Positioning in the looming stagflation environment

Geopolitical tensions are increasingly clouding the global growth outlook. We gauge the potential impact on markets and share our latest asset allocation view amid rising inflation and lower growth.

Russia’s invasion of Ukraine is one of the true black swan events of recent years, and the raft of sanctions imposed could certainly affect global economies. As our Global Chief Economist and Head of Macroeconomic Strategy Frances Donald noted, there are three aspects we need to consider when assessing the macroeconomic impact of the recent geopolitical conflict:

- Another stagflation shock makes the prospect of a return to Goldilocks conditions by year end look less than solid

- More dovish commentary is expected from the Bank of Canada, Bank of England, and, most notably, the European Central Bank

- The theme of global desynchronization should become more important throughout 2022—Europe is most exposed to growth destruction from higher energy prices

What’s changed and our current assessment

Following the raft of sanctions imposed on Russia, interest-rate futures immediately reflected the prospect of a lower-than-expected interest-rate hike by the U.S. Federal Reserve (Fed) in March, that is, a 25-basis point (bps) rate rise became the consensus view.¹ In response, some European government bonds have rebounded.

Earlier this year, before the military conflict started, we had a slightly positive view on Europe for 2022 as it possesses multiple growth drivers. Indeed, the latest readings of the region’s Purchasing Managers’ Indexes appear reasonable; however, given the raft of sanctions imposed,² we have started to look at Europe less positively.

At the time of writing, the Russia-Ukraine situation remains fluid. As such, here's our current base-case assessment:

- We believe that geopolitical events and a stagflationary outlook won’t lead to a global economic recession at this point; however, a rapid deterioration of the conflict and the introduction of more severe sanctions against Russia may significantly weaken the global economy (subject to the scale of the conflict and its duration)

- Europe, as Russia’s major trading partner, would be most affected, and capital flows will likely return to the United States

- Lower rate-hike expectations

- Commodity-driven inflation is driving the need for inflationary hedges

Potential impact to broad asset classes

The U.S. dollar continues to be supported

The prospects of a more sustained stagflationary shock, exacerbated by recent events, have led to adjustments in our asset allocation positioning. As such, we believe that persistent volatility and more frequent bouts of risk aversion will occur in the first half of 2022. The United States is still on an above-trend growth path³ at this point amid the expected resumption of shale energy demand—we think the U.S. dollar will continue to be supported, attracting capital inflow into U.S. assets.

Equities: geographical and sector

Within developed markets, we favor U.S. equities over their European counterparts. Versus other regions, we believe the United States will be minimally affected by sanctions imposed against Russia. Within the United States, the energy and defense industry should expect to see higher substitute demand. For example, the United States will likely play a more important role given the country’s ban—along with the United Kingdom—on Russian oil exports, as it can provide shale energy.

Given weaker economic growth momentum, coupled with ongoing geopolitical uncertainty, we expect equity markets to experience heightened volatility; however, markets with significant exposure to energy and materials (as inflation hedges) and consumer staples (as a defensive play) may find some insulation thanks to higher commodity prices.

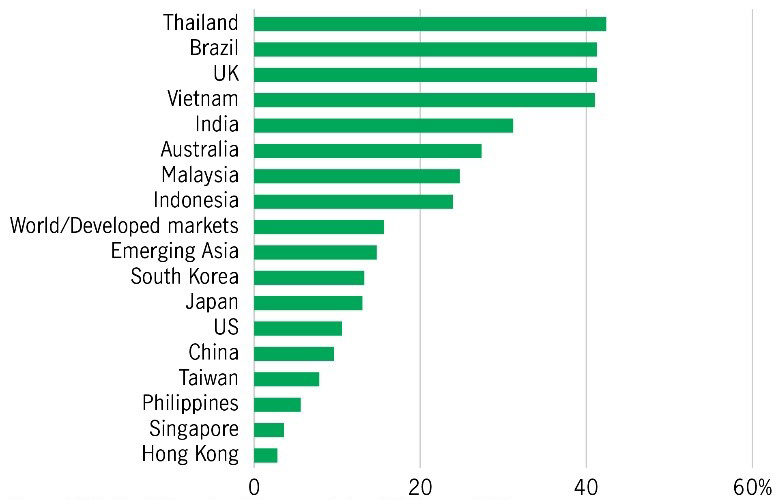

Within emerging markets, we’re relatively more positive toward select Asian equities (commodity-exporting markets such as Indonesia, Thailand, and the Philippines).

MSCI market exposure to materials, energy, and staples

Select bonds that can outperform

In our view, the prospect of aggressive rate hikes is now lower, and the Fed is expected to raise interest rates by only 25bps in March (50bps had been anticipated by the market). We also think that bonds now look more favorable and our overall allocation has been revised to less of an underweight.

Assuming current geopolitical events and stagflation do not lead to a severe recession, we believe the U.S. high-yield market has the potential to deliver relatively better performance versus risk assets such as equities because the asset class provides better compensation in the form of higher coupons. Also, U.S. high yield has a lower default potential versus other regions, as these bonds have a relatively greater exposure to oil and gas sectors. Although signs of financial deleveraging in the face of liquidity withdrawal by the Fed will need to be monitored carefully.

Meanwhile, floating-rate bonds (beneficiaries of a rising rate environment), China renminbi government bonds (a stable exchange rate and higher coupon rates versus other government bonds), and preferred securities (a fixed-income-like product that offers higher coupon rates) are also expected to be more resilient than other risk assets.

Other income-generating asset classes, such as real estate investment trusts (REITs), will be supported, as rate differentials (REIT yields minus government bond yields) should narrow at a slower pace than before.

Commodities

We view commodities in two ways: as inflation hedges and diversification tools. We expect commodity prices such as oil and agriculture products to remain elevated on the back of supply disruptions and geopolitical events. Commodities with inflation-hedge properties such as precious metals (gold and silver), oil, and farm products could perform better.

Conclusion

At this time of writing, the macro outlook and geopolitical events remain highly fluid. The odds of slower growth and higher inflation are rising, and we believe investors should seek active management and diversification to reshape their portfolios in an evolving investment landscape.

1 Bloomberg, as of March 7, 2022. Federal funds futures indicated a 96.9% chance of a 25bps hike at the March Fed meeting. On the announcement of European Union sanctions, Germany’s 10-year government bond price rose from 97.776 on February 25, 2022, to 100.799 on March 1, 2022. Meanwhile, 10-year bond yields fell from 0.2261% to -0.0799% over the same period. 2 Bloomberg, as of March 7, 2022. Eurozone IHS Markit's Composite Purchasing Managers' Index climbed to a five-month high of 55.5 in February 2022. On March 8, 2022, the United States banned Russian oil exports. The European Union announced a series of sanctions against Russia. These included a ban on all transactions with the Central Bank of Russia, which limits its ability to access foreign reserves. In addition, seven Russian banks were removed from the SWIFT international payments system and eurozone-based companies banned from exporting technology to Russian weapons manufacturers, pharmaceutical companies, military communications units, and shipyards. Last, eurozone-based companies are banned from doing business with the designated state-owned companies specializing in military production. 3 Bloomberg, as of March 7, 2022. The U.S. economy expanded by 5.7% year over year in 2021, a higher-than-trend growth of 2.0% to 3.0%.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange-trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

550654