to continue delivering attractive returns on an aggregate basis.

The question then becomes: What would it take for the asset class to deliver negative returns in any given year?

With the well-diversified composition that we currently have in the Asian HY market, we believe that the main downside risks would be much broader, macro-related – something that could negatively impact returns across all the different markets – rather than any individual bottom-up, idiosyncratic event.

Like with any other US-dollar fixed-income asset class, this would be either: 1) a sharp rise in US Treasury yields, 2) an aggressive widening in aggregate credit spreads (due to, for example, the spillover from a US recession), or 3) a combination of the two.

However, given the impressive carry (i.e. average yield-to-maturity of 8.9% as of end-August) and low interest rate/credit spread sensitivity of the asset class, it would take a major negative market-moving event to bring total returns of the asset class to negative for any given year. Not to mention that the asset class is well supported by domestic investors (i.e. “all-in yield” buyers) who are familiar with their own local markets, and by limited supply.

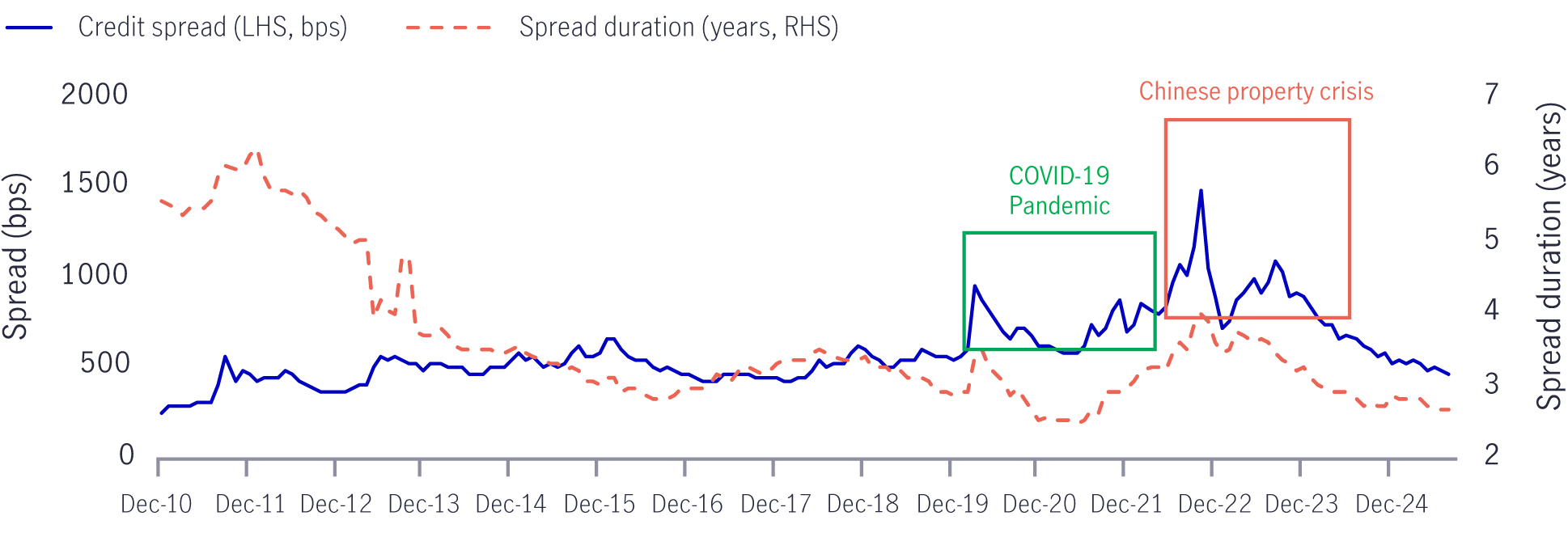

Chart 5: Asian HY sensitivity to interest rate and credit spread movements6

At this juncture, we feel that the market should be supported given that we are in the early innings of the US rate-cut cycle (i.e. both the US Federal Reserve (Fed) dot plot and Fed Fund Futures imply that this rate cut cycle will last at least until 2027) and that the favorable macroeconomic backdrop and monetary easing across the Asia region is supportive for aggregate credit spreads, despite the persisting headwinds on trade policy and geopolitics.

