To versus through glide paths: what’s the difference?

As a plan sponsor of a retirement plan, staying up to date with the strategies that can help members navigate retirement risks, including the risk they face of outliving their savings due to longer lifespans, can be important. We can help you understand how target-date funds and different glide path designs can help your members achieve financial resilience.

This viewpoint is part of our latest analysis, “Analyzing the merits of through versus to glide paths,” which is designed to help guide your retirement planning decision-making.

Your role in helping members retire comfortably

One of the most significant changes in retirement planning has been the move from defined benefit pension plans to defined contribution plans. This transition has shifted much of the financial responsibility and risk from employers to employees, but there’s a general concern that individuals may not possess the investing expertise needed to navigate long-term financial stability. That’s where you step in. As a plan fiduciary, you play a pivotal role in selecting the plan’s default investment options, which many members may end up holding throughout the life of their plan.

Target-date funds are a viable option for the default investment selection because they offer a diversified and professionally managed strategy targeted toward a planned retirement date. How do you know which target-date fund is the right one for your plan?

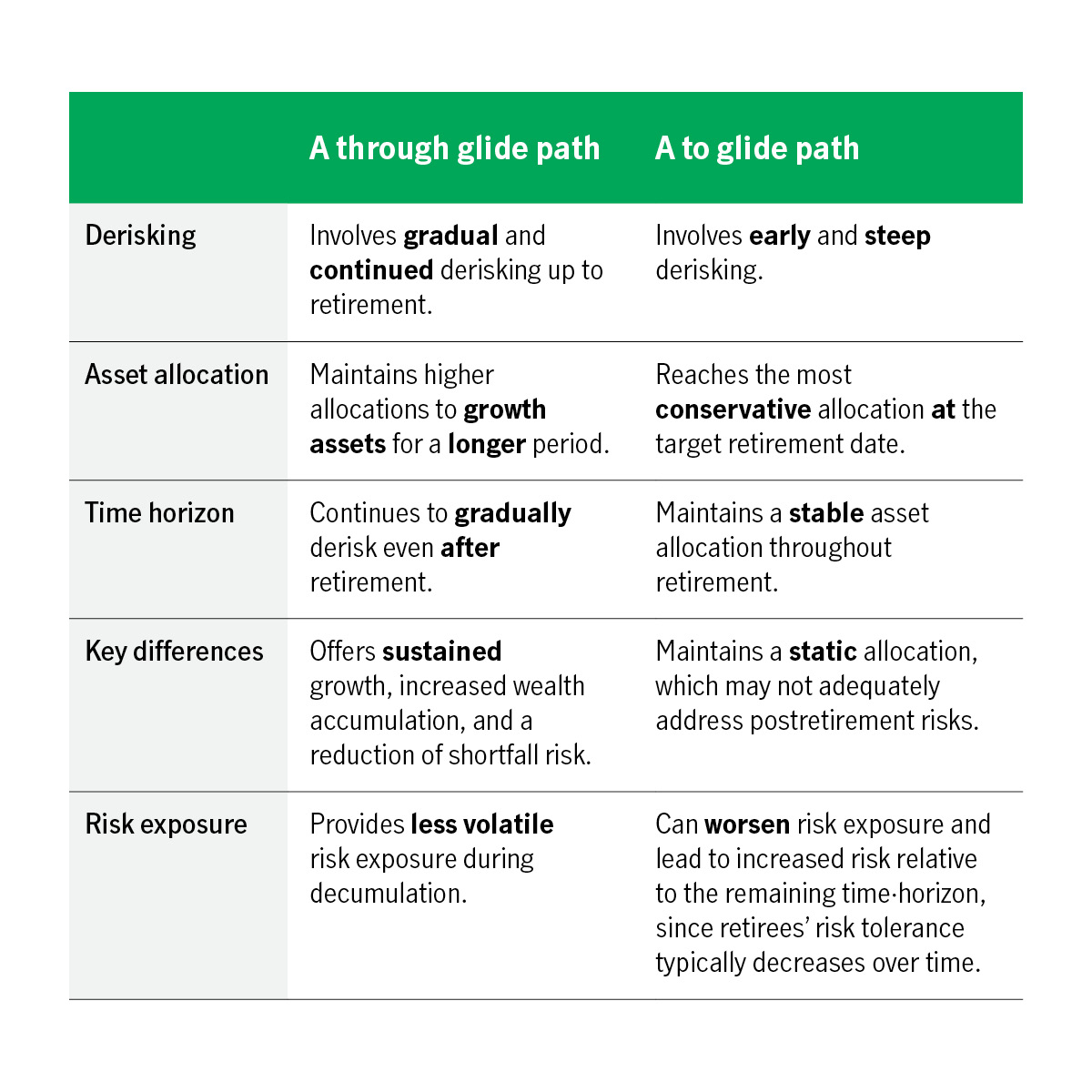

To and through have different glide path designs

A glide path is the asset allocation over time within a target-date fund. It shows how and when the allocation changes to balance growth potential with risk management.

Each target-date fund has its own glide path design to manage risk differently. One of the key differences between to and through glide paths is that the to path becomes static during the decumulation phase, whereas the through path continues to invest using an accumulation strategy. Plan sponsors should consider your members’ demographics and assess how each glide path would address their needs.

To vs. through glide paths: a deep dive

Consider members’ risk exposure when choosing default investments

Based on life expectancy today, Canadians could live decades longer than anticipated.1 Glide paths can address the risk many people have of running out of money in retirement, both before and after they retire. Understanding the differences between glide path strategies in target-date funds can help you select the best options for your members.

Glide path design can mitigate retirement risks

Explore target-date fund options and download our analysis to start enhancing your retirement offerings.

Want to explore target-date fund options?

Connect with your Manulife representative on how to pick a suitable glide path according to your members’ retirement goals.

Important disclosures

Important disclosures

The commentary in this publication is for general information only and should not be considered legal, financial, or tax advice to any party. Individuals should seek the advice of professionals to ensure that any action taken with respect to this information is appropriate to their specific situation.

1 Office of the Chief Actuary, Government of Canada, December 14, 2022. Latest published information.