2026 corporate tax rate card for Canada

2026 Corporate tax rate card

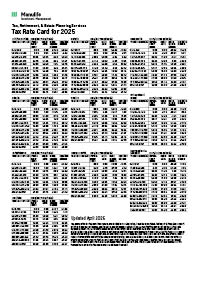

The latest 2026 corporate tax rate card puts the most up-to-date corporate tax rates for active business income, investment income, and much more all in one place. This reference card is designed to help you and your corporate clients with tax planning for the 2026 calendar year.

Included in this piece are tables for:

- combined federal and provincial corporate tax rates for Canadian-controlled private corporations on their active business income and investment income

- small business limit reductions on taxable capital employed and adjusted aggregate investment income

- corporate tax integration tax tables for tax deferral/(prepayment), tax savings(cost) and the retention advantage/(disadvantage) on various income sources

Confused about what all these numbers mean?

Contact your advisor for help and to create a solid tax and investment plan. In the meantime, here are some details that might help you get started.

Canadian-controlled private corporation (CCPC)

Is a private corporation with shares that aren’t listed on a designated stock exchange that was incorporated in and is a resident of Canada. It isn’t controlled by non-resident persons, public corporations that are listed on a designated stock exchange in or outside of Canada or any combination thereof.

Small business limit

The dollar value limit for active business income of a CCPC that’s taxed at rates subject to the small business deduction. This results in the lowest effective federal and provincial tax rates that can apply to active business income.

Active business income

Active business income is income earned from a business source, including any income incidental to the business.

Small business deduction

The small business deduction is a reduction to the corporate tax rate on active business income up to the small business limit.

General tax rate

The tax rate that applies to active business income that isn’t eligible for the small business deduction because it’s above the small business limit. Instead, this active business income is eligible for the smaller general rate reduction, resulting in higher effective federal and provincial tax rates than income eligible for the small business deduction.

Investment income tax rate

The tax rate that applies to investment income other than Canadian dividends that isn’t eligible for either the small business deduction or the general tax rate reduction. Income subject to this rate isn’t considered active business income.

Taxable capital employed in Canada

This is a measure of the financial resources a company uses to make money in Canada. The value is determined by a prescribed formula. When taxable capital employed exceeds a specific threshold, it can reduce CCPC’s small business limit.

Adjusted aggregate investment income

This includes sources of passive income, like capital gains net of the current year’s capital losses, interest, foreign dividends and Canadian dividends from an investment portfolio among other passive sources. When the total income from these sources exceeds a specific threshold, it can reduce CCPC’s small business limit.

Proper tax planning is something that can save you a lot of money. There are many different tax strategies you can implement, depending on your age, income, personal situation and goals. We recommend meeting with your advisor to come up with a plan that works for you and helps you achieve your specific goals.

For information on your personal 2026 tax rates see our 2026 tax rate card. For additional tax planning support, see our 2026 Advisor Quick Reference Guide.

Important disclosures

Important disclosures

This communication is published by Manulife Investments. Any commentaries and information contained in this communication are provided as a general source of information only and should not be considered personal investment, tax, accounting or legal advice and should not be relied upon in that regard. Professional advisors should be consulted prior to acting based on the information contained in this communication to ensure that any action taken with respect to this information is appropriate to their specific situation. Facts and data provided by Manulife Investments and other sources are believed to be reliable as at the date of publication.

Certain statements contained in this communication are based, in whole or in part, on information provided by third parties and Manulife Investments has taken reasonable steps to ensure their accuracy but can’t be held liable for such information being inaccurate. Market conditions may change which may impact the information contained in this document.

You may not modify, copy, reproduce, publish, upload, post, transmit, distribute, or commercially exploit in any way any content included in this communication. Unauthorized downloading, re-transmission, storage in any medium, copying, redistribution, or republication for any purpose is strictly prohibited without the written permission of Manulife Investments.

Manulife Investments is a trade name of Manulife Investment Management Limited and The Manufacturers Life Insurance Company.

Manulife, Manulife & Design, Stylized M Design, and Manulife Investments are trademarks of The Manufacturers Life Insurance Company and are used by it and by its affiliates under license.