The case for liquid real assets in a shifting inflation regime

For over a decade, global investors operated under the assumption that inflation would remain subdued, anchored below 2%¹ - a belief reinforced by central bank credibility and structural disinflationary forces like globalization and technological deflation. However, the post-pandemic world has ushered in a new regime of structurally higher inflation risks, with evolving policy responses that make liquid real assets increasingly attractive.

.jpeg)

Key takeaways:

- Inflation risks are structurally higher post-pandemic, driven by fiscal expansion, monetary easing, and a closed US output gap.

- Rising tariffs, reshoring, and geopolitical fragmentation are reversing disinflationary trends, tightening global supply chains.

- Long-term capital investment in AI infrastructure and rising defense budgets are fueling demand for energy, metals, and utilities.

- Infrastructure, energy, and metals & mining (including rare & critical minerals) are benefitting from secular demand and supply constraints, while REITs show selective regional and sectoral opportunities.

- Real assets offer differentiated returns and income potential, with periodic low correlation to traditional equities and bonds.

Monetary policy easing

Across major economies, especially outside the US, monetary policy is easing even as fiscal expansion accelerates. In the US, the Federal Reserve is expected to pivot toward monetary stimulus despite the absence of a clear economic shock. This double-barreled stimulus – monetary and fiscal – arrives at a time when inflation has already bottomed at levels above the Fed’s 2% target2. As of this writing, core Consumer Price Index (CPI) stands at 3.1%3, and the risk is that inflation could reaccelerate once stimulus fully takes hold.

This risk is compounded by the fact that the US output gap is closed. The economy is operating above potential, meaning there is little slack to absorb additional demand. In such an environment, any incremental stimulus – especially fiscal – has a higher probability of translating into price pressures rather than real growth. This dynamic increases the likelihood of an inflation shock, increasing the attractiveness of inflation-sensitive assets.

Tariffs, global supply chain and geopolitical risks

Structural forces are also shifting. Deglobalization is reversing decades of supply chain optimization. Rising trade barriers, reshoring initiatives, and geopolitical fragmentation are reducing efficiency, increasing redundancy, and raising unit labor costs. These changes are inherently inflationary and diminish the deflationary impulse once provided by globalization.

China, long a source of global disinflation, is undergoing a strategic pivot. Its anti-involution campaign aims to reduce excess production capacity, consolidate industries, and restore pricing power. This shift will likely reduce China's role as a supplier of ultra-low-cost goods. Meanwhile, other countries are pushing back on Chinese exports in recent days: the US is considering new tariffs, Mexico has followed suit, and the European Union is investigating dumping practices and considering trade restrictions4. These developments suggest a global tightening of supply, supporting higher prices.

Benefitting from structural trends

Thematic trends are also inflationary. The AI buildout is driving massive capital investment in data centers, straining electricity grids and increasing demand for semiconductors, metals, and energy. Simultaneously, defense spending is rising as geopolitical tensions mount. These trends are not cyclical – they represent long-term shifts in fiscal priorities and industrial demand, both of which are inflationary.

Despite these pressures, markets have only partially priced in a higher inflation regime. The yield curve has steepened, but not dramatically. This suggests that while investors are adjusting to the reality of structurally higher inflation, we believe valuations for inflation-sensitive assets remain compelling. This creates a compelling entry point for strategies that benefit from inflation surprises.

We see specific real asset classes benefiting from structural shifts in inflation and demand:

Infrastructure is evolving beyond roads and bridges. The asset class stands to benefit from rising demand for AI and digital infrastructure, supported by the continued electrification and energy transition efforts globally. Electric and Gas utilities have been strong this year, driven by record-high electric consumption from data processing growth, factory reshoring, and decarbonization initiatives.

Energy: OPEC’s effort to stabilise oil prices may support demand growth and benefit the refining sector. We expect natural gas to remain a bright spot over the next year, with Canadian and US Liquefied Natural Gas (LNG) projects ramping up supply needs. Near term prices could remain elevated as it appears that production will lag demand for natural gas. Furthermore, countries in Europe and Asia are looking to diversify away from Russian gas and reduce coal use, likely locking in long term LNG contracts with North American suppliers. AI-driven power demand remains a wild card, potentially further increasing North American gas consumption.

Metals & Mining are supported by multiple tailwinds. Gold remains resilient, backed by global central bank purchases and strong Chinese demand. Geopolitical risks and uncertainty enhance its diversification appeal, whilst metal miners operating leverage boosts profitability. Copper faces tighter supply due to mine disruptions in the Democratic Republic of Congo (DRC) and Panama and falling inventories point to global deficits. A strong secular demand from electrification and higher capex expectations from grid upgrades adds to a positive outlook.

Uranium continues to benefit from the clean energy push, especially China’s nuclear expansion. Meanwhile, silver and platinum are showing signs of catching up to gold, supported by supply deficits and improving fundamentals.

