Fed’s first rate cut of 2025: Implications & takeaways

After nine months on pause, the US Federal Reserve (Fed) announced another rate cut of 25 basis points (bps) on September 17 (US time), bringing the federal funds rate into a target range of 4%-4.25%. Alex Grassino, Global Chief Economist, and Yuting Shao, Senior Global Macro Strategist, share their latest views on the rate decision and its implications for Asia.

Fed rate path in line with our expectations

Alex Grassino

The FOMC’s decision to cut the Fed funds rate by 25 basis points was hardly a surprise. In fact, the markets had pretty much been pricing in this move since Fed Chair Powell’s Jackson Hole speech in late August. As a result, the main focus was on what the Fed might do next and when.

Bottom line: Against a backdrop where the Fed's forecasts call for slightly better growth, slightly firmer inflation, and a slightly lower unemployment rate, Fed watchers should expect the central bank to deliver more rate cuts in the coming months. At this point, the “dot plot” is signalling that a reasonable base case would be for the Fed funds rate to be 50 bps lower by year-end 2025, with one additional cut likely in 2026. This rate path would be in line with our own expectations between now and the end of Fed Chair Powell’s term next May. Where we differ from the Fed’s latest projections is that we expect new Fed leadership to continue easing interest rates toward neutral, which we currently have at 3%.

Asian economies and assets stand to benefit

Yuting Shao

The much-anticipated Fed rate cut in September should bring positive momentum for emerging markets (EM) as the resumption of the Fed easing cycle loosens financial conditions, boosts investor sentiment, and generally bodes well for risk assets. Asian economies, and assets in particular, should also stand to benefit via the following channels:

