Growing your small business niche

How group benefits can open the door to opportunity.

Small business is big business in Canada, with an estimated 1.2 million construction companies, dental offices, tech firms and more employing millions of people. Attracting and keeping top talent is always a challenge and increasingly, small business owners are feeling the pressure to get creative with incentives This presents an opportunity for advisors who can assist businesses of all sizes in setting up extended health and dental benefits for their staff.

In a recent Harris Poll commissioned by Express Employment Professionals, Canadian companies say they are experiencing an increase in employee turnover, with the most common reasons being advancement opportunities offered elsewhere (42%) and better pay/benefits (37%).¹

James Baggs is an account executive with Manulife’s group benefits team who works directly with advisors in southern Alberta, guiding them through the group benefits process. He says there’s an array wealth of untapped potential that can flow from a single small business inquiry.

“Small business owners are certainly under increased pressure to attract and retain top talent, and group benefits has a big role to play in overall employee satisfaction,” says James. “What are the costs to an employer if they lose a key employee, particularly in a small business? Significant time can be spent on hiring and training the right person.”

Manulife has plans for groups as small as two people, creating the opportunity to start a conversation with even the smallest business owner. And with annual recurring commissions, group benefits can offer earnings stability for an advisor’s business.

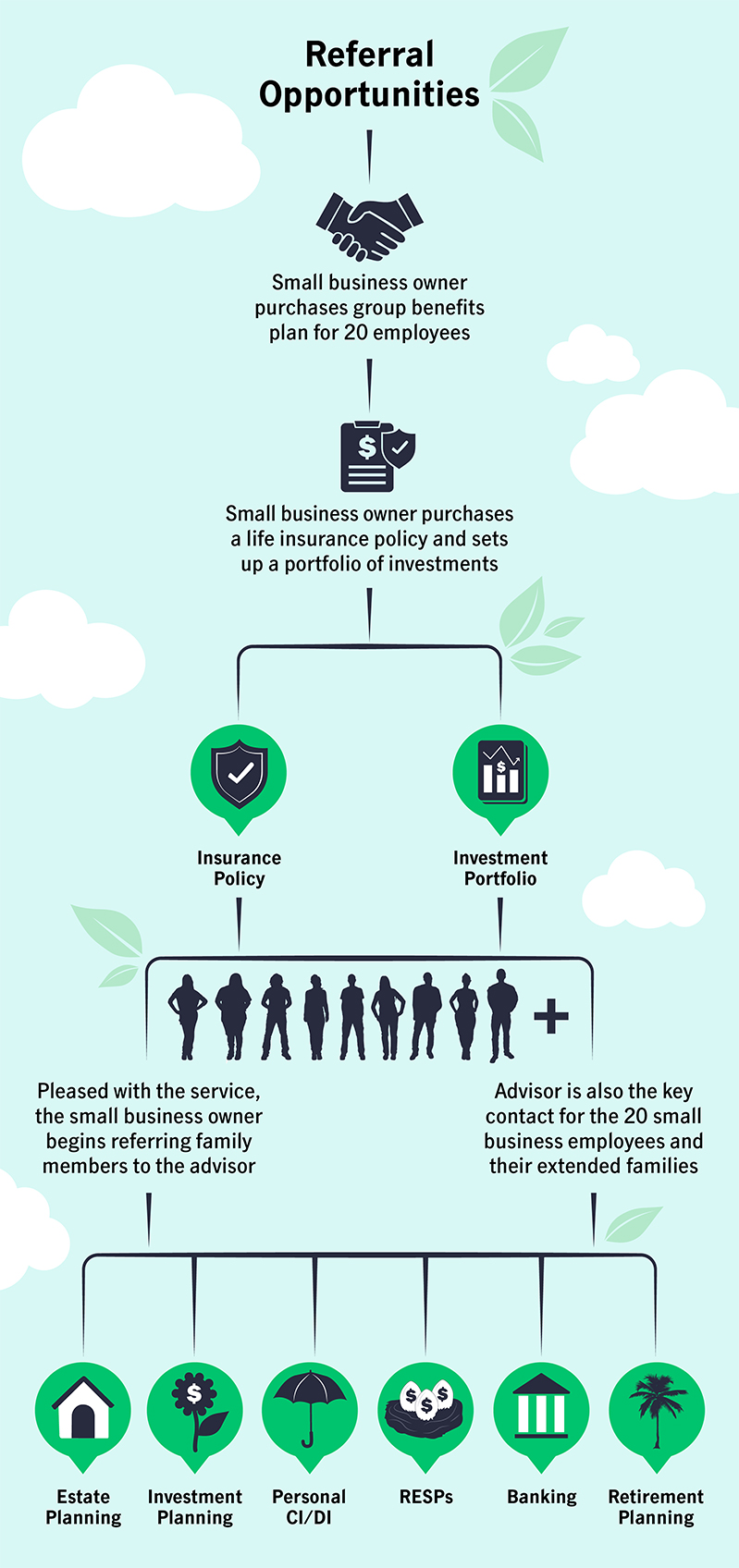

Group benefits gateway

An advisor’s core business may focus on life insurance or wealth management, but sometimes an opportunity can present itself through referrals. For example, an advisor receives an unexpected request from an existing client who wants help in setting up employee benefits for their small business – a restaurant with a staff of 20. The advisor doesn’t have any experience in this area, but also doesn’t want to miss out on a chance to prove their worth.

“By thinking beyond your core business, group benefits can be the perfect gateway for showing value to a high net-worth client,” says James. “Building trust can lead to warm discussions on what an advisor can do for them above and beyond group benefits.”

In addition, by setting up a business owner with group benefits, an advisor could become a key point of contact for the employees of that company, who may be looking for guidance on life insurance, investments, and estate planning.

Support through the entire group benefits process

If you’re an advisor located in southern Ontario, there’s a chance you might have a connection to Jeff Anstett, another Manulife group benefits account executive.

“Much of my time is spent with advisors who have never been involved with group benefits before,” says Jeff. “They might have wealth or insurance clients who now want to get group benefits for their business.”