Aggregate valuations have tightened, but they need to be put in the proper context

Asian HY hasn’t been able to catch a break since the start of the decade. We have seen back-to-back headwinds from the COVID-19 pandemic in early 2020 and the downturn of the Chinese HY property sector in 2021-22. However, with aggregate valuations having tightened to pre-pandemic levels in recent months, the market is telling us that we have shifted to a new regime and that we should be looking at Asian HY from a fresh perspective.

This raises the question: what should the fair credit spread levels (or valuations) for the asset class be?

If we refer to the period before the COVID-19 pandemic, Asian HY had been trading at credit spread levels that ranged largely between 400 and 600 basis points (bps).

This period (2010-2020) was just as eventful as any other in recent history in the context of the global markets, as we have encountered various episodes of volatility, including the Eurozone debt crisis, Brexit, Fed tapering, and escalating Sino-US trade tensions.

What really differentiated the COVID-19 pandemic from other events was the profound impact it had globally on supply chains, consumer behaviour, and business models; in other words, it was arguably a “tail risk” event.

In the absence of another major global shock, we believe that a credit spread range of between 400 and 600 bps would be reasonable for aggregate Asian HY bonds, given the changes that the asset class has been through in recent years, in addition to normalizing default rates and stable fundamentals.

If we encounter another major global shock comparable to that of the COVID-19 pandemic, we may see credit spreads widen to a range of 600 to 800 bps, using 2020-21 as reference, but the chances of aggregate credit spread levels widening beyond 1,000 bps is less likely given we do not expect to see a significant pick-up in the number of defaults nor an event as significant as the collapse of the Chinese property segment within the asset class in the foreseeable future.

Additionally, aggregate spread duration (a measure of credit risk) for Asian HY has declined to near historic lows, which, given the range of 400 to 600 bps of credit spread, would make the asset class even more appealing from a risk-reward perspective, compared to the past.

Chart 6: JACI non-investment grade (IG) historical spread and duration spread levels7

We expect that the tightening of aggregate valuations in Asian HY will continue to be driven by supply and demand dynamics. In particular, the lack of new issuance and the negative net supply for the asset class, coupled with strong investor demand.

This robust technical factor supports the market, as investors will seek opportunities to acquire Asian HY bonds at attractive valuations, whether through a market sell-off or new issuance, thereby creating a psychological floor for bond prices. On the other hand, persistent market headwinds, including a global growth slowdown, geopolitical tensions, and trade uncertainties, will help to maintain balanced valuations.

Ultimately, this means that investors can potentially receive an additional 4% to 6% in yield on top of the yield offered by US Treasuries from investing in Asian HY bonds due to credit spread pick-up, but this will require careful security selection as there is a wide dispersion in credit spreads between the higher- and lower-quality names. Nonetheless, this pick-up will remain attractive as the Fed continues to cut interest rates and as investors seek to enhance the overall return on their investment portfolios.

There will be alpha generation opportunities as long as there is dispersion

With the aggregate tightening in valuations, we do not believe this implies fewer investment opportunities. To generate alpha in any particular market, it is important to note the level of dispersion rather than simply looking at valuation levels. Without getting too technical, dispersion refers to the variability of returns among different securities compared to the market average.

In markets with higher dispersion, skilled portfolio managers who rely more heavily on bottom-up security selection can potentially generate greater alpha by making the correct calls (i.e. overweighting/underweighting securities with excess returns well above/below the mean) because of the wider range of excess returns and the relatively higher number of opportunities available.

For example, a portfolio manager would only need to have a 1% overweight position in a security that delivers 10% in excess return to be able to generate 10 bps of alpha.

Conversely, in markets with lower dispersion, not only are there relatively fewer alpha-generating opportunities with a tighter distribution of returns, but portfolio managers may also need to have more concentrated positions in the select few outperformers to achieve comparable alpha.

For example, assuming a portfolio manager successfully selects a security that delivers 2% in excess returns (which may be considered high in a market with low dispersion), the portfolio manager would still need to have a 5% overweight position in that security to generate 10 bps of alpha, which is more difficult and leads to higher concentration risk.