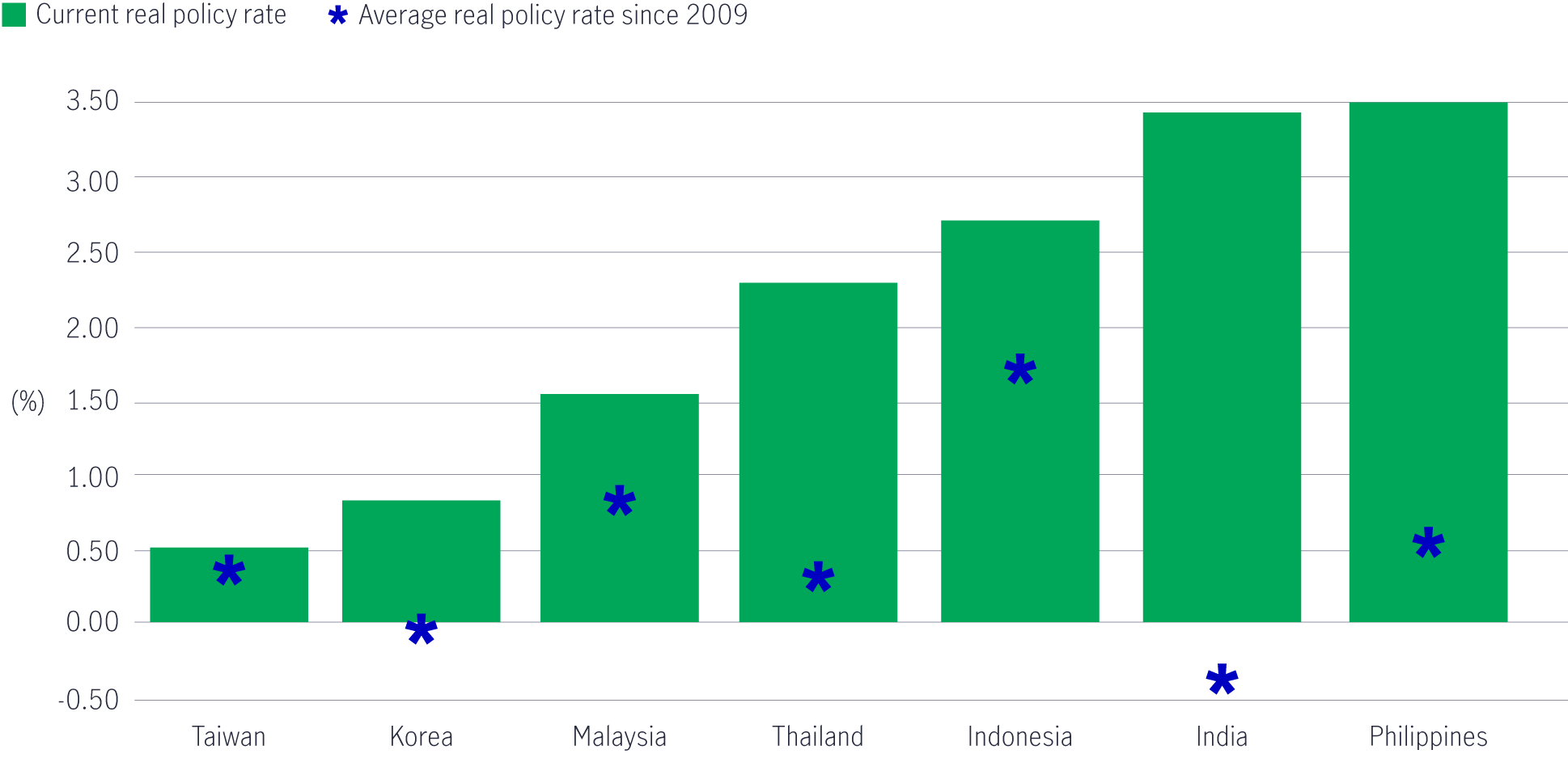

1. Central banks in Asia have more room to cut policy rates to support growth

Despite continued disinflationary trends across most economies in the region and lower oil prices, policymakers have been mindful of interest-rate differentials with the US, given that narrowing differentials could trigger capital outflows and currency depreciation (we will elaborate on these two points later). For the first half of 2025, most Asian central banks maintained a cautious approach toward monetary easing despite high real policy rates (the nominal policy rate minus inflation). The Fed’s September rate cut and the expectation of further easing in the coming months should give Asian central banks the space to introduce policy rate reductions to boost their economies. Another surprise rate cut by Bank Indonesia earlier this week is a case in point.

Although growth stayed resilient amid the front-loading of trade and bilateral trade agreements between the US and many Asian economies that helped alleviate tariff uncertainty, the fact that most economies in the region run a current account surplus means the risk of “payback” and slowing exports will weigh on growth. To that end, having more room for central banks to ease will improve the regional macroeconomic outlook.

Chart 1: Key Asian central bank policy rates (real)