The role of an account executive is to assist with advisor education on the group benefits process – which includes comprehensive guidance on the entire sales cycle from initial inquiry to successful implementation of a benefits plan.

When Jeff begins working with an advisor, it starts with listening.

“I have the advisor tell me about the opportunity and learn what is motivating the small business owner to seek out benefits,” says Jeff. “Are they looking for group benefits because they’re growing and want to attract and retain top talent? Or are they looking at their employees’ wellness and productivity? I want a small business owner to know how group benefits can help create loyalty to a workplace while also being more proactive with healthy living – which encourages employees to be more productive and reduces absenteeism.”

The next step is helping an advisor to design a plan. Your account executive can help you with this and can also create a benchmarking report that compares group benefits plans for a particular industry and region in Canada. This helps to ensure the group plan is as competitive as possible.

“Many advisors don’t know group benefits, so I spend the majority of my time making the process easy to understand, which in turn helps the advisor to feel confident about presenting a plan to his or her small business client,” says Jeff. “My goal is to make the advisor feel like getting involved in group benefits is simple and straightforward. I want an advisor to feel comfortable working with me to help them design a plan that will work for their client.”

When a quote is prepared, an account executive will help the advisor prepare for the client meeting, which can involve role playing and presentation practice.

“I make sure the advisor understands the nuances of a plan,” says Jeff. “For example, Manulife Vitality2 is a unique value-add included in our plans, so it’s important that advisors are aware of all the Vitality benefits when presenting a quote to their client.”

Manulife differentiator

Depending on the industry, a group benefits plan can be customized in unique ways. For instance, what works for a construction firm may be quite different to that of a tech company. Group benefits plans aren’t cookie cutter – they work best when a small business owner is providing what the employees want.

But wellness is a growing priority for many business owners across all industries.

“Manulife is investing in employee health to make the plan sponsors more profitable,” says James. “Manulife Vitality Group Benefits – available exclusively through Manulife in Canada - is a big differentiator that makes it easy for small business owners to promote healthy lifestyle options for employees.”

Take a restaurant, for example. Staff are on their feet and moving, so by connecting a mobile phone or wearing a fitness tracker linked to the Vitality program, these employees can complete challenges to easily earn weekly rewards such as gift cards. When they reach silver status, they become eligible to receive a 40 per cent discount off a Garmin smartwatch³.