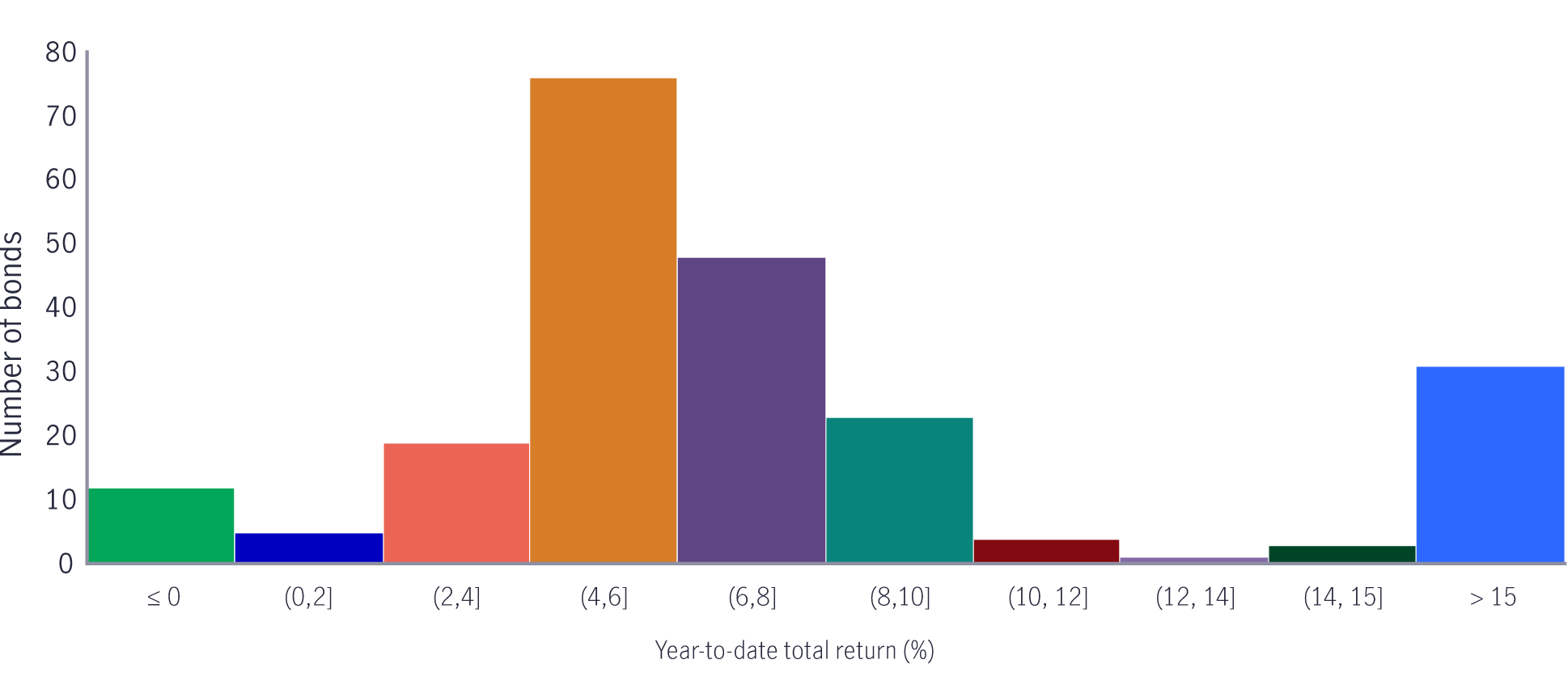

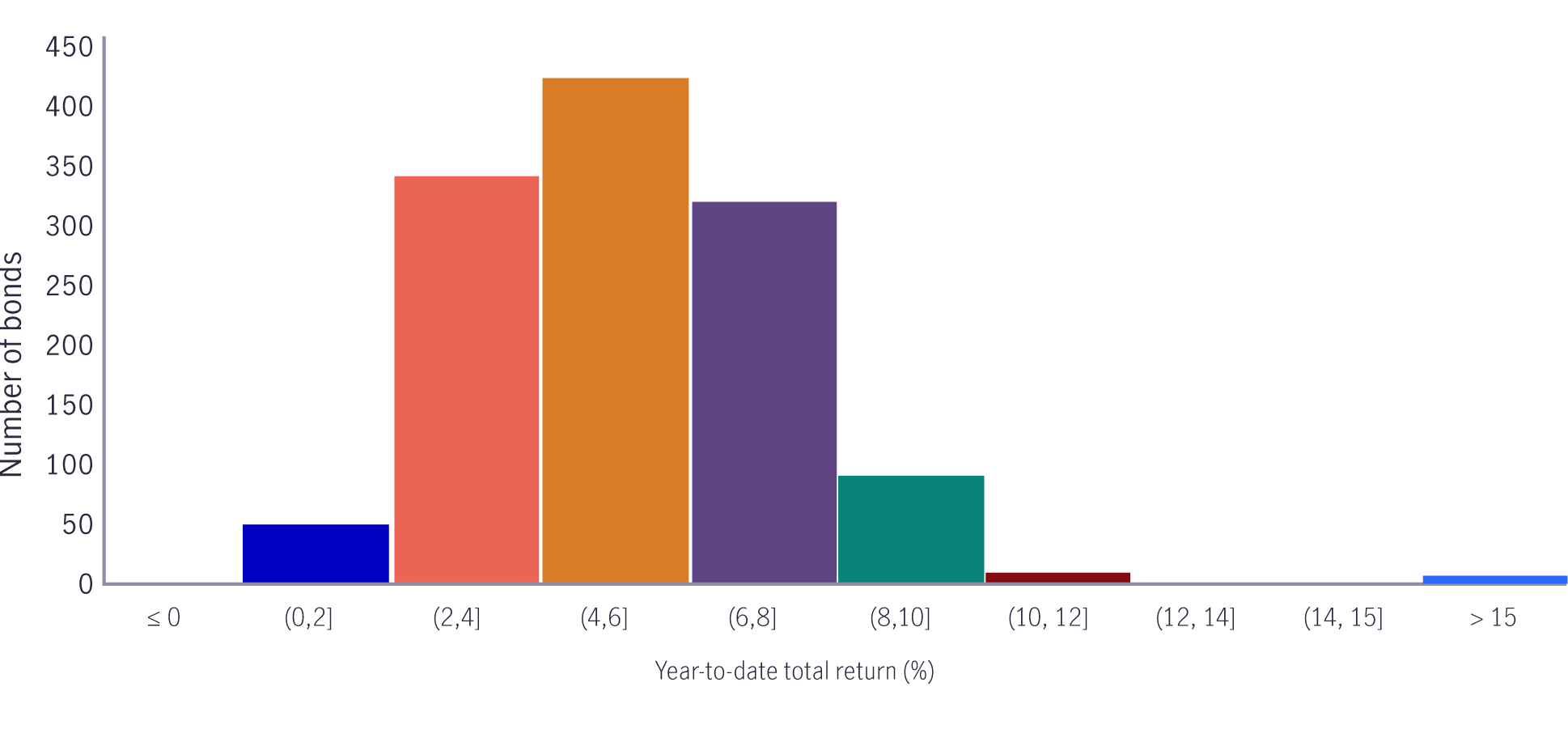

We can see from the charts below that the Asian HY market remains well dispersed compared to, for example, the Asian IG market.

Chart 7: Dispersion of total returns in Asian HY and IG market (2025 YTD)8

HY

IG

Conclusion: Three takeaways (in figures) after three years

With the progression we have seen in Asian HY over the past three years, we believe now is the right time for investors to put aside the past and to focus on how this asset class can potentially add value for their investment portfolios. As such, we would also like to highlight three key takeaways – with numbers – for investors.

