India’s bond index inclusion: Attracting foreign investment; bolstering its regional position

On 21 September 2023, JPMorgan announced that Indian government bonds would be included in the company’s Government Bond Index-Emerging Markets (GBI-EM) Global index suite starting in June 2024. We examine the short- and long-term implications of this significant decision for the Indian bond market, including how it could attract greater foreign investment and may bolster the country’s long-term position in Asia’s fixed-income universe.

After several years of reform, it has now been confirmed that India will be included in the JPMorgan GBI-EM Global index suite starting in June 2024, representing a significant milestone in the development of the Indian bond market.

This comes after India was placed on ‘watch positive’ for index inclusion in 2021 after the Indian government announced the removal of restrictions for foreign investors in the sovereign bond market in 2020. JPMorgan’s recent decision also considered investors’ opinions that India’s inclusion would result in a more diverse and representative index by reducing concentration among greater-weighted countries.

As a result, starting in June 2024, India will join the flagship JPMorgan GBI-EM Global Diversified index with a 1% weight. At this point, only FAR (Fully Accessible Route)- designated Indian government bonds with a notional value of US$1 billion or more and at least a remaining maturity of 2.5 years will be allowed to join the index¹. Currently, 23 bonds with a notional bond value of US$330 billion are eligible for the index.

Over time, the country’s weight will increase by one percentage point each month until it reaches its final index weighting of 10% in April 2025, on par with China and Indonesia, the largest expected country weights of the revised index.

After full inclusion, India will be the second biggest EM country in the index after China. Asia will compose roughly 50 percent of the index. Overall, inclusion gives investors access to the second-largest bond market and the highest-yielding market in the region.

Short-term implications: increased capital inflows and macro support

Over the short term, inclusion is expected to increase passive capital flows linked to the index significantly.

Roughly US$236 billion of global funds is benchmarked to the GBI-EM Global index suite. Once inclusion starts, inflows into the country’s government bonds are expected to total around US$30 billion, or US$3 billion per month, until India reaches its final weight². Related buying should be most supportive for the long end of the curve with maturities greater than five years.

From a macro perspective, increased capital inflows should help narrow the country’s marginal current account deficit (-0.2% of GDP- Q1 2023) or even flip it into surplus, which should support the rupee.

The initial response from the market to the index inclusion news has been positive: Indian bonds have outperformed other Asian local markets month to date by around 10-15 basis points3.

Long-term implications: greater foreign investment and structural market maturation

Over the longer term, the implications should be more transformative, including greater foreign investor participation while the government bond market and the Indian bond asset class continues to develop and mature structurally.