And the research suggests the same. According to the 2017 Happiness Calibrator Vitality member survey⁴, there was a 78 per cent increase in respondents reaching high levels in the Vitality program over three years and a 15 per cent decrease in claims. 91 per cent said the Vitality program had a positive effect on company culture and 92 per cent reported an improvement in their overall health and wellbeing. Healthier staff reported lower levels of sickness and feeling distracted at work. The lower claims can translate to lower premiums over time – a significant improvement for a client’s bottom line.

It’s easy to get started!

It may feel like a bit of effort to shift gears into group benefits, but the support is there to help navigate the process.

“Advisor feedback is very positive in terms of the support offered by Manulife,” says Jeff. “Quotes are prepared quickly, account executives spend the time to ensure advisors understand everything well before presenting to their client, and there is a larger Manulife support team that includes plan administration, customer service and renewals.”

Your Manulife account executive is also available to assist you in client meetings and presentation training to help with closing a deal. “At the end of the day, an advisor can tell me that I took a very intimidating and complex product and made it easy enough for them to present to their client.”

Along with competitive compensation, there’s an increasing expectation that employees will have some type of extended health coverage through a company benefits plan. When there’s an opportunity to help a small business owner with a group benefits request, the advisor has support in place to help make the process as smooth as possible.

For more information about getting involved in Manulife Group Benefits, visit the Group Benefits section of Advisor Portal.

1 Harris Poll commissions by Express Employment Professionals, Dec. 8, 2021. 2 *With some exceptions, Manulife Vitality will be available for members on an employer-sponsored group benefits plan with extended health care coverage. The Vitality Group Inc., in association with The Manufacturers Life Insurance Company, provides the Manulife Vitality Group Benefits program. Vitality is a trademark of Vitality Group International, Inc., and is used by The Manufacturers Life Insurance Company and its affiliates under license. Manulife, Manulife & Stylized M Design, and Stylized M Design are trademarks of The Manufacturers Life Insurance Company, and are used by it, The Vitality Group and its affiliates under license. ©2022 The Manufacturers Life Insurance Company. PO Box 2580, STN B Montreal QC H3B 5C6. All rights reserved. 3 Reach Silver status and receive a 40% discount for a health and activity device at Garmin.ca. Eligibility and availability of rewards are not guaranteed and may change over time. Insurance and Group Benefits are provided by The Manufacturers Life Insurance Company. Employer-sponsored group benefits programs are provided by The Manufacturers Life Insurance Company. The Vitality Group Inc., in association with The Manufacturers Life Insurance Company, provides the Manulife Vitality program. Please consult your human resources department to learn more and find out if Manulife Vitality is available for your workplace. © 2019 Tim Hortons, 2019 Cineplex® Entertainment LP, ©2019 Indigo. All rights reserved, © 2020 Footlocker.com, Inc. All Rights Reserved, © 2020, Hudson's Bay Company, Garmin is a registered trademark of Garmin Ltd. or its subsidiaries. 4 https://www.manulife.ca/business/group-benefits/vitality.html

Important disclosures

Important disclosures

© 2022 Manulife

FOR ADVISOR USE ONLY.

As one of Canada’s largest integrated financial services providers, Manulife offers a variety of products and services including insurance, living benefits, segregated fund contracts, mutual funds, annuities and guaranteed interest contracts. The persons and situations depicted are fictional and their resemblance to anyone living or dead is purely coincidental. This media is for information purposes only and is not intended to provide specific financial, tax, legal, accounting or other advice and should not be relied upon in that regard. Many of the issues discussed will vary by province. Individuals should seek the advice of professionals to ensure that any action taken with respect to this information is appropriate to their specific situation. E & O E. Manulife Mutual Funds and Manulife Exchange‑Traded Funds (ETFs) are managed by Manulife Investment Management (formerly named Manulife Asset Management Limited). Manulife Investment Management is a trade name of Manulife Investment Management Limited. A division of Manulife Asset Management Limited. Commissions, trailing commissions, management fees and expenses all may be associated with investments in the Manulife Mutual Funds and Manulife ETFs. Please read the ETF facts/fund facts as well as the prospectus before investing. The Manulife Mutual Funds and Manulife ETFs are not guaranteed, their values change frequently and past performance may not be repeated. Any amount that is allocated to a segregated fund is invested at the risk of the contract holder and may increase or decrease in value. Manulife, Manulife & Stylized M Design, and Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license. www.manulife.ca/accessibility