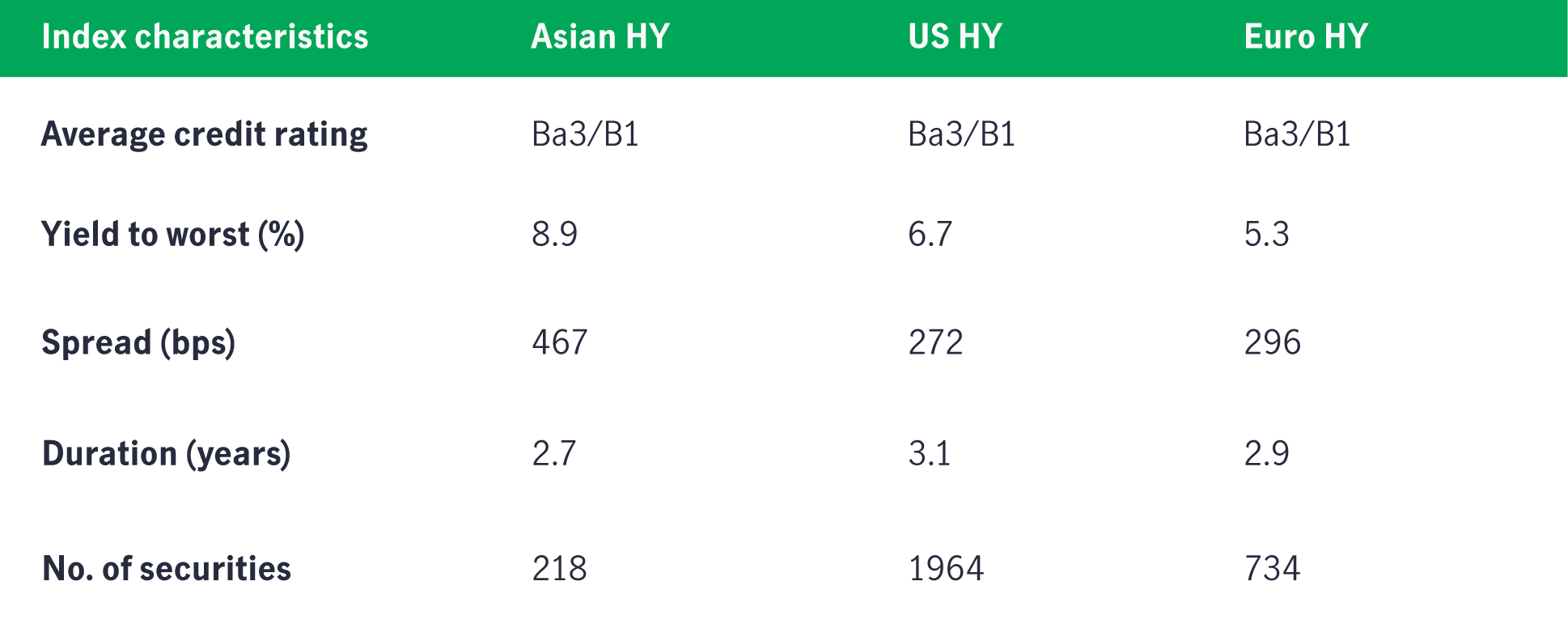

1) Return: 8.9

This is the average yield-to-worst (“yield”) that investors are getting from investing in Asian HY, coming from both the underlying bonds’ coupon income (around 6%) and pull-to-par capital appreciation. This is more attractive than the 6.7% and 5.3% average yields offered by the US and European HY markets, respectively, not to mention that the other two HY markets have higher interest rate (duration) and credit (spread duration) sensitivity as well.

It is also worth noting that the three markets have similar average credit ratings.

Chart 8: Characteristics across Asian, US, and European HY markets9

2) Risk: 4.5

This is the monthly annualized year-to-date volatility of the Asian HY asset class (in % terms), as of end-August 2025. More importantly, Chinese HY credits have been notably less volatile than the broader index with a comparable figure of 3.7%, unlike what many investors had expected, due to the money and fiscal support by the government since 2022, as well as the shift in sector mix within China HY (i.e. lower exposure to real estate and more diversified across other cohorts).

Instead, much of the volatility this year has come from the frontier markets (including Sri Lanka and Pakistan) due to their vulnerability to trade as well as their ongoing economic recoveries.

