Asia-Pacific (ex-Japan) equities: strategic opportunities amid a diverging landscape

Asia-Pacific (ex-Japan) equities fell marginally year to date (as of September 24, 2021) amid substantial dispersion among markets.¹ The recent resurgence of COVID-19 cases, coupled with rising inflation across the globe and market volatility in China, has raised questions about the pace of the economic recovery and the trajectory of equity markets in Asia. Our Asian equities investment team outlines the key factors that will drive equities for the remainder of 2021. Although the divergence in regional performance is expected to continue, they believe the broad Asian equity universe continues to offer attractive opportunities for active managers who seek diversification and reasonably valued companies.

Throughout the COVID-19 pandemic, both last year and into 2021, we foresaw a divergence in the performance of Asian equity markets. In 2020, East Asian markets with superior pandemic containment measures and relatively higher inoculation rates led the region, while ASEAN countries lagged due to concentrated urban populations, limited access to vaccines, and less developed healthcare infrastructure.

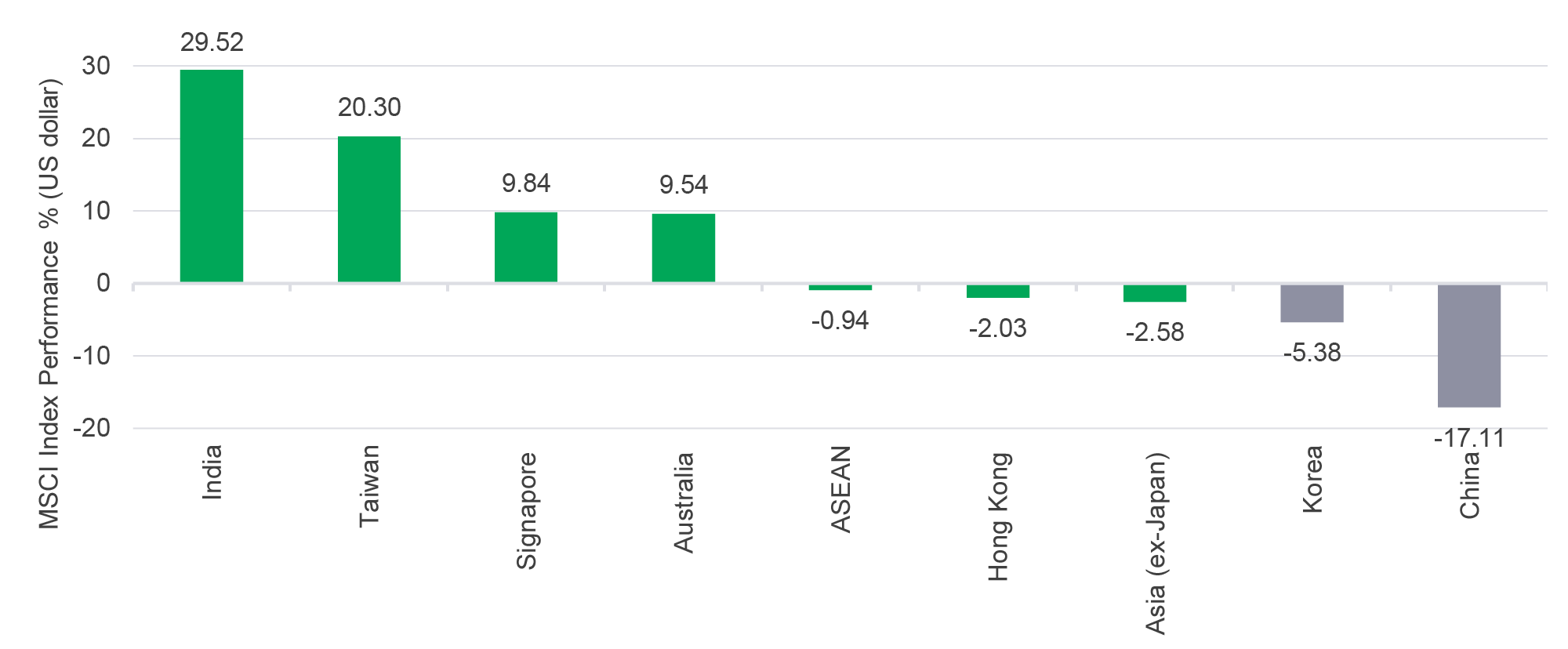

Looking at year-to-date market performance in the region (September 24, 2021), we saw some changes within the market dynamic. Some North Asian markets (e.g., Taiwan) have continued to perform well while others have fallen. India has emerged as the best-performing regional market, rebounding after experiencing a second COVID-19 outbreak earlier in the year. Meanwhile, ASEAN markets have posted marginally negative performance.

Asian equity market performance, 2021 (year to date)

The rest of 2021: growth divergence expected to continue

After a sharp recovery from the pandemic-driven collapse in economic activity so far, we expect growth—both globally and across Asia-Pacific—to moderate throughout the rest of 2021. The resurgence of COVID-19 cases, particularly in India, has deferred the highly anticipated economic recovery to the latter part of the year. Even then, hopes of a significant recovery throughout the remainder of the year depend greatly on inoculation rates and each country’s ability to contain the spread of new variants.

On the policy front, the U.S. Federal Reserve adopted a more hawkish tone at its June policy meeting² and might begin the long process of tapering its monthly asset purchase program. This is likely to be one of the most closely watched events moving forward. Other major central banks have also indicated a shift toward a tightening bias.³

Our current macro assessment: monetary policy and inflation

In our view, most market participants aren’t yet ready for tighter monetary policy globally. This is evidenced by companies with negative free cash flow trading at the highest price-to-book values, relative to the market, in the past 20 years. In our view, the market may be pricing in excessive optimism in regard to these companies, relying on growth fueled by external capital instead of organically generated cash flows; however, these valuations may be challenged as bond yields rise.

