Get your head in the game!

Coaching your clients through important investment decisions.

The topic of cognitive bias, or the mental shortcuts our brains take to make faster decisions, is becoming better understood. Over millennia, we’ve adapted and honed our responses, which have come in handy for keeping us safe – whether it’s running from a predator or turning on the light so we don’t fall down the stairs. But these biases, developed as they are to save time and keep us alive, can be detrimental when it comes to more complex decisions, such as those related to investing. Because we don’t always have access to all the information, it can be challenging to make certain decisions when our emotions are also being triggered. That’s the point where an advisor can be in a good position to offer an objective point of view and coach clients through the tough choices.

Should I stay or should I … run!

Let’s say you’re out foraging for berries, and you think you see what may or may not be a tiger in the tree line. What do you do? Do you stand there and think about the last time a tiger chased you, weighing the pros and cons of eating berries for dinner or being dinner, or do you make the decision to flee in a millisecond? Of course you run, even if that’s not actually a tiger lurking in the trees. This is an example of an emotional decision. When we act emotionally, our brain takes a small amount of information and makes a fast choice. While a swift decision might be the right one when facing a tiger, speed may not be wisest when it comes to financial decisions, especially when savings and retirement goals are on the line.

These reactions can come into play even in a mundane, everyday situation. Consider the grocery store. We go there with a budget and a plan to stock up on fresh fruits and vegetables, but retailers understand how to tap into shoppers’ emotional side. Chips and cookies can evoke feelings of pleasure, so the store will proudly display them front and centre, often at the entrance. Even though you’ve gone to the store with a solid plan, a few emotional purchases might pull it off track.

Similarly, with investing, the best of intentions can be derailed by temptation. Advisors have a unique vantage point that can help clients evaluate potential emotional reactions, by looking at market events objectively and explaining them in a way that can hopefully avoid a knee-jerk reaction from clients.

Do as I say, not as I do

There’s a familiar saying, “The path to ruin is paved with good intentions,” but sometimes our good intentions don’t line up with our actions. In fact, what people say and do are sometimes complete opposites. Let’s consider the common scenario where you’ve spent time building an investment plan with a client. You’ve done all the preparation and provided product comparisons, and the plan is received well – but then nothing. The client takes no action. The reason may be status quo bias, which is the tendency to prefer the current situation to making a change.