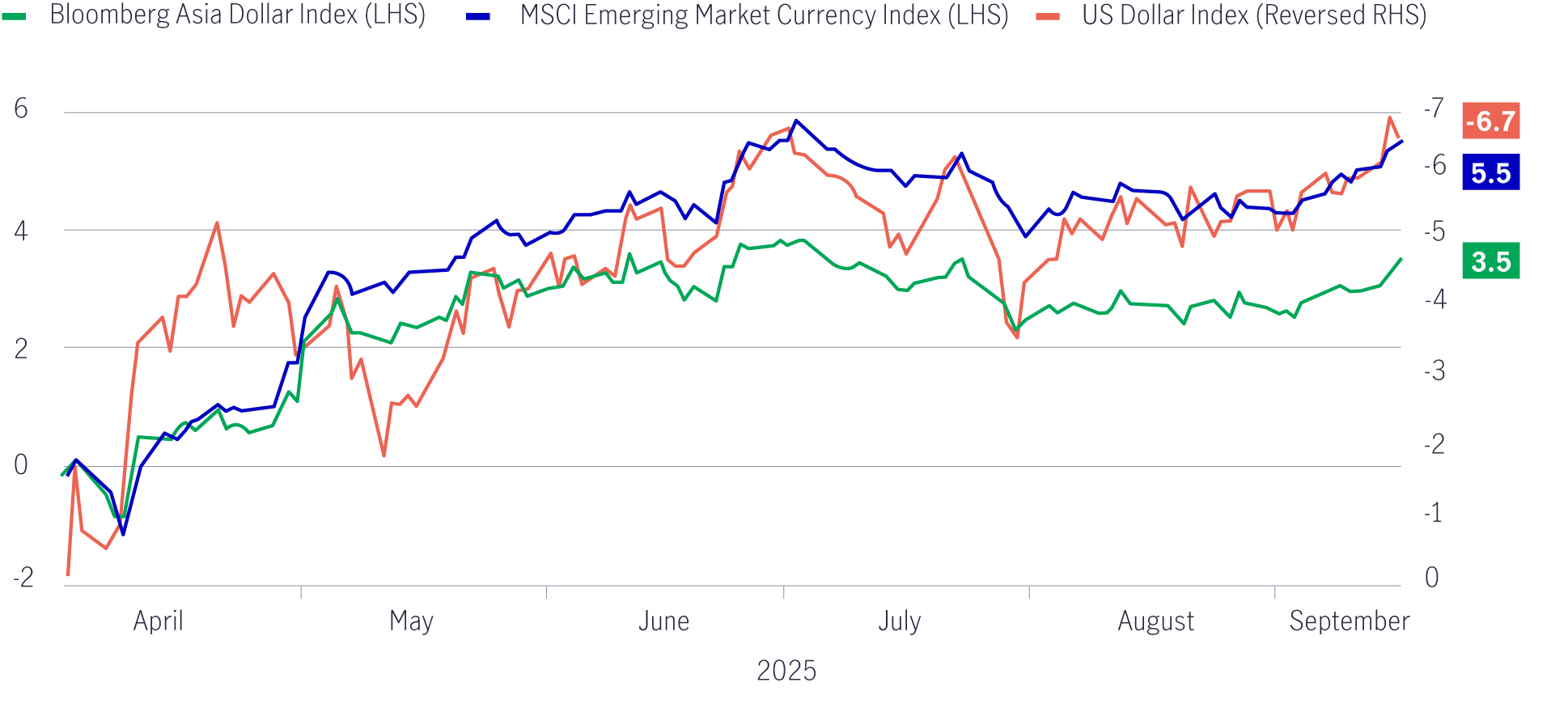

2. A weaker US dollar supports the positive outlook for Asian currencies

In our opinion, although the Fed is likely to stay data dependent, the rate cut in September and further easing expectations put pressure on the US dollar. What’s more, recent developments surrounding the Fed’s independence confirm our belief that there is a structural trend of greenback weakness. Asian currencies have largely underperformed their EM peers since “Liberation Day” on April 2, given the higher tariff risk they face. However, with lower inflationary pressures and a weaker US dollar, EM Asia currencies have the scope to catch up in an environment where volatility remains low, especially for high yielders in the region. That said, we note the caveat that recent domestic political developments, especially in ASEAN economies, could impact macro policy and investor sentiment.

Chart 2: Asian currencies underperformed EM peers since Liberation day (Cumulative returns, %)

3. The Asian market can attract continued capital inflows as the Fed rate cut underpins an improved risk appetite

Asia has been on the receiving end of global inflows over the past few months, riding on the boom of the artificial intelligence (AI) and information technology themes, as well as recovering investor interest in China equities. Although the valuation edge has waned given the recent outperformance, Asian equities remain undervalued compared to many of their developed-market counterparts. On top of Asia’s relatively resilient growth, benign risk, and accommodative monetary policy backdrop, corporate reforms in major markets (including mainland China, South Korea, Japan, and Singapore) aimed at enhancing corporate governance, improving profitability and returns, will likely attract more foreign investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional

Australia: : Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. Mainland China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area: Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which

is authorised and regulated by the Financial Conduct Authority

United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.