Inflation may also prove challenging for some companies: Rising raw material prices, freight costs, and the reduced supply of electronic components and semiconductor chips in the first half of 2021 are expected to place pressure on the earnings of certain downstream industries. However, we think the impact of cost-push inflation will ease when supply chains across different regions return to a more normal level.

China: opportunities amid increased volatility and a shifting regulatory landscape

Looking ahead, China’s economic agenda will likely center on the development of advanced technology, the real economy, industrialization, and decarbonization. These are areas where we anticipate policy tailwinds.

For example, we have a positive stance on China’s renewable energy sector—especially companies in the power-grid network and solar-energy supply chain—where we see strong structural growth potential, driven by the government’s goal to reach carbon neutrality by 2060.

Similarly, we expect 5G infrastructure to unleash the potential of segments such as industrial automation, autonomous driving, smart cities, and artificial intelligence—such development is expected to drive demand for cybersecurity software and services. This area remains underappreciated, in our view.

We also see opportunities in regions outside of China, namely Europe, the United States, and other emerging markets. This includes companies exposed to the recovery in consumption and investments.

Technology in Taiwan and South Korea

While investors may be concerned about short-term weakness in the tech cycle, we believe the long-term growth outlook for the sector in Taiwan and South Korea remains promising. We expect another round of tech product upgrades to occur in 2022, as tech bellwethers introduce new chips and software that must be supported by new product specifications. Furthermore, the deployment of 5G-related applications remains at a nascent stage of growth, and we believe that momentum will gather pace in 2022.

India: a slower rebound could favor financials, materials, and IT names

India suffered a setback after COVID-19 infections spiked during the second wave. But as this appears to be easing and state governments have indicated that they’ll take a more measured approach to easing restrictions, suggesting that a more gradual economic recovery lies ahead. We expect to see a downward revision in full-year 2022 earnings estimates before improvements occur in 2023. Given rising material and commodity prices across the globe, we think that Indian-branded consumer goods companies could face margin pressure.

That said, we see favorable risk/reward characteristics in the following sectors:

- Financials: Most large banks are well capitalized and we expect credit costs to be manageable. Furthermore, these banks are more likely to benefit from formalization and the cyclical recovery following the second COVID-19 wave.