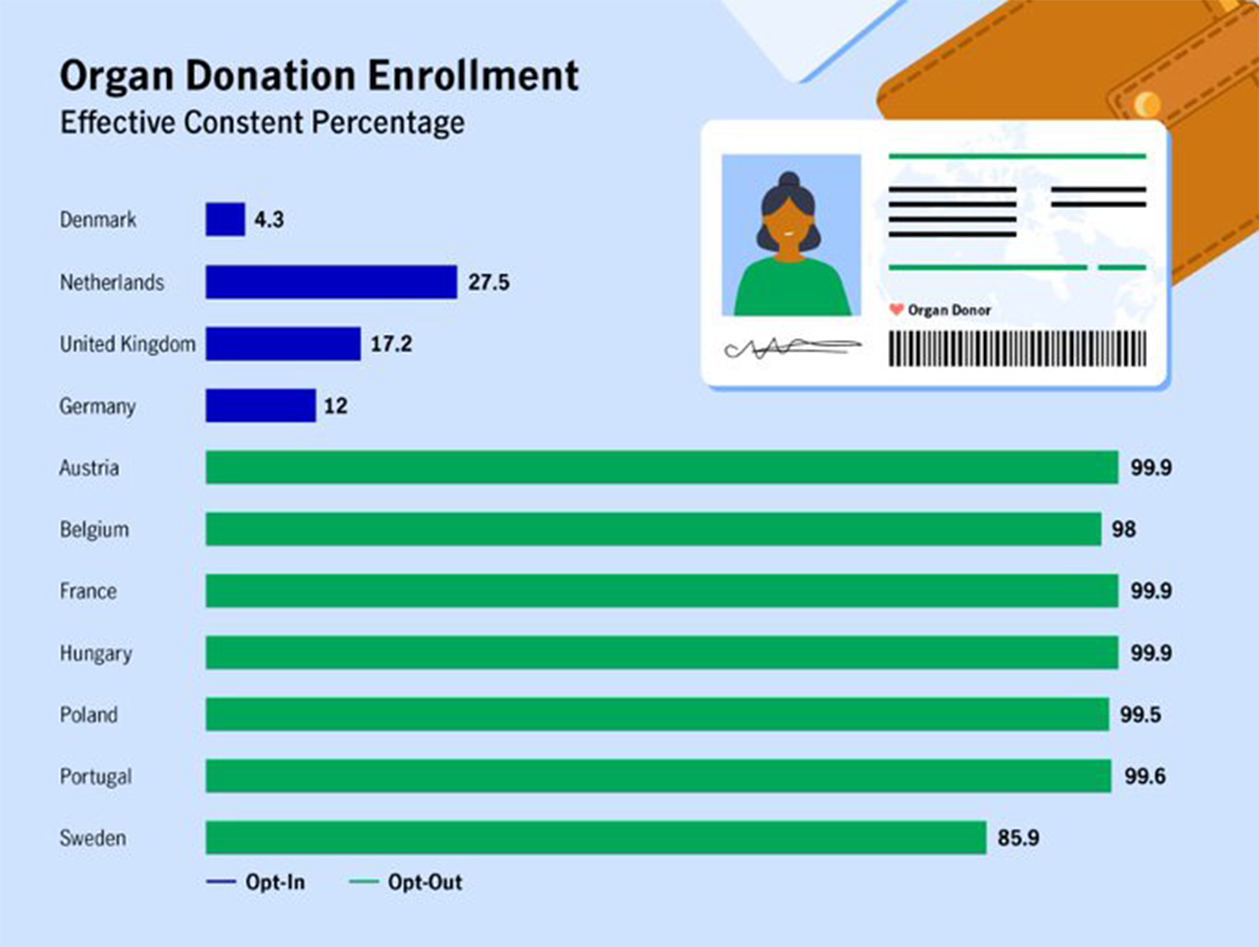

Let’s look at another example of status quo bias. In some countries, when a person obtains a driver’s license, the default option is to be an organ donor. If they don’t want to donate their organs, then they must “opt out.” Other countries have an “opt in” policy, where the new driver must take specific action and make the decision to become a donor. As the graph below illustrates, the power of the status quo is quite strong. In the countries where citizens must make an active choice to opt out, the vast majority consent to be donors.

Status quo bias can pose significant challenges for clients, especially when it comes to saving for retirement. In company-sponsored retirement plans, for example, all that’s required to opt in is to sign a form. Then the company does the rest, which often includes matching employee contributions up to a certain amount. In theory, this would seem very beneficial for the employee, as it represents free money and additional savings. But in a study that examined the power of suggestion, what came to light is that it can be very hard for employees to take the step of opting in. This is where a default may be useful. The study found that employees would be fine with a 3 per cent default opt-in to a company retirement plan, but that it wouldn’t be enough to realize retirement goals. However, employees are reluctant to change the percentage because they believe that the default “must be enough.” This illustrates the power of the status quo bias, but also highlights a good way of handling bias using defaults.¹

Play ball!

When coaching clients, there are several ways to get around biases that you could try. Take the concept of pre-commitment. This strategy prepares the client for dealing with choices by making a decision and setting a date by which they will take action. Imagine a large inheritance, as an example. The client may know they are going to receive it, but the events immediately preceding the inheritance may leave them in a heightened emotional state. By encouraging a plan or a pre-commitment on what to do with the proceeds, some of the emotion is removed from the decision.

Defaults and fresh start date interventions are additional useful tactics. Let’s say you’re trying to encourage a client to start investing on a regular basis. You could set up a preauthorized monthly deposit, and this becomes the default part of the plan. To encourage action for regular deposits, consider having the client choose a meaningful start date, such as a birthday or anniversary. This fresh start date can kick-start a habit of regular investing.

But I want it NOW!

When asked if they would like $100 now or $110 in three days, most study participants chose the $100.¹ This represents present bias, or a preference for a smaller reward sooner, rather than waiting a bit longer for something better. This bias can be a significant derailer for retirement portfolios. A new car, a jet ski or a lavish vacation can all be spontaneous purchases with significant effects on a portfolio down the road. What’s interesting, though, is that when the timeline is extended, people tend to make a different choice. When participants were asked whether they would like $100 in a year, or $110 in a year and three days, almost all participants agreed to wait the extra few days for the increased reward.

With another group, participants were asked how they’d feel if they won $10, and “pretty good” was a typical response. But when asked how they would feel if they lost $5 out of their wallet, the overwhelming reaction was sadness. This reaction to losing a smaller amount of money dwarfed the good feeling of winning a larger amount, which is an example of loss aversion bias. In general, we feel twice as strongly about losses than we do about gains.

In cases where clients are demonstrating present bias or loss aversion bias, it’s important to frame things a bit differently. When talking about risk, for example, illustrate the potential losses that could arise from taking too little risk. Sitting in cash during an economic expansion could result in real losses due to inflation. Illustrating the value of being invested in a portfolio with a suitable amount of risk for your client would mitigate the loss aversion bias by framing the scenario in a better light.

Helping the client see the other side of the coin can also be helpful when it comes to present bias, or the preference for smaller rewards and instant gratification. In these situations, it’s helpful to have the client cue their future self. That new car, boat or frivolous treat may be nice, but how will these choices impact the long-term growth of their portfolio? Help your clients to imagine the future they want and the type of retirement or savings goals they have. Then, factor in too much current spending and ask them what they think that will do to the picture they have painted in their heads.

It still always comes down to building trust

These examples only scratch the surface of the topic of behavioural economics and how the biases we have can affect our investment decisions. But developing effective strategies to overcome these biases can be an excellent business-building tool for advisors. Consider what your clients are reacting to: not whether the market goes up or down, but rather how monetary gains or losses will affect their lives. It’s important to build trust by helping your clients understand their life outcomes and goals rather than simply focusing on making money. Be their true-blue financial friend, not just a friend in fair weather.

To gain greater understanding of the subject and the insights offered, read our white paper here.

1 Lerner JS, Keltner D. 2001. Fear, anger, and risk. Journal of personality and Social Psychology 81: 146-59 1 Thaler & Bernatzi, 2010; Madirian & Shea. The power of suggestion: Inertia in 401(k) participation and savings behavior (2001)

Important disclosures

Important disclosures

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the fund facts as well as the prospectus before investing. Mutual fund securities are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. There can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated. Manulife Funds and Manulife Corporate Classes are managed by Manulife Investments, a division of Manulife Asset Management Limited. Manulife, Manulife & Stylized M Design, Stylized M Design and Manulife Investments are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.