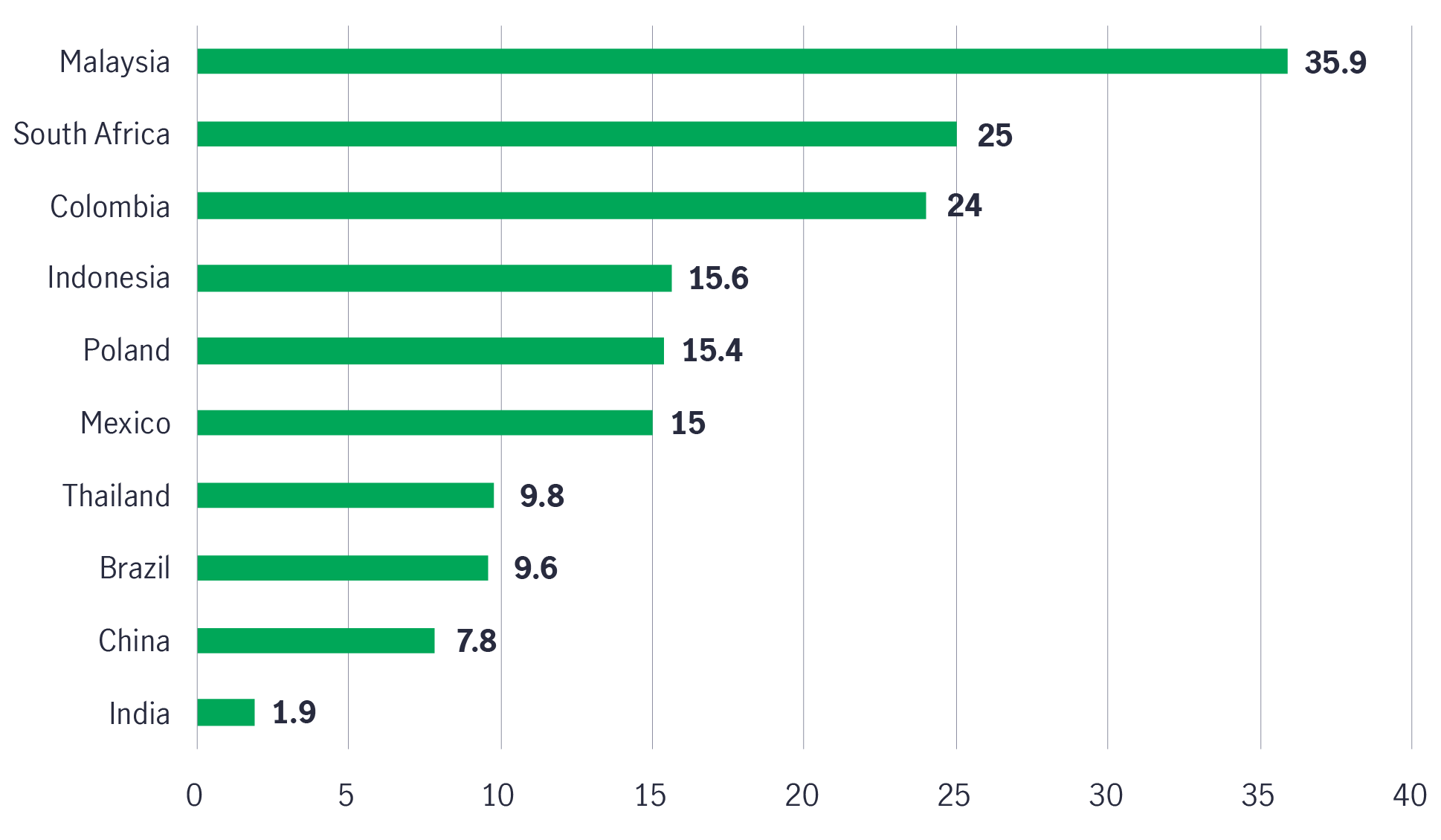

Around 1.9% of the country’s government bond market is currently owned by foreign investors (Chart 1), significantly below other emerging markets, particularly when accounting for India’s economic size as the world’s fifth-largest economy.

Chart 1: Foreign ownership of government bonds in key emerging markets (%)4

JPMorgan’s decision may also spur further foreign investment through knock-on effects and the inclusion of Indian government bonds in other major global sovereign bond indices:

- The Bloomberg Barclays Emerging Market bond index may review India’s inclusion as early as this year, as some investors have pushed for an expedited review before 2024. Inclusion could result in an estimated US$15-$20 billion in inflows5.

- FTSE Russell’s Emerging Market debt index has had India on its “watch list” since March 2021. It is slated to review India’s status in September 2023 for potential inclusion.

The impact of greater foreign investment could lead to numerous structural changes in the government bond market, such as an increase in the number of potential buyers, a potential improvement in overall market liquidity, and a central government that may be more fiscally prudent due to greater external scrutiny.

Ultimately, the potential benefit for foreign investors is that index inclusion will garner more attention and raise the profile of the high-yielding bond market of the world’s fifth-largest economy.

The inclusion also does not come without long-term risks, as India remains an emerging market. Most prominently, substantial inflows into the government bond market may lead the Reserve Bank of India or the government to smooth out its market impact via intervention. Furthermore, it could result in the government increasing net market borrowing and will likely subject the local bond market to greater exposure to changes in global financial conditions.

Investors should remain vigilant and seek out fund managers with experience in the burgeoning but volatile Indian bond market.

Manulife Investment Management capabilities in Indian fixed income

Manulife Investment Management has been investing in onshore Indian bonds in its flagship pan-Asian fixed income strategy since 2016.

In 2020, Manulife Investment Management also created a joint venture (JV) with Mahindra Finance in India6. As one of the few global financial institutions with a presence in India, the JV gives us a distinctive onshore presence with an experienced team of fixed income portfolio managers, analysts, and traders to leverage local market insights and analysis into informed investment decisions.

Having on-the-ground expertise and extensive experience investing in India gives us an edge navigating access to the onshore market on behalf of foreign investors as structural barriers around administrative and settlement-related issues remain for now.

Conclusion

We believe JPMorgan’s index inclusion decision is a welcome first step for India’s fixed income market to attract greater international attention and foreign investment. Indeed, not only should it help bolster India’s already robust macro credentials over the short-term, but also assist the government bond market’s development over the long-term.

With the inclusion of Indian government bonds in other major global bond indices over time, the market should gradually become a key one to watch in Asia’s fixed income universe.

1 JPMorgan report issued on 21 September 2023. 2 JPMorgan report issued on 21 September 2023. 3 Bloomberg, as of 28 September 2023. 4 Morgan Stanley report, as of 22 September 2023. 5 Bloomberg, 22 September 2023. 6 On 29 April 2020, Mahindra & Mahindra Financial Services Limited (Mahindra Finance) completed the proceedings for divestment of 49 percent stake in its wholly-owned subsidiary, Mahindra Asset Management Company Private Limited (Mahindra AMC), to Manulife, a leading global financial services group. Manulife has invested US$ 35 million (~INR 265 crore) in the 51:49 joint venture, which aims to expand its fund offerings, drive fund penetration, and achieve long term wealth creation in India. https://www.manulife.com/en/news/manulife-investment-management-acquires-49-percent-in-mahindra-asset-management.html.

Important disclosures

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The Intercontinental Exchange (ICE) Bank of America (BofA) U.S. All Capital Securities Index tracks all fixed- to floating-rate, perpetual callable and capital securities of the ICE BofA U.S. Corporate Index. The ICE BofA BB U.S. High Yield Index tracks a subset of the ICE BofA U.S. High Yield Index and includes securities rated BB. The ICE BofA Fixed Rate Preferred Securities Index tracks the performance of fixed-rate U.S. dollar-denominated preferred securities in the U.S. domestic market. The ICE BofA U.S. High Yield Index tracks the performance of below-investment-grade U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market and includes issues with a credit rating of BBB or below. It is not possible to invest directly in an index.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or our affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or our affiliates, nor any directors, officers, or employees, shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any affiliates or representatives are providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. Mainland China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

3151481