- Materials: We’re optimistic about the domestic building materials sector as we believe firms within this space could pass on cost increases at a faster rate than pure consumer companies.

- IT services: With U.S. corporate earnings showing strength, IT remains cyclically well positioned. We’re more positive on larger-cap names as they’re better positioned to manage salary inflation and attrition during the upturn. IT also provides protection against policy tail risk should the rupee depreciate due to changes in global monetary policy.

- Structural growth opportunities over the longer term: We’re constructive on macro themes such as import substitution plays that could benefit from the “made in India” policy and the China+1 supply chain diversification trend. In our view, opportunities could be found across the materials and healthcare sectors.

ASEAN: opportunities amid a challenging economic landscape

The recovery in most Southeast Asian countries now looks more subdued following the resurgence of COVID-19 cases. The spread of the more infectious Delta strain amid a relatively slower vaccination rollout has taken its toll on the region’s economy. We now expect a downward revision to the region’s growth outlook this year. That said, we believe that companies in the following sectors will outperform:

- Healthcare: During the initial stage of the outbreak, hospitals suffered from low patient flows and the cancellation of elective surgeries. Over time, these hospitals have subsequently benefited from assisting the government to perform COVID-19 tests and treating patients. Income derived from these services has helped sustain earnings growth. Post COVID-19, these facilities should benefit from the normalization of operations and a resumption in healthcare tourism.

- Exporters: Manufacturers in Southeast Asia should continue to do well due to solid demand from reopening in the United States and Europe. Some companies have benefited from the shift in orders from China to Southeast Asia. While restricted operations and component shortages may cause some disruption, we believe the impact will be short-lived. The region’s exporters also typically benefit from a stronger U.S. dollar in the event of tapering-related anxiety.

- Digitization of the ASEAN economies: As highlighted in our 2021 outlook, Southeast Asian countries, particularly Indonesia, are experiencing robust growth in their digital economies. Data centers in Indonesia are rapidly expanding as digitization gathers pace across the financials, e-commerce, and ride-hailing sectors. Demand for logistics and warehousing services has grown strongly in the region, and we see high levels of investment in these areas. We anticipate that the listing of key sector leaders in the second half of 2021, particularly in Malaysia and Indonesia, will set the benchmark for the future listing of more new economy businesses in Southeast Asia.

Conclusion

The divergence of Asian equities’ performance so far in 2021 is poised to continue. North Asian economies and Singapore with higher vaccination rates and better containment measures should have a longer runway for growth. In contrast, the recovery for many ASEAN markets has been delayed and may not occur until the end of 2021 or early 2022. This divergence offers a unique opportunity for active managers to choose quality companies throughout the region.

1 The MSCI AC Asia-Pacific Index fell 2.58% through September 24, 2021, but there was significant divergence between the best-performing market (India) and worst-performing market (China). 2 “Transcript of Chair Powell's Press Conference,” federalreserve.gov, June 16, 2021. 3 In this instance, we’re referring to the People’s Bank of China, the European Central Bank, Bank of England, and the Reserve Bank of Australia. 4 Multinational companies based in China to look for another supply chain center in Asia to diversify their supply chains.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other pre-existing political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material, intended for the exclusive use by the recipients who are allowable to receive this document under the applicable laws and regulations of the relevant jurisdictions, was produced by, and the opinions expressed are those of, Manulife Investment Management as of the date of this publication, and are subject to change based on market and other conditions. The information and/or analysis contained in this material have been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. Past performance does not guarantee future results. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit nor protect against loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than 150 years of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at www.manulifeim.com/institutional

Australia: Hancock Natural Resource Group Australasia Pty Limited., Manulife Investment Management (Hong Kong) Limited. Brazil: Hancock Asset Management Brasil Ltda. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area and United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority, Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland. Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad (formerly known as Manulife Asset Management Services Berhad) 200801033087 (834424-U) Philippines: Manulife Asset Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Hancock Natural Resource Group, Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife Investment Management, the Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance

543341