What happens in a recession?

With recent tariffs, drops in global markets, and stock market worries, you might be anxious about what comes next—like the possibility of a recession. But what exactly is a recession, what causes one, and what happens when it’s under way?

What’s a recession?

From a technical standpoint, a recession is often defined as two consecutive quarters of shrinking GDP. What does that mean? Think about a cold day in the middle of the summer. It’s unpleasant (and annoying), but you just swap shorts for jeans, and by the next day, the weather is back to normal. That’s like the general ups and downs of the market—there are small changes. Now think about winter. For long periods, trees are bare, people stay indoors, and there’s a general sense of gloom. That’s what a recession feels like—for at least six months, the economy slows down, people spend less, and there are fewer jobs.

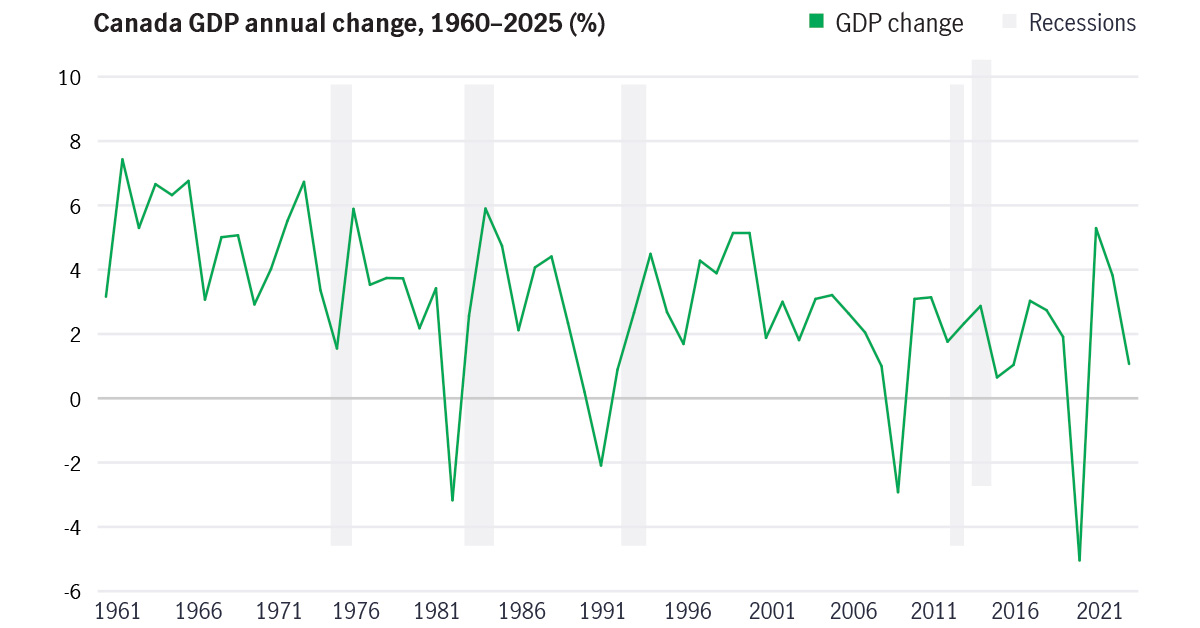

When were the most recent recessions in Canada?

Canada’s most recent recession started in the early days of the COVID-19 crisis. That recession began in March 2020 and ended in April 2020, making it the shortest (but deepest) recession in Canada.

Front and center in the years leading up to the COVID-19 pandemic was the Great Recession, which began at the tail end of 2008 and continued until May 2009. Real GDP fell roughly 4.3% from its pre-crisis level, and unemployment peaked at 8.5% during 2009 (the rate was 6% at the start of the crisis). While similar developments unfolded in the United States, unemployment didn’t peak there until October 2009, suggesting that the end of a recession doesn’t necessarily mean the end of economic distress.

Shorter yet milder recessions in Canada were fueled by the bursting of the dot-com bubble in 2001, the first Gulf War in 1990/1991, and central bankers’ attempts to rein in inflation in 1981/1982.

Source: Canada GDP 1960–2025 | MacroTrends, 2025.

What causes recessions?

Recessions generally stem from declining confidence, a sense among businesses and consumers that the economic tide is turning. Recessions are often the result of structural changes in one or more key industries, economic shocks, or even psychological forces such as extreme optimism (which can lead to speculative behaviour). Financial bubbles bursting (e.g., the stock market crash of 1929 and the real estate crash of 2007) can also be the cause of recessions. Recessions can also be provoked by central banks (e.g., the Bank of Canada) as they try to lower inflation by raising interest rates and may accidentally, or sometimes even knowingly, cause a recession.

What happens in a recession?

- Unemployment often rises—Unemployment typically rises as businesses cut back or shut down, but the degree of disruption can vary. The unemployment rate reached as high as 9.8% in Canada during the relatively mild recession of 1990/1991, yet it continued to increase after the recession was declared over.

- ·People may save more—People who still have their jobs tend to spend less in recessions, worried they may become unemployed, while those who are already unemployed cut back on spending. As more people reduce their spending, the result can be a negative economic spiral (since consumer spending makes up a large part of the economy), leading to progressively lower incomes, higher unemployment, and an extension or deepening of a recession.

- Prices can fall—Severe recessions can lead to deflation—a general decrease in prices— especially on discretionary items (e.g., travel and alcohol) and real estate. In this environment, spending focuses on necessities, such as housing and groceries.

- Liquidity can dry up—Banks become less motivated to lend in recessions for fear of not being repaid, so it may be harder to take out a loan. Interest rates also tend to fall, shrinking banks’ profit margins.

- Deficits can increase—Governments often increase spending to offset the recession’s effects. At the same time, tax receipts fall as corporate and personal incomes decline.

How should you invest during a recession?

Just like in good economic times, investing during a recession really comes down to being properly diversified. By investing across various asset classes, geographic regions, and management styles, an investor can take part in up markets and avoid the whims of panic selling in down markets.

Unfortunately, there are no recession-proof asset classes, but it’s worth exploring how two of the most central components of investor portfolios tend to respond in this environment.

- Bonds—Investors often turn to bonds to help cushion the impact of stock market downturns. While they’re a far cry from being risk-free investments, bonds offer a steady stream of interest income and are generally viewed as safer investment alternatives in times of uncertainty.

- Stocks—Stocks often pull back ahead of recessions, but by the time the recession happens, it’s usually too late. Since recession concerns are usually baked into stock prices, it’s harder to use them as a reference point for predicting a recession. In fact, not only are falling markets poor predictors of recessions (the 1987 crash didn’t lead to one), but recessions don’t necessarily imply stock market declines either.

Is a recession coming?

Is Canada headed for a recession? It’s impossible to say for sure. While some economists think it’s likely, others are less sure. It’s important to remember that even when these events are predicted, they don’t always happen. There was chatter on the possibility of recessions in 2022 and 2023, but Canada managed to avoid that fate.

The beginning of a recession can only be confirmed after it has actually started, so it’s entirely possible for an economy to be in a recession without investors even knowing it.

What is certain, however, is that cycles happen. Markets rise and fall, and this includes recessions. Navigating through these cycles can be unsettling, but it’s important to stay focused on a long-term end goal and remember that recessions come and go. This is especially important when you’re considering your retirement investments. Whether you’re retiring in several decades or much sooner, a lot can change in a few years. It’s best not to make any impulsive decisions on money you won’t be using immediately. Revisiting your investment strategy in this context is vital, but keeping your emotions in check is equally important.

Important disclosures

Important disclosures

This content is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made.