Chart 9: Volatility of Asian HY markets (monthly annualized)10

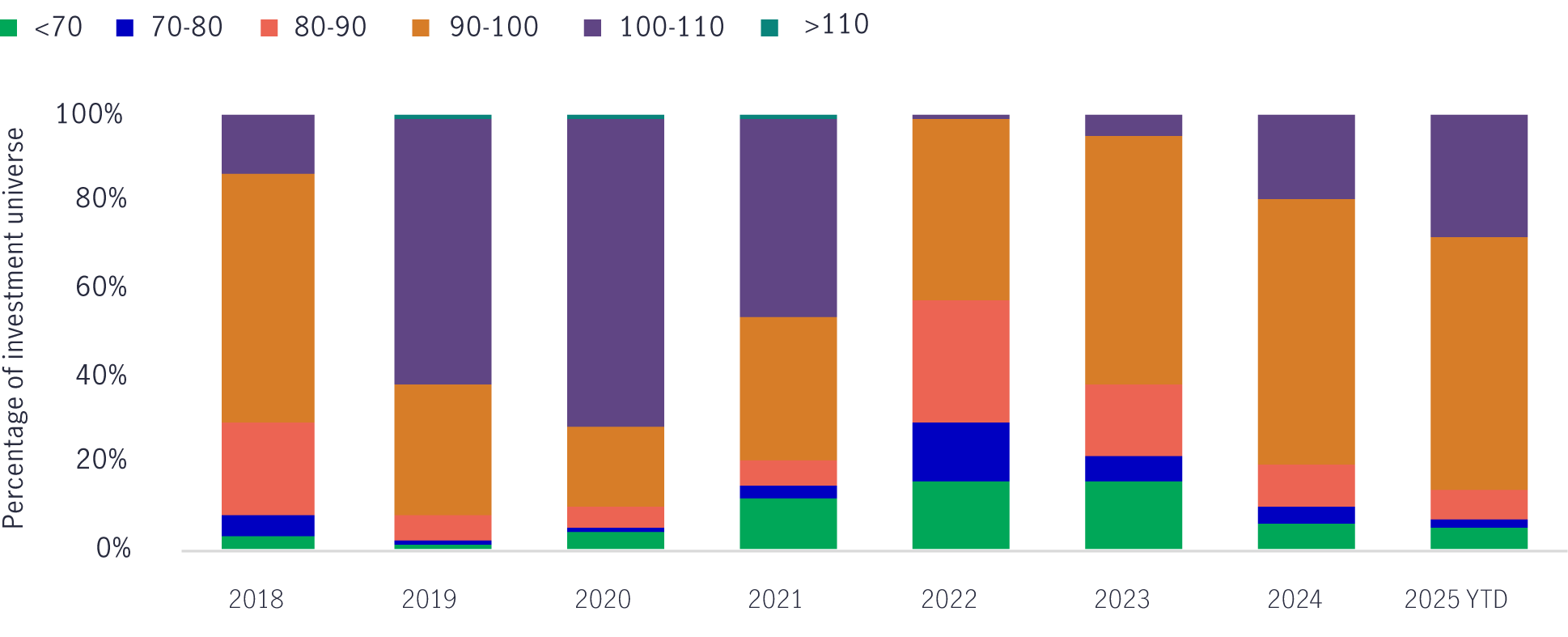

3) Quality: 94

This is the percentage of Asian HY bonds that are trading at a bond price above 80 cents on the dollar. This figure is closer to the one we saw in 2018-19, suggesting it may be more appropriate to compare the asset class to the pre-Covid era, as mentioned above. In addition, higher average bond prices also signify an improvement in quality, as investors are willing to pay more (in some instances, above par) to own the bonds. A part of this is also attributed to the supportive technical factors mentioned earlier.

Chart 10: Historical breakdown of Asian HY bond prices11

Rather than staying on the sidelines, why not put the past behind you and consider revisiting the asset class now?

1 Source: Manulife Investment Management, JP Morgan Indices, Bloomberg, as of August 31, 2025. Asian HY represented by JACI Non-IG Index. 2 Source: Manulife Investment Management, JP Morgan Indices, Bloomberg, as of December 31, 2023. 3 Source: Manulife Investment Management, JP Morgan Indices, Bloomberg, as of August 31, 2025. 4 Source: Bloomberg, as of August 31, 2025. 5 Source: Manulife Investment Management, JP Morgan Indices, Bloomberg, as of August 31, 2025. 6 Source: Manulife Investment Management, Bloomberg, JP Morgan indices, as of August 31, 2025. Based on JACI Non-IG Index (August 2025): YTW 8.9%, Duration 2.7 years, Spread Duration 2.7 years TR = Total Return, YTW = Yield-to-worst. 7 Source: Manulife Investment Management, JP Morgan Indices, Bloomberg, as of August 31, 2025. 8 Source: Manulife Investment Management, JP Morgan Indices, as of August 31, 2025. 9 Source: Manulife Investment Management, Bloomberg PORT, JP Morgan Asia Credit Non-Investment Grade Index, Bloomberg US Corporate High Yield Index and Bloomberg Pan European High Yield (USD Hedged) Index, as of August 31, 2025. 10 Source: Manulife Investment Management, JP Morgan Asia Credit Non-Investment Grade Index, as of August 31, 2025. 11 Source: Manulife Investment Management, Bloomberg, JP Morgan indices, as of August 31, 2025.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional

Australia: : Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. Mainland China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area: Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which

is authorised and regulated by the Financial Conduct Authority

United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

4843241