Rare Earths, Critical Metals & Minerals (Cobalt, Antimony, Tantalum, Scandium) continue to be of strategic importance for their use in defense technologies, electronics, aerospace components and permanent magnets.

Real Estate Investment Trusts (REITs): Despite some signs of stabilization, we see persistent macroeconomic and sector-specific headwinds. While falling interest rates may offer some relief, the lagged impact of prior rate hikes, elevated financing costs, and uncertainty around tariffs and trade policy continue to cloud the outlook—particularly in the US office and retail segments. Additionally, US office REITs remain under pressure from structural shifts in workplace demand, with utilisation improving but not yet translating into new leasing activity.

However, we do see attractive valuations in Hong Kong and Singapore as well as seeing M&A activity picking up in UK industrial REITs. Healthcare related REITs offer selective opportunities within senior housing as ageing populations drive demand. Lastly data center/ AI infrastructure build-out continues to support occupancy.

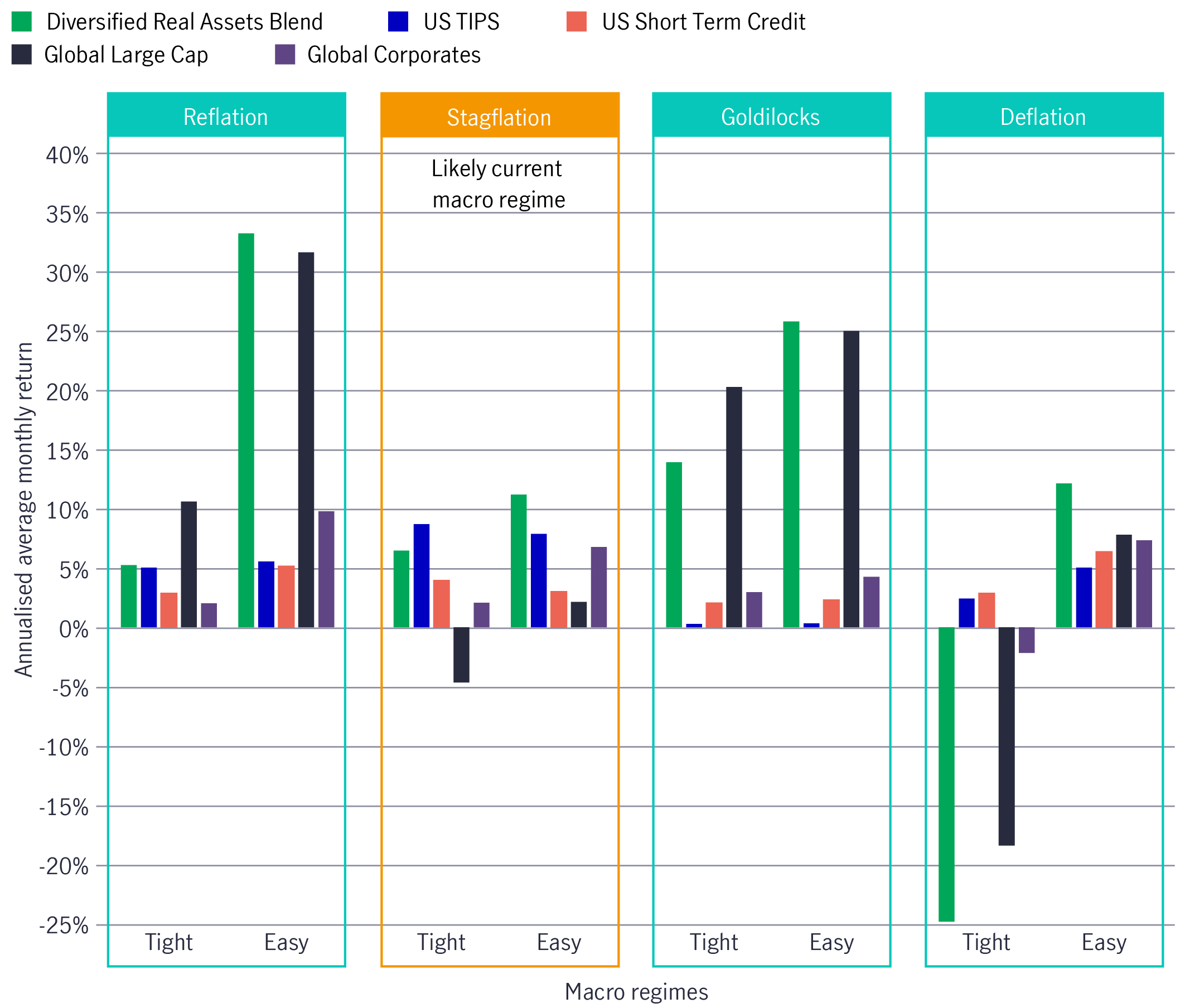

Real assets tend to outperform in high inflation environments

Inflation expectations are likely to remain elevated as tariffs percolate through higher consumer prices. We believe increased political pressure on the Fed could modestly dampen inflation expectations over a 2-year horizon. The shift back to low growth aligns with our view of below-trend economic performance in the near term. With the Fed now expected to cut rates several times in 2025 and 2026, financial conditions could ease more decisively, potentially triggering a trend reversal. This reinforces the odds of easy-stagflation or easy-reflation regimes ahead. In such environments, real assets have historically outperformed broader markets, making them a compelling allocation for investors (see Chart 1).

Chart 1: Real assets can add value under current macro regimes and environment

Inflation hedge with income potential

A diversified allocation to liquid real asset – spanning energy, materials including precious/base metals and mining, real estate, infrastructure equities, and short-maturity Treasury Inflation-Protection Securities (TIPS) – may help investors manage inflation risk. These assets tend to benefit from rising input costs, pricing power, and real asset exposure. Many real assets have the potential to generate steady income, such as rent from property, tolls from infrastructure, or utility cashflows, that may provide competitive yields linked to inflation.

Diversified and differentiated returns

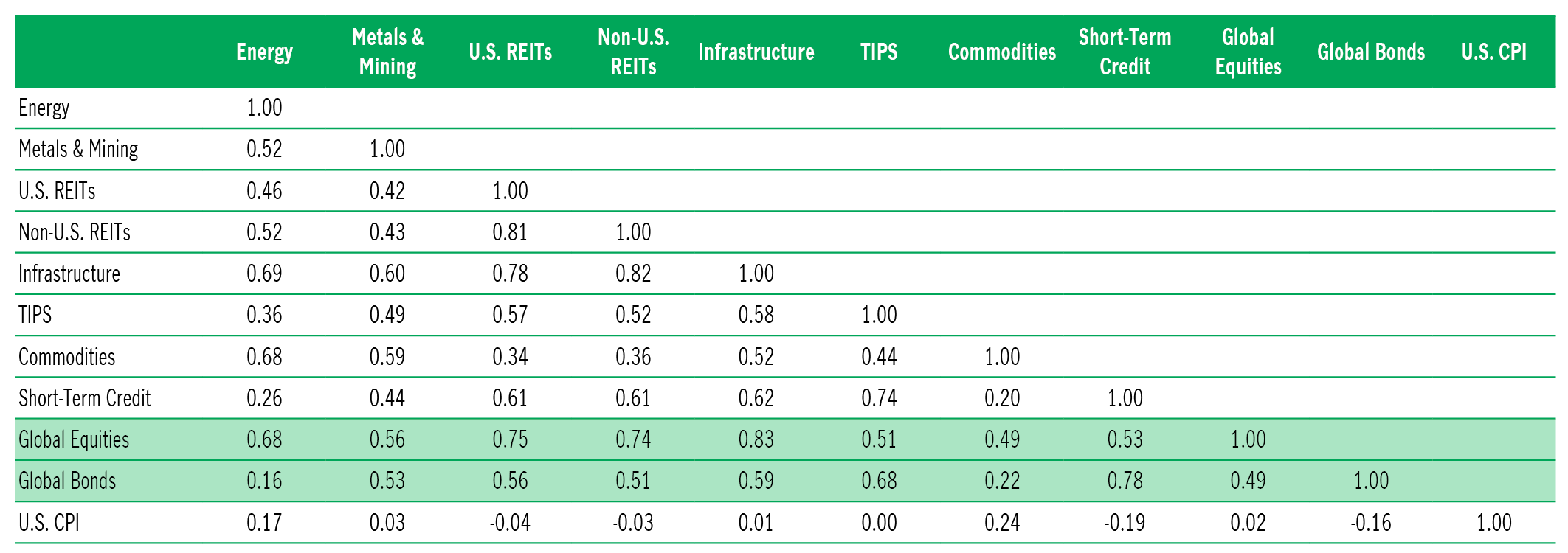

Real assets have at times, shown low return correlation with traditional equities and bonds, offering potential diversification benefits (see Chart 2). The distinct return profile can enhance portfolio resilience, especially during periods of elevated inflation and market volatility.

Chart 2: Correlations of real assets versus traditional global equities and bonds (August 2010 – August 2025)

As inflation risks become more entrenched and policy responses more aggressive, investors will need to rethink traditional portfolio construction. Liquid real assets have the potential to offer an inflation hedge alongside income, across a broad diversified global opportunity set – all of which are especially valuable in today’s uncertain environment. Real assets can provide a bridge between inflation protection and capital appreciation, making them a strategic allocation in today’s evolving landscape.

1 Source: Manulife Investment Management, Bloomberg, Inflation sensitive equities: A new way forward, January 2025; 2 Source: Manulife Investment Management, Bloomberg, September CPI, as of October 14, 2025. 3 Source: Manulife Investment Management, Bloomberg, September CPI, as of October 14, 2025. 4 Source: Manulife Investment Management, Reuters, Trump ratchets up US-China trade war; China ramps up rare earth restrictions, October 14, 2025.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional

Australia: : Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. Mainland China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area: Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which

is authorised and regulated by the Financial Conduct Authority

